|

|

||||||

|

|

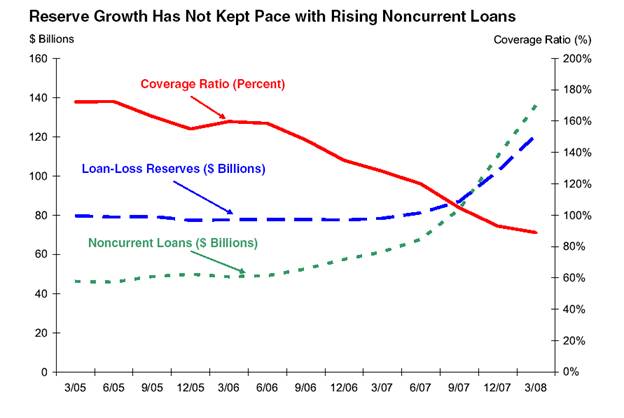

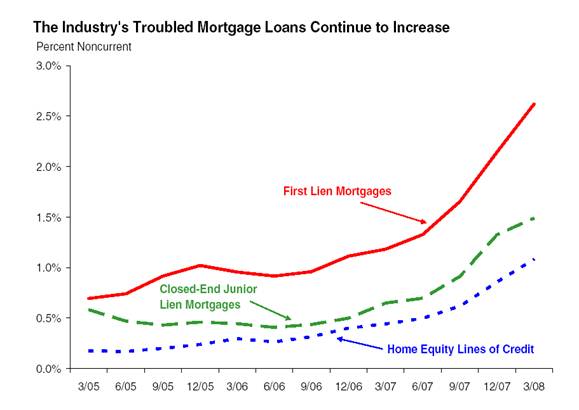

June 2, 2008 Wall Street Decides to Close Its Ears and Hum With recent economic reports coming in generally weak but slightly better than expectations, we're seeing a relative calm in the financial markets. We don't see investors abandoning their aversion to risk, (though we're still alert to any signs of substantial improvements in market internals that would signal that), so there's not enough optimism to provoke self-feeding speculation. Still, credit spreads held relatively steady last week, rather than continuing their recent widening. For now, we remain tightly hedged, since the overall profile of valuations and market action remains unfavorable. As I noted a couple of weeks ago, "The reality is that as recessions develop (and I continue to believe the U.S. faces a much more significant downturn than we've observed to date), the data can take months to accumulate to a compelling verdict, and in the meantime, speculative pressures can remain alive." Lest investors allow the weak but benign economic reports to create an "all clear" impression for the economy, the latest FDIC Quarterly Banking Profile, released last week, should encourage them not to close their ears and hum. I have to say that having read these regularly since the early 1990's, this is easily the most dismal report I've ever seen. Among the highlights: "Industry earnings for the fourth quarter of 2007 were previously reported as $5.8 billion, but sizable restatements by a few institutions caused fourth quarter net income to decline to $646 million." Note what the FDIC is saying here. The banking industry reported $5.8 billion in earnings to its investors, but restatements took that total down by 89%. Stop and think about that - only 11% of the earnings that were reported to investors survived after the restatements. And yet, investors seem naively willing to take recent earnings reports, guidance and charge-off levels at face value, as if these reports can be trusted. Unfortunately, all that seems to matter to investors over the short-run is whether earnings-per-share can beat estimates by a penny, regardless of whether they are massively restated later. The report continues, "Noncurrent loan growth remains high. The annualized net charge-off rate in the first quarter rose to 0.99 percent, more than double the 0.45 percent rate of a year earlier and the highest quarterly net charge-off rate since the fourth quarter of 2001. Even with the heightened level of charge-offs, the amount of loans and leases that were noncurrent (90 days or more past due or in nonaccrual status) rose by $26.0 billion (23.6 percent) in the first quarter, following a $27.0-billion increase in the fourth quarter of 2007. Loans secured by real estate accounted for close to 90 percent of the total increase, but almost all major loan categories registered higher noncurrent levels." Now, one might respond, fine, the rate of non-current loans was high, but financials have charged off their losses, so the heavy write-downs are behind us. But that's where the FDIC suggests that investors are wrong. While there are, in fact, more loss reserves per dollar of total loans now, these reserves aren't keeping up with the proportion of loans that are actually going bad: "Insured institutions continued to build their loan-loss reserves in the first quarter. The industry's ratio of loss reserves to total loans and leases increased from 1.30 percent to 1.52 percent, the highest level since the first quarter of 2004. However, the growth in loss reserves was outstripped by the rise in noncurrent loans, and the industry's "coverage ratio" fell for the eighth consecutive quarter, to 89 cents in reserves for every $1.00 of noncurrent loans from 93 cents at the end of 2007. This is the lowest level for the coverage ratio since the first quarter of 1993."

Look carefully at the slopes of the lines on the chart above. Given that mortgage resets remain heavy and will continue well into 2010, is it really reasonable to assume that the increase in noncurrent loans will suddenly subside? From our perspective, it is far more likely that the rate of loan-loss reserves will be forced up sharply, simply to prevent further erosion in the coverage ratio. In order to actually raise the coverage ratio to normal levels, far more massive writedowns will be required than we've observed to date.

The implications of this go far beyond whether or not the prices of financial stocks have "discounted" the lower potential earnings. See, this isn't just a problem of whether the stock prices of financial companies are right. The larger issue is what happens on the real side of the economy, in terms of spending and lending and economic activity. I can't overly stress the points made by Martin Feldstein (the head of the National Bureau of Economic Research, which officially dates U.S. recessions) just a few weeks ago: "I'll tell you what worries me. We saw house prices overshoot by 60% relative to costs of building and relative to rents. And I worry about the possibility that they will keep falling; they will spiral downwards. In the same way that they went much too high, they could go much too low. And if that happens, then we are going to see individuals feeling a lot poorer, cutting back on their spending, defaulting on mortgages, and we're going to see the holders of those mortgages see their assets, their capital being cut and therefore their ability to make loans being cut." In short, investors appear to be viewing the recent period of weak but not terrible economic news as a signal that the worst is behind us and that clear conditions are ahead. That could very well provoke some self-feeding speculation, which we would observe first through an improvement in breadth and price/volume behavior. But even if we do see some fresh short-term speculation, the evidence suggests that the worst of the credit problems are still well ahead. It would be naïve to accept that the amount of writeoffs taken to-date is anything close to what will be required - they are not even keeping pace with the accelerating pace of non-current loans. Financial companies should, and most probably will, get to the task of preserving capital, cutting dividends further, and raising new funds in the not-distant future. The markets probably will not like this, because it will be an admission that credit conditions are still deteriorating. Meanwhile, new claims for unemployment remained firm last week, rising to 372,000. It is typical for those claims to spike following an early-recession lull. At the point where we observe a 400,000 figure, market psychology is likely to shift rapidly. Whether or not investors accept that as a likelihood, they should certainly recognize it as an important risk factor here. Market Climate As of last week, the Market Climate for stocks remained characterized by unfavorable valuations and unfavorable market action. The stock market remains relatively overbought, so there remains a continued risk of abrupt weakness given the unfavorable Climate. For now, the Strategic Growth Fund remains fully hedged, but we are willing to cover a moderate portion of our short call options (leaving the defensive put coverage of our hedge in place) if market internals improve sufficiently to indicate more robust risk tolerance among investors. Here and now, we remain defensive and very skeptical of the notion that the U.S. has skirted a downturn. With regard to the "economic stimulus," I remain convinced that consumers are sufficiently indebted, and concerned about that debt, to use the bulk of the tax rebates in hand for debt service. In equilibrium, the U.S. government will have issued more Treasury bonds, in order to finance a similar contraction in mortgage indebtedness. The effect of the "stimulus" will simply be a modest increase in the volume of Treasury debt held by the public, foreigners and financial institutions, and a modest decrease in the volume of mortgage debt held by the public, foreigners and financial institutions. In bonds, the Market Climate remained characterized last week by moderately unfavorable yield levels and moderately unfavorable yield pressures. With the 10-year Treasury yield pushing over 4% last week, we are approaching yield levels that would support a somewhat longer portfolio duration than we currently have. As I've frequently noted, yield levels in the bond market hold more sway, in terms of total return implications, than prevailing yield trends (which need not persist indefinitely). So I would expect to respond to normalized yield levels - relative to inflation, economic growth, and other factors - by increasing the maturity profile of our holdings in the Strategic Total Return Fund. For now, the Fund has a very low duration of less than 1 year, mostly in Treasury bills (which is unusual and not likely to persist as market conditions change) and also holds about 15% of assets in foreign currencies. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |