|

|

||||||

|

|

December 4, 2011 Have We Avoided A Recession? In recent months, we've observed a fairly neutral flow of economic data - not strong by any means, but offering a reprieve from the clearly negative momentum that we observed in late-summer. The following chart is presents a consensus of economic measures that we track as a composite (long-term chart here ), focusing on the past decade. Note the bounce toward zero that we've seen in recent months. New orders remain generally weak, but other measures are dead-neutral. Note that we saw a similar pop for a few months just as we were entering the last recession in 2007. Modest upticks in these measures - even if concerted - don't carry much information.

The latest employment report presents a similar picture. Payrolls increased by a tepid 120,000, which is much less than would normally be required just to keep the unemployment rate steady. But the November unemployment rate actually "improved" to 8.6% last month, largely because 315,000 unemployed workers abandoned their search for work, thus dropping out of the count altogether. Overall the report wasn't bad, but it was simply too tepid to carry much information. Combining the average workweek with average hourly earnings for all employees provides a nice complementary measure of economic activity. The data below are deflated using the core CPI to better reflect real income. Again, we observe a modest improvement from the negative economic momentum of a few months ago, but very little evidence to suggest a sustained turn in direction. Indeed, we saw the same sort of pop just as we were entering the last recession.

In our view, it is very difficult to obtain useful views about economic direction using the standard "flow of anecdotes" approach that is the bread-and-butter of many analysts. The economic data reported daily are a mix of leading, coincident and lagging indicators, often noisy and subject to revision, and without any overall economic structure. Adjusting one's entire economic views following each report, as if each somehow adds significant information, is a recipe for confusion. Treating economic data as a flow of anecdotes, without putting any structure around them, is why the economic consensus has failed to ever anticipate an oncoming recession. We use a variety of methods to gauge recession risk. The most straightforward is to form fairly low-order indicator sets like our Recession Warning Composite (see November 12, 2007, Expecting A Recession ), that have a long historical record of accurately distinguishing recessions. These indicator sets are comprised of what might be called "weak learners" - conditions that do not in themselves have infallible records of identifying recessions, but that provide very strong signals when observed in combination with other recession flags. They include fairly straightforward conditions such as whether or not the S&P 500 is below its level of 6 months earlier, whether credit spreads are wider than they were 6 months earlier, whether the Purchasing Manager's Index is in the low 50's or below, and so forth. As of last week, a simple average of 20 of these binary recession indicators continued to show a preponderance of signals still in place - a condition that has never been observed except alongside a U.S. recession.

Moreover, we can select random subsets of these indicators across random periods of time, in order to make the model less sensitive to exactly how it is put together. That method typically produces more variation in the overall conclusion about the economy, so the confidence in that conclusion is particularly strong when multiple models agree. At present, we observe agreement across a broad ensemble of models, even restricting data to indicators available since 1950 (broader data since 1970 imply virtual certainty of recession). The uniformity of recessionary evidence we observe today has never been seen except during or just prior to other historical recessions.

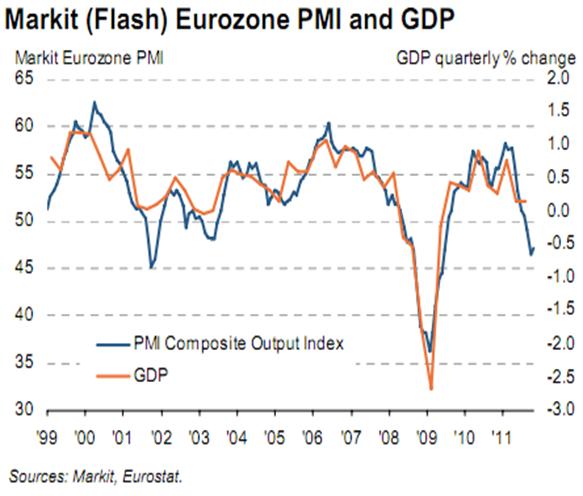

Moreover, if we look around the world, we already observe clear signs of a downturn. This deterioration is most notable in Europe, where the Eurozone PMI is already consistent with economic contraction at an annual rate of about 2%.

Similar evidence of an emerging downturn can be seen in China (graphic via Mike Shedlock)

In short, recent U.S. economic reports have improved modestly from the clearly negative momentum that we saw in late-summer. Unfortunately, the underlying recessionary pressures we observe are largely unchanged. When we take the present set of economic evidence in its entirety, we see very little evidence of a meaningful reduction in recession risks. Indeed, the evidence from the rest of the world, both developed and developing, reinforces the expectation that the global economy is approaching a fresh contraction. Wanted: Voluntary losers As of Friday the yield on 1-year Greek debt is up to a new record of 297%, with the 1-year note trading at 32.50 and other debt trading at about 25% of face value. Haven't we moved past Greece already? Well, no. Based on reported holdings of Greek debt in the European banking system, the implied losses on Greek debt alone are now enough to put many European banks into capital shortage. Europe could solve Italy's issues tomorrow and European banks would still face a banking crisis. Investors were quite excited last week when central banks announced a coordinated reduction in the interest rate for U.S. dollar swap lines. It's interesting that the more arcane an intervention is, the more excited investors get - maybe because complex-sounding interventions allow Wall Street's imagination to run wild and substitute for actual understanding. Very simply, what happened last week was a liquidity operation - essentially, European banks can now borrow dollars for a fraction of a percent less than they previously could. This prevents transactions denominated in dollars from "freezing up" across Europe (since European banks are no longer willing to lend to each other). But it does nothing to address the sovereign debt crisis. It does nothing to make European banks more solvent. All a "swap" is, really, is a loan of X dollars, in return for some number Z euros. At the end of the period, the borrower pays back X dollars, plus some interest, and gets back exactly Z euros. Notably, it doesn't matter what the actual value of the euro is at the time of repayment. X and Z don't change. So the Federal Reserve, for example, doesn't take on any foreign currency risk in this trade. The euros are really nothing but collateral for what otherwise is a simple loan of U.S. dollars. Meanwhile, we're seeing various proposals for more complex ways for some institution to buy distressed European debt. The most recent iteration looks for the IMF to buy the debt. But when the IMF buys debt, it takes a senior claim to all other bondholders, and imposes conditions to make sure that their tranche of debt gets repaid (the IMF is emphatically not in the business of providing loans that it doesn't think it will get back). Europe doesn't face a liquidity problem. It faces a solvency problem. What investors really want isn't just for someone to buy distressed European debt, but for someone to buy that debt and willingly take a loss on it so the money doesn't ever actually have to be repaid. That isn't going to happen easily. Short of major fiscal improvements in Europe (which appear increasingly hopeless in the face of an oncoming recession) any solution will have to explicitly or implicitly impose losses on someone. In my view, the best "someone" is the investors who willingly made the loans in expectation of earning a spread, and who knowingly took a risk. The worldwide hope among these investors is that the "someone" taking the hit will instead be the German people, but Germany remains resolutely against printing permanent new euros in order to effectively redeem the debt of Italy and other countries. Despite hopes that the ECB will suddenly shift its policy on this, I continue to expect that any ECB purchases of distressed European debt will follow an agreement on European fiscal union, and that even if initiated, will be on a smaller scale than investors seem to hope. Without airtight fiscal credibility among distressed Euro-area countries, whatever debt purchases the ECB makes will be almost impossible to reverse. We represent the Lollipop Guild Frankly, I am concerned that Wall Street is becoming little more than a glorified crack house. Day after day, the sole focus of Wall Street is on more sugar, stronger sugar, Big Bazookas of sugar, unlimited sugar, and anything that will get somebody to deliver the sugar faster. This is like offering a lollipop to quiet down a 2-year old throwing a tantrum, and expecting that the result will be fewer tantrums. What we have increasingly observed over the past decade is nothing but the gradual destruction of the ability of the financial markets to allocate capital for the benefit of future growth. By preventing the natural discipline of the markets to impose losses on poor stewards of capital, and to impose interest rates high enough to force debtors to allocate the capital usefully, the world's policy makers are increasingly wrecking the prospects for long-term economic growth. The world's standard of living (what we can consume for the work we do) is intimately tied to its productivity (what we can produce for the work we do). That productivity requires our scarce savings to be allocated to productive physical capital, and to productive human capital (primarily education). Nietzsche famously said "What does not kill me makes me stronger." The corollary is "What constantly rescues me makes me weaker." The world will only stop looking for bailouts when policy makers stop handing them out. Market Climate As of last week, the Market Climate for stocks was characterized by conditions that reestablish the " whipsaw trap " that we observed a few weeks ago. Historically, about 70% of these low-sponsorship rallies have failed, but we are also aware that about 30% have not. For now, we remain broadly defensive in Strategic Growth and Strategic International, but are open to shifting to a moderately more constructive stance if we observe a more persistent improvement in market internals. Given our expectation of an oncoming recession, my impression is that our best opportunity for a more constructive investment stance is likely to come at significantly improved valuations (i.e. lower levels), but we'll take our evidence as it arrives. In Strategic Total Return, we continue to have about 20% of assets in precious metals shares, with low-single digit exposures in utility shares and currencies, and an average duration of about 3 years in Treasury securities. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |

(graphic via

(graphic via

{kind=link}