|

|

||||||

|

|

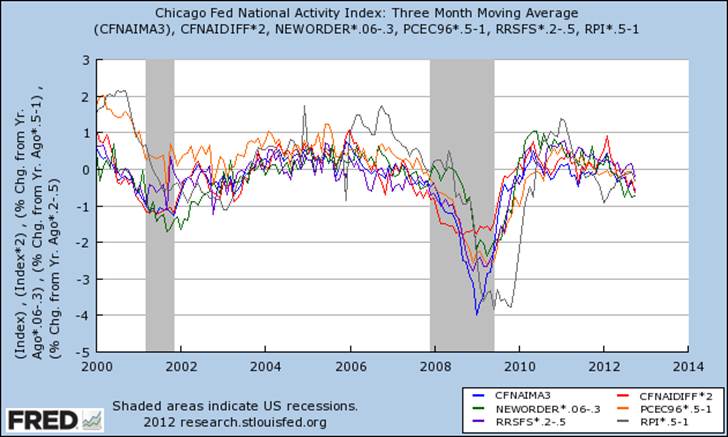

December 17, 2012 Roach Motel Monetary Policy While we continue to observe some noise and dispersion in various month-to-month economic reports, the growth courses of production, consumption, sales, income and new order activity remain relatively indistinguishable from what we observed at the start of the past two recessions. The chart below presents the Chicago Fed National Activity Index (3 month average), the CFNAI Diffusion Index (the percentage of respondents reporting improvement in conditions, less those reporting deterioration, plus half of those reporting unchanged conditions), and the year-over-year growth rates of new orders for capital goods excluding aircraft, real personal consumption, real retail and food service sales, and real personal income. All values are scaled in order to compare them on a single axis.

Strong leading indicators such as the CFNAI and the Philly Fed Index have been weak for many months, and the deterioration in new orders has moved from a slowing of growth to outright contraction in recent months. In the order of events, a slowing in real sales, personal income, and personal consumption expenditure typically follows – these are called coincident indicators. These growth rates generally only weaken materially once a recession is in progress, and reach their highest correlation with recession about 6-months into the downturn. That’s what we’ve begun to observe over the past few months, adding to our impression that the U.S. joined a global (developed economy) recession during the third quarter of this year. The most lagging set of economic indicators includes employment measures, where I’ve frequently noted that the year-over-year growth rate of payroll employment lags the year-over-year growth rate of real consumption with a lag of about 5 months. As a result, the year-over-year growth rate in payroll employment reaches its highest correlation with recession nearly a year after a recession has started – another way of saying that it is among the last indicators to examine for confirmation of an economic downturn. All of that said, our concern about recession emphatically is not what drives our concern about the stock market here. In early March, our measures of prospective return/risk moved to the lowest 1% of historical data based on a broad ensemble of indicators and consistent evidence of market weakness following similar conditions in numerous subsets of historical data. Those conditions remain largely in place today. There’s no question that massive fiscal and monetary interventions have played havoc with the time-lag between unfavorable conditions and unfavorable outcomes in recent years, which prompted us back in April to introduce various restrictions to our hedging criteria (see below). Still, present conditions remain strongly negative on our estimates. Meanwhile, the stock market is not “running away” – at best, these interventions have allowed the market to churn at elevated levels. Only a month ago, the S&P 500 Index was below its level of March 2012, when our estimates shifted to the most negative 1% of the data, and was within about 11% of its April 2010 levels, which is the last time that our present ensemble approach would have encouraged a significant exposure to market risk. Notably, as of last week, an upward spike in long-term Treasury yields took market conditions to an overvalued, overbought, overbullish, rising yields syndrome – which has tended to be anathema to the stock market, even prior to the more limited downward bouts of recent years. Beyond that, a natural question is – if recession concerns don’t factor into our present defensiveness in the first place, why should we be concerned about recession at all, and devote so much analysis to this issue in the weekly comments? The first answer is that the foundation of this particular cyclical bull market has rested on the continuation of massive fiscal and monetary interventions, and a new recession would stretch those interventions to untenable limits (and to some extent already have), which should be of concern regardless of one’s stock market views. The second answer is that much of Wall Street’s overbullish sentiment, as well as its “valuation” case for stocks, rests on the continuation of record high profit margins that are largely an artifact of extreme government deficits and depressed personal savings (see Too Little To Lock In). A contraction in sales, coupled with a contraction in profit margins – which is what we presently expect – is likely to devastate the “forward operating earnings” case for stocks, and I continue to expect Wall Street to be blindsided by this fairly predictable outcome (as it was in 2001-2002, as it was in 2008-2009). The distortions we presently observe in the economy will have significant long-term costs, but it is entirely naïve to believe that these costs should be evident precisely at the point where the wildest distortions are taking place. Federal deficits presently support about 10% of economic activity, and the primary driver of improvement in the unemployment rate has not been job creation but a plunge in labor participation, as millions of workers drop out of the labor force. In a post-credit crisis environment, and particularly with Europe’s sovereign debt in question, it should be no surprise that the world has been willing to accumulate U.S. currency and Treasury debt at near-zero interest rates. That makes debt seem benign and money creation seem without consequence. But it is absurd to point at that happy short-term outcome and dance under the illusion that escalating debt won’t matter in the longer term, or that massive money creation will be easily reversed, or that strong inflation will be avoided if it is not reversed. We have already accumulated enough government debt to place a broad range of current and future government services under a cloud. Given that most of the publicly held U.S. government debt is of short maturity, there is no way of inflating away its real value over time, because interest rates would adjust at each rollover of that debt. In the event that the sheer size of the U.S. debt results in a loss of confidence (which is a 5-10 year proposition, though not yet a present one), there is no reason that we could not expect the same short-term funding strains that many European countries are facing in fits and starts today. Meanwhile, last week, Ben Bernanke announced that the current “Twist” program (where the Fed buys long-term Treasuries and sells an equal amount of shorter-dated Treasuries) will be replaced with outright “unsterilized” bond purchases. In doing so, Ben Bernanke has put the economy on course to choke down 27 cents of monetary base for every dollar of nominal GDP by the end of next year – in an economy where even the slightest normalization to interest rates of just 2% would require the monetary base to be cut to just 9 cents per dollar of GDP to avoid inflationary outcomes. The chart below is a reminder of where we are already. Understand that Fed policy now requires interest rates to remain near zero indefinitely, because competition from non-zero interest rates would reduce the willingness to hold zero-interest currency, provoking inflationary outcomes unless the monetary base was quickly reduced. Given an economy perpetually at the edge of recession, so far, so good. But as interest rates essentially measure the value that an economy places on time, Ben Bernanke's message to the U.S. economy is clear: time is worthless.

Monetary policy has become a roach motel, as Peter Schiff has remarked - easy enough to get into, but impossible to exit. Bernanke seems pleased to note that inflation presently remains low, but why shouldn’t it? In a structurally weak economy, velocity drops in exact proportion to new monetary base, with zero effect on real output or inflation. The problem is that Bernanke seems incapable of running thought experiments. Suppose the economy eventually strengthens at some point past 2013. At that point, the Fed would have to sell nearly $3 trillion of U.S. debt into public hands in order to reabsorb the money creation he claims “is only a temporary matter.” These sales would add to the stock of U.S. debt already held by the public, very likely while a significant government deficit is still in place. Such a sale would be, by two orders of magnitude, the largest monetary tightening in U.S. history. Is that possible to achieve without disruption? I doubt it. So instead, the Fed must rely on the economy remaining weak indefinitely, so it will never be forced to materially contract its balance sheet. To normalize the Fed’s balance sheet without contraction and get from 27 cents back to 9 cents of base money per dollar of GDP without rapid inflation, we would require over 22 years of suppressed interest rates below 2%, assuming GDP growth at a 5% nominal rate. Indeed, Japan is on course for precisely that outcome, having tied its fate 13 years ago to Bernanke’s experimental prescription (stumbling along at real GDP growth of less than 1% annually since then). Bernanke now sees fit to inject the same bad medicine into the veins of the U.S. economy. Of course, a tripling in the consumer price index would also do the job of bringing the monetary base back from 27 cents to 9 cents per dollar of nominal GDP. One wonders which of these options Bernanke anticipates. Psychotic. Big picture – my perspective remains unchanged: the long-term viability of the global economy is being increasingly wrecked by short-sighted policies focused on avoiding short-term economic adjustments, and at bottom, on avoiding the restructuring of unserviceable sovereign, mortgage and financial debt. Yet only that restructuring is capable of unchaining the economy from reckless past misallocations; only that restructuring is capable of unleashing robust new demand that would form the basis for sustainable economic activity and job creation. You either pull the bad tooth, or you provide every kind of pain killer and symptom reliever, and let the problem rot indefinitely. From an investment perspective, we know that the impact of quantitative easing both in the U.S. and abroad has generally been limited to a rally in stocks toward the highs of the prior 6-month period, in some cases moving as high as the monthly Bollinger band (2 standard deviations above the 20-month average). Given that the S&P 500 is within a few percent of its highs, and that conditions have already established an overvalued, overbought, overbullish, rising-yields conformation, much of the “benefit” of QE on stocks appears already priced in, as it has been since October when Bernanke effectively announced the present policy. The downside risk overwhelms the upside potential, in my view, but we can’t confidently rule out some amount of upside potential – which would still seem dependent on the avoidance of negative economic surprises. The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Only comments in the Fund Notes section relate specifically to the Hussman Funds and the investment positions of the Funds. Fund Notes As of last week, our estimates of prospective return/risk in stocks remained strongly negative, with a spike in long-term Treasury yields contributing to a syndrome of overvalued, overbought, overbullish, rising-yield conditions. Strategic Growth remains fully hedged, with a “staggered strike” position that places the strike prices of the put option side of our hedge within a few percent of present market levels, at a cost of about 1.5% of assets in put option premium looking out to springtime. Strategic International also remains fully hedged, though a reasonable combination of market outcomes (particularly a moderate market decline in the U.S. without a much deeper breakdown in international market action) could contribute to a constructive shift in our investment stance. Strategic Dividend Value remains hedged at about 50% of the value of its stock holdings – its most defensive stance. Strategic Total Return presently has a duration of just under 3 years (a 100 basis point move in yields would be expected to impact Fund value by about 3% on the basis of bond price fluctuations), having slightly boosted that duration in response to recent price weakness in Treasuries. The Fund also has about 15% of assets in precious metals shares, and just under 5% of assets in utility shares. Last week, I received a note from a shareholder essentially asking “what do you hope to accomplish in the Strategic Growth Fund?” Given the challenges of the most recent market cycle, that’s a fair question, and is one that I detailed in the 2012 Annual Report. What follows draws largely on the discussion on pages 7-9 (Notes on an extraordinary market cycle). Additional performance information and Fund reports can be found on The Funds page of the website. Put simply, our goal is to achieve strong returns over the complete market cycle (bull market and bear market combined), with smaller periodic losses than a passive “buy and hold” approach would experience. The Fund has often been hedged since its inception in 2000, so its performance has often appeared remarkable – relative to the S&P 500 – when measured from stock market peaks to market troughs, and less compelling when measured from market troughs to market peaks. Given the Fund’s objectives, we’ve always emphasized the importance of measuring performance instead over a complete market cycle – bull peak to bull peak, or bear trough to bear trough. Consider the performance of Strategic Growth Fund from a full-cycle perspective. From the inception of the Fund on 7/24/2000 to the peak to the bull market peak in the S&P 500 on 10/09/2007 (and including a full intervening bear market), Strategic Growth Fund achieved a cumulative total return of 119.79% (11.54% annually) compared with a total return of 20.70% (2.64% annually) for the S&P 500. The deepest intervening loss in Strategic Growth Fund was 6.98%, compared with a 47.41% intervening loss for the S&P 500. Measuring the complete cycle from the bear market trough on 10/09/2002 to the bear market trough on 3/09/2009, Strategic Growth achieved a cumulative total return of 37.95% (5.14% annually) compared with a cumulative loss of -1.25% (-0.20% annually) for the S&P 500. The deepest intervening loss in the Strategic Growth Fund during that period was 21.45%, compared with an intervening loss of 55.25% for the S&P 500. Note that one requires a gain of over 75% to turn a 55.25% loss to a 21.45% loss, so that reduction in maximum drawdown was no small difference [(1-.2145)/(1-.5525) - 1 = 75.53%]. Prior to 2009, I often began our annual and semi-annual reports with the remark that the Fund’s returns were “as intended” – neither disappointing nor extraordinary relative to my expectations or the historical research upon which our investment strategy is based. The recent cycle from the 2007 peak to the recent peak was different. While we correctly anticipated the 2008 market downturn and associated credit strains, the evidence began to deviate in major ways from anything observed in the U.S. post-war record on which our return/risk estimation methods rested. In my view, policymakers began to emphasize the protection of bondholders over the interests of the public. Signals from market action that had been reliable during the post-war period were less effective in late-2008 than in other post-war data, though we avoided the bulk of the downturn in any event. As we increasingly had to contemplate data outside of the post-war period, I insisted on stress-testing our methods against that data. Shareholders who aren’t familiar with our response to that period are encouraged to review the more detailed comments in the 2012 Annual Report, but the upshot is that we introduced two changes to our methods. One addressed what I called our “two data sets” issue (post-war data vs. Depression-era data), resulting in the ensemble methods we use at present. Unfortunately the continued uncertainty until that problem was solved led us to miss an intervening advance during 2009-early 2010. The second, smaller change was to address the effect of large and persistent monetary and fiscal interventions by adding additional restrictions to our criteria for using “staggered strike” hedge positions, which I introduced into our approach in April of this year. Nearly everything about the recent market cycle, including market behavior, economic impact, and policy response, has been extraordinary. The cost of these extraordinary outcomes, and our responses to them, is that in the period from the 2007 S&P 500 peak to the present, Strategic Growth Fund has lagged the total return of the S&P 500 by a cumulative 18% (-3.76% annually). Given that figure, had we captured a modest portion of the 2009-early 2010 market advance, there would be no such shortfall, and the churn of recent years might seem like little but a nuisance. My hope is that we'll observe numerous opportunities to recover that ground in the coming cycle. The problem, in my view, is that the “splice” created by that "two data sets" issue continues to create a misleading impression of our investment process. The most recent cycle (2007-present) features a correctly negative outlook approaching the 2007 peak, a negative outlook today, but the absence of an intervening constructive period in 2009-early 2010. The result is a seemingly interminable period of defensiveness – hence my miscast reputation as a “permabear,” and the incorrect assumption that our investment position will always be hedged. The essential feature of our investment approach is that we try to accept proportionately greater market exposure during periods when the prospective return/risk profile of the market is favorable, and proportionately less when the prospective return/risk profile is weak or negative, on our estimates. So in a typical market cycle, we would expect to be defensive in the overvalued, late-stage portion of a market advance, moving to a constructive or aggressive position once more reasonable valuations are coupled with an early improvement in market action, and eventually moving back to a defensive stance. If you examine the 2000-2007 cycle, you’ll see exactly that sequence – a pattern we also observe in numerous historical cycles. From the standpoint of our investment discipline, the “extraordinary” aspect of the most recent cycle for us was the absence of an intervening constructive period – concerns about Depression-like drawdowns took precedence until we were convinced that our methods were robust to that data. So what do I hope to accomplish in the Strategic Growth Fund? Simple. My hope is to achieve our investment objectives. My hope is that, having addressed the extraordinary challenges of the recent cycle, we will return to a performance profile that is “as intended” - reflective of the performance of our investment strategy in other market cycles that we’ve observed throughout history and since the inception of the Fund. Despite the challenges that we’ve addressed in this most recent cycle, I am as convinced as ever that our objectives remain achievable more generally. The standard caveats and disclosures apply, of course – past performance is not indicative of future returns, and there’s no assurance that we will achieve our investment objectives. Still, I am convinced that process matters; that stress-testing matters; and that historical evidence matters. Our investment process emphasizes comprehensive historical evidence and testing; it emphasizes performance over the complete market cycle; it emphasizes disciplined risk-management, especially with regard to deep losses; and it emphasizes the proportional exposure to market fluctuations as our return/risk estimates change. The recent cycle demanded two responses: an enhancement of our estimation methods in 2009-2010 to make our process robust to Depression-era outcomes, and a smaller change in our criteria for using staggered-strike option hedges, as monetary policy was too frequently aimed at creating free “put options” for investors. Still, the core of our investment discipline remains unchanged. Shareholders who understand our process will not be surprised if (and I expect, when) we remove all of the hedges in Strategic Growth at some point in the coming market cycle, or even add a few percent of additional exposure in call options. That is an event we would expect over the course of every market cycle. Those who understand our process will not interpret smaller shifts in our exposure as some indication of wild bullishness or a wholesale change in my investment thinking. We generally set our investment exposure proportional to the return/risk profile we estimate. Those estimates can turn positive for some period of time even during the course of a bear market. Given that I expect the next bear market low to achieve better valuations than the 2003 low (regardless of how it compares with 2009), I expect there’s a good chance that during the coming market cycle we will be able to remove more of our hedges than the 70% that we removed in 2003. At the same time, my hope is that investors who understand our process will recognize why we maintain our discipline here. I’m comfortable that our methods are robust not only as they apply to historical data, but also as they apply to the most recent market cycle. There are certainly points in the recent cycle where the investment stance encouraged by our present methods might have been different, but our present defensiveness in response to current market conditions is similar to the defensiveness we would have taken in numerous other market cycles. When investment conditions improve, we will shift our positions accordingly. The need to capture Depression-era data in our discipline was an extraordinary event, but that is fortunately an event that will occur exactly once. We also know what our performance has been when our discipline proceeds “as intended” – and I have every intent of continuing to pursue that discipline. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |