|

|

||||||

|

|

March 22, 2010 Zombies and Rube Goldberg Machines When I was a kid, I used to make up different Rube Goldberg machines and put them together for fun. You've seen the type - a ball rolls down a Hot Wheels track and falls into a cup, which drops down a pulley onto a little see-saw, which knocks a domino onto a mousetrap, which yanks a string, which pulls a block forward with a pin on it, which pops a balloon. They usually went much faster in practice than I had imagined, and the mousetraps would invariably get at least one finger, but it was entertaining. This, to my mom, was much preferred to my attempt to ride down the stairs in my top dresser drawer with my best friend Jimmy. In hindsight, that was a Bad Idea, since the drawer burst into pieces and we found ourselves tumbling to the floor. As we look at the U.S. financial system, and particularly the mortgage market, it strikes me that we've created one massive Rube Goldberg machine which is very complicated, but has the end result of obligating the U.S. public to huge bailouts, possibly without their continuing knowledge. At one end, the Fed purchases $1.5 trillion in Fannie and Freddie debt obligations. Then the Treasury guarantees those obligations. Then Fannie and Freddie begin buying back delinquent mortgages, paying off the lenders in full, and taking the losses at public expense. Next thing you know, a mousetrap snaps and a bubble gets popped. I've detailed some of these concerns in the 2/16/2010 comment The Federal Reserve's Exit Strategy: Unlegislated Bailout of Fannie and Freddie. Meanwhile, the FASB continues to allow banks "significant judgment" in valuing their assets. This risks creating a zombie ("living dead") banking system by allowing a growing gap to emerge between stated asset values and the probable stream of cash flows from these loans. This is not wisdom, but is instead a decision to collectively close our ears and hum. An essential part of a sound financial system is the ability to verify assets, and a clear set of standards on how impaired assets should be valued, and equally important, reported. Undoubtedly, "significant judgment" should end at the point that a mortgage actually goes delinquent, but it's uncertain that this is the standard being applied. Modifications and foreclosures force a restatement of the asset on the balance sheet, and in the current environment, the ability to obscure valuations appears to be a primary reason for the growing gap between delinquencies and foreclosures, as well as the reluctance of banks to modify mortgages. Allowing dead assets to stay on the books as if they are alive is precisely what created insolvent zombie banks in Japan, which continued to operate for over a decade at public expense, even while lending activity stagnated. On this front, the growing gap between delinquencies and foreclosures is notable. It's not at all clear how this growing gap will be resolved. In the coming quarters, it is possible that accounting firms, given the implosion of Arthur Anderson following the Enron scandal, will force greater discipline on the banks than they may be willing to exercise on their own. In that case, we may observe some of the same pressure we anticipated in February 2008 (Watching for Audit Delays and "Unqualified" Opinions), as reported bank losses started to accelerate. Strenuously Overbought, Again On Thursday, the S&P 500 pushed to a strenuously overbought level, with over 90% of S&P 500 stocks above their respective 50-day, 20-day and 10-day averages. Back on October 19, 2009, when the S&P 500 was about 5% lower than it is here, I noted that the S&P 500 had never been more (intermediate-term) overbought. Clearly, the overbought conditions we observed 5 months ago did not prevent the market from pushing a few percent higher to yet another strenuously overbought peak (which is much what we experienced at several points in 2007 as well). Still, even a shallow correction would put the market back at those October levels. That sort of outcome is an important characteristic of strenuously overbought markets. Even if things work out well over the short term, it is rarely rewarding to chase such advances, since prices typically retreat to the same or lower levels a few months later (and in some cases, can remain below those levels years later). Back in October, I noted "investors clearly are approaching the current market with every belief that the extreme valuations of 2007 represent the sustainable norm to which stocks should return. This despite the fact that the 2007 peak reflected rich valuation multiples against earnings that were themselves inflated by abnormally elevated profit margins. The anchoring of investor expectations to a period of rich valuations and unusually wide profit margins may not be reasonable, but it prevents any ability to "forecast" a significant near term decline, much less a sustained downtrend. At the same time, we do have sufficient evidence to indicate that market risk is not worth taking on the basis of average outcomes from the combination of valuation and market action we currently observe." With the overvalued, overbought conditions of October now compounded by rising yield pressures and overbullish sentiment on a variety of measures (investment advisors are again down to just 21.3% bears), we remain defensively positioned here. While investors looking at the 2007 highs undoubtedly observe a significant amount of apparent "room to recover" for stocks, it is extremely important to recognize that those 2007 valuations were what one might call "Bubble Part II", and priced stocks for terribly poor long-term returns. Unless investors wish to repeat the experience, it is worth noting that stocks are already overvalued beyond nearly every pre-bubble norm. Indeed, outside of the bubble years from the late 1990's through 2007, the S&P 500 has never been priced to achieve a poorer long-term return than it is now. Bill Hester underscores this point his latest research piece this week, An Update on Valuations and Forward Earnings Assumptions (additional link below), which reviews the current valuation picture. Based on analyst estimates for expected S&P 500 operating earnings, Bill observes, "Last October, analysts were about half way to pricing in profit margins that matched the record levels of 2007. Now, they are just about there." It is important to note that our current defensive position is driven by the present combination of overvalued, overbought, overbullish conditions, coupled with upward yield pressures, and is independent of my larger concerns about the potential for a second wave of credit strains. So there are two distinct sets of concerns here, one that would exist even in the absence of credit concerns, and the other that directly involves those concerns. This distinction is important, because as we've anticipated for months now, we have finally entered the window in which additional credit strains - if they are indeed likely to emerge - should actually begin appearing in the data. Specifically, beginning with data for February 2010 and later, the concern is that we will begin to observe a spike in delinquencies - first in the form of "30-day delinquencies" and gradually in either large increases in loan loss provisions or in the actual onset of foreclosures. Moreover, first quarter earnings reports will give us the first look at various off-balance sheet entities that are now required to be brought onto corporate balance sheets. So the several few months will be important in gauging the extent to which "second wave" risks are or are not materializing. While it would be difficult to take a lack of fresh credit strains as evidence of restored health in the banking and lending system, we can't rule out the possibility that the Rube Goldberg machine created by the Fed and the Treasury will be enough to take us through a period of years (or if we follow Japan's example, decades) where we will gradually bury the losses of the banking system, trading a short-lived period of adjustment instead for a long-term period of stagnant credit. We will not retain our concerns about second-wave credit strains if the data do not support it. As we move through this year, absent fresh credit strains, we will gradually assume a "post-war" world. If these strains do not emerge, we will scale (in an approximately linear way) our weights through 2010 to place greater weight on the "typical post-war recovery" dataset, while gradually fading our concern about abrupt solvency problems in our financial system. That is, we will move gradually with the evidence. For now, the Market Climate is unfavorable regardless of whether the unobserved "data set" we are in reflects an ongoing post-crash credit crisis or a typical post-war recovery. We have anticipated the current window of potential trouble for some time now. The most important basis for accepting greater risk will continue to be better clarity and better valuation. Market Climate As of last week, the Market Climate remained characterized by strenuous overvaluation, strenuous overbought conditions, overbullish sentiment, and hostile yield pressures. Even without any concern about credit conditions, this set of evidence holds the Strategic Growth Fund to a fully hedged investment stance. As noted last week, our hedges currently take a "staggered strike" conformation, and is the most defensive stance we've taken since the 2007 peak. This staggered strike differs from a plain-vanilla "fully hedged" stance by using about 1% of assets to raise the strike prices of our defensive put options. Aside from that amount of put option premium, the primary driver of day-to-day returns in the Fund here is the difference in performance between the stocks the Fund owns and the indices (S&P 500, Russell 2000 and Nasdaq 100) that the Fund uses to hedge. In bonds, the Market Climate remained characterized last week by modestly unfavorable yield levels and hostile yield pressures. The Strategic Total Return Fund continues to carry a duration of about 4 years, mostly in intermediate term Treasury notes. My near-term concern continues to be the risk of fresh credit strains. As we observed in 2008 and early 2009, the likely outcome of such credit strains is a flight-to-safety toward default-free Treasury securities (a flight that tends to outweigh supply concerns over the near term), and a tendency toward dollar strength and commodity weakness. That said, the long-term implications of bailouts, tax shortfalls and lack of budget discipline is likely to be significant inflation pressure beginning about 4 years or so out, and continuing for the remainder of the decade. The chart below provides an effective reminder of the situation. It should not escape investors that the rapid expansion of deficits during the 1970's and into the early 1980's was accompanied by a hostile inflation climate, while the fiscal discipline of the 1990's produced a very pleasant period of low inflation pressures. Inflation is always and everywhere a fiscal phenomenon. Though hyperinflations are typically driven by the inevitable financing of fiscal deficits by money creation, you will not find sustained inflation without sustained fiscal irresponsibility. As Peter Bernholz notes in Monetary Regimes and Inflation, "there has never occurred a hyperinflation in history which was not caused by a huge deficit of the state." While we certainly don't anticipate anything on the order of hyperinflation, the expansion in deficit spending that we currently observe (regardless of whether one measures the deficit as a fraction of GDP or as a fraction of government spending) is beyond anything ever observed in the post-war era. I continue to anticipate a near doubling in the CPI over the course of about 10 years, focused primarily in the latter half of this decade.

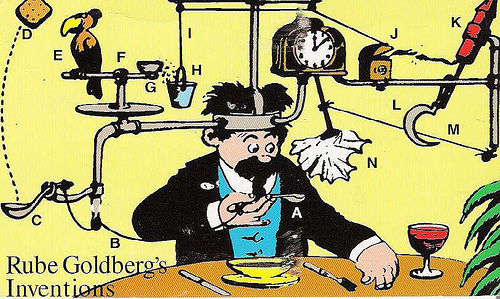

NEW from Bill Hester: An Update on Valuations and Forward Earnings Assumptions --- Professor Butts and the Self-Operating Napkin. The "Self-Operating Napkin" is activated when the soup spoon (A) is raised to mouth, pulling string (B) and thereby jerking ladle (C) which throws cracker (D) past parrot (E). Parrot jumps after cracker and perch (F) tilts, upsetting seeds (G) into pail (H). Extra weight in pail pulls cord (I), which opens and lights automatic cigar lighter (J), setting off skyrocket (K) which causes sickle (L) to cut string (M) and allow the pendulum with the attached napkin to swing back and forth, thereby wiping chin.

--- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |