|

|

||||||

|

|

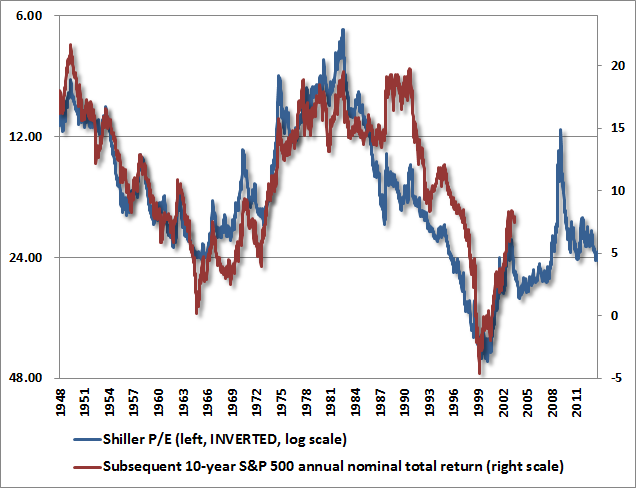

July 29, 2013 Baked In The Cake “I can feel it coming, S.E.C. or not, a whole new round of disastrous speculation... and finally the inevitable crash. I don’t know when it will come, but I can feel it coming, and, damn it, I don’t know what to do about it.” “The danger of mispricing risk is that there is no way out without investors taking losses. And the longer the process continues, the bigger those losses could be. That's why the Fed should start tapering this summer before financial market distortions become even more damaging.” The U.S. equity market is now in the third, mature, late-stage, overvalued, overbought, overbullish, Fed-enabled equity bubble in just over a decade. Like the 2000-2002 plunge of 50%, and the 2007-2009 plunge of 55%, the current episode is likely to end tragically. This expectation is not a statement about whether the market will or will not register a marginal new high over the next few weeks or months. It is not predicated on the question of whether or when the Fed will or will not taper its program of quantitative easing. It is predicated instead on the fact that the deepest market losses in history have always emerged from an identical set of conditions (also evident at the pre-crash peaks of 1929, 1972, and 1987) – namely, an extreme syndrome of overvalued, overbought, overbullish conditions, generally in the context of rising long-term interest rates. Despite individual features that convinced investors in each instance that “this time is different”, the corresponding handful of truly breathtaking market losses in history have a single source: the willingness of investors to forego the need for a risk premium on securities that have always required one over time. Once the risk premium is beaten out of stocks, there is no way out, and nothing that can be done about it. Poor subsequent returns, market losses, and the associated destruction of financial security (at least for the bag-holders) are already baked in the cake. This should have been the lesson gleaned from the period since 2000, but because it remains unlearned, it will also become the lesson of the coming decade. The coming 10-year period will likely include two or three bull markets, and two or three bear markets. Still, at the end of that decade, I expect that the S&P 500 Index will be little changed from its present level, having achieved an average annual total return of less than 3%, nominal, including dividends, with a number of deep interim market losses along the way. This isn't even a dire forecast. It's the central expectation based on valuation approaches that have a near-90% correlation with subsequent 10-year returns in close to a century of market data. With respect to the present, mature, overvalued, speculative half-cycle, I don't expect this cycle to be completed with a 20% loss, or a 25% loss, but instead a loss in the 40-55% range. Again - this isn't even a dire forecast. A 40% market loss is the central expectation. Even run-of-the-mill bear markets average a loss of about 32%, while run-of-the-mill cyclical bear markets in a secular bear context average a loss closer to 38%. It’s all well and good to say that the market advance since 2009 has fully recovered the 55% loss of the 2007-2009 bear market – as long as you also realize those gains. Otherwise, the recent market advance will ultimately be nothing but a forgotten parenthetical remark in a dismal investment story stretching from 2000 to some point late in this decade. I have particular concern about those who are coming into the market at these levels on the idea that the market is safe because it keeps going up. Bank of America notes that institutional investors have never dumped as much stock onto the public than they have in the past four weeks. Margin debt remains at historic levels, exceeding 2.3% of GDP for only the third time in history - the other two times, not surprisingly, being at the 2000 and 2007 market peaks. But aren’t stocks “cheap on forward operating earnings”? Isn’t the Shiller P/E (the S&P 500 divided by the 10-year average of inflation-adjusted earnings) distorted by recessions over the past decade? Let’s address these arguments directly. The Shiller P/E is now 24.4, about the same level as August 1929, higher than December 1972, higher than August 1987, but less extreme than the level of 43 that was reached in March 2000 (a level that has been followed by more than 13 years of market returns within a fraction of a percent of the return on Treasury bills – and even then only by revisiting significantly overvalued levels today). The Shiller P/E is presently moderately below the level of 27 at the October 2007 market peak. It’s worth noting that the 2000-2001 recession is already out of the Shiller calculation. Moreover, looking closely at the data, the implied profit margin embedded in today’s Shiller P/E is 6.3%, compared with a historical average of only about 5.3%. At normal profit margins, the current Shiller P/E would be 29. Below, I’ve presented the Shiller P/E versus the annual nominal total return of the S&P 500 over the following decade. The Shiller P/E is in blue (the left scale is an inverted log scale – I can’t understand why some analysts use a regular scale, which introduces nonlinearities). Subsequent S&P 500 total returns are in red. Even taken at face value with no other adjustments, the present Shiller P/E is more overvalued than it was at any point in history except 1929 and approaching the 2000 and 2007 market peaks (all which were, in fact, followed by dismal outcomes that wiped out every bit of intervening gain in excess of Treasury bill returns).

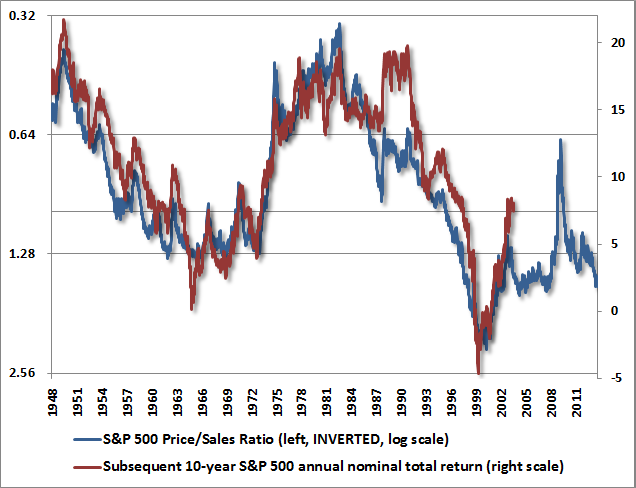

As an alternative measure (and there are several such measures that perform strongly across history, all with identical conclusions), the following chart presents the S&P 500 price/revenue multiple, (which implicitly normalizes profit margins – and for good reason: the resulting total return estimates are far more reliable than approaches that don’t account for margins). On this measure, the expected total returns for the S&P 500 over the coming decade are close to 2% annually, which – given a dividend yield of more than 2% even here – implies an S&P 500 Index in 10 years that is lower than it is today.

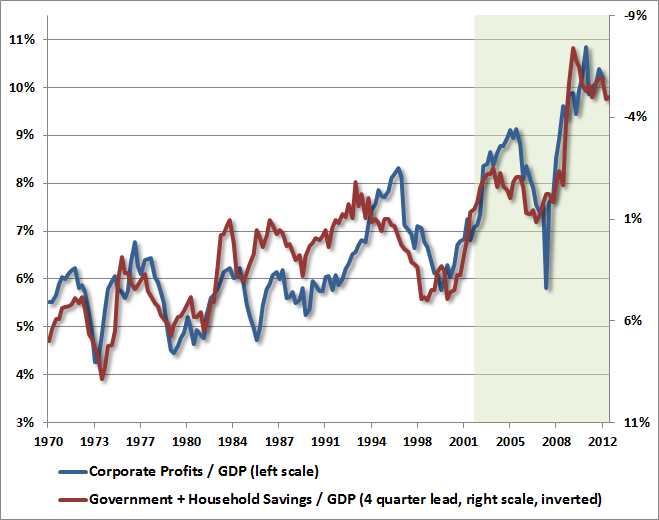

Again, this expectation - that the S&P 500 Index will be slightly lower than its present level a decade from today - isn't some dire, extreme, gloom-and-doom, low-probability event. It's the most likely outcome - the central expectation. Notice that both of the foregoing valuation approaches were quite favorable toward stocks in 2009. Whatever criticism one may have for my insistence on stress-testing against Depression-era data (when valuations similar to 2009 were followed by another two-thirds loss in the market), it should be clear that present valuations are nowhere near where they were in 2009, nor are the prospects for investors. Poor long-term market returns are now baked in the cake. As I’ve noted before, occasional deviations between actual and expected returns are informative. Actual returns in the decade following 1990 and 2003 exceeded expected returns precisely because stocks were so overvalued at the end of those 10-year spans (2000 and 2013). In turn, investors could – and can – expect poor returns over the decade following those overvalued points. Conversely, actual returns in the decade following 1964 fell short of expected returns precisely because stocks were so undervalued at the end of that 10-year span in 1974. In turn, investors could expect excellent returns over the decade following that undervalued point. Profit Margins and Forward Earnings Moving to forward operating earnings, it’s essential to remember that stocks are not a claim on a single year of income, but are instead a claim on a very long-term stream of future cash flows that will be delivered to investors over time. Using a single year of results as a metric is only appropriate if that single year of results can be considered a “sufficient statistic” that is representative of the entire future stream. At present, nothing could be further from the truth. Profit margins are 70% above historical norms. Why isn’t this representative or sustainable? Simple. Maintaining current profit margins would require recent post-crisis government deficits and suppressed household savings to be permanent. It’s an economic identity that savings (household, government, corporate and foreign) equal investment. It’s also true that in U.S. data, fluctuations in gross domestic investment move inversely with movements in the current account (what we call “foreign savings” in this context), which is why “improvements” in the trade deficit are almost always matched by “disappointments” in gross domestic investment over time. The resulting relationship boils down to a simple reality. Corporate profits move tightly and inversely to the combined sum of household and government savings. This is true in terms of levels. It is true in terms of changes over time. It is true over 4-year horizons. It is true over 10-year horizons. It is just a fact of economic accounting: the deficits of one sector must emerge, in equilibrium, as the surplus of another. The chart below shows this relationship.

Source data: Federal Reserve Economic Data (FRED): CPATAX/nominal GDP vs. I’ve added shading to emphasize the past decade. Notice that profits as a share of GDP over this period have averaged 8.3%, versus an average of just 5.8% prior to the most recent decade. Why? Historically, combined government and household savings have almost always been positive, averaging 4.8% of GDP. In the past decade, combined household and government savings have averaged a deficit of -2.5% of GDP. We are consuming more than our income, and financing it with debt. This has allowed corporations to maintain revenues despite the fact that workers are not, in aggregate, earning sufficient income to support that consumption. The combined deficit of households and government moved beyond -7% of GDP in mid-2009, and remained near this level for nearly three years. Only in the past two quarters has that combined deficit narrowed to less than -4% of GDP, and as indicated in the chart, there tends to be a modest 4-quarter lead until the full effect of those fluctuations appear in corporate profits. Interestingly, much has been made of the improvement in the government deficit in the first quarter. Indeed, the deficit across all levels of government shrank in the first quarter by $269 billion. Normally, one would have expected a sharp deterioration in corporate profits in response. But Wall Street is clearly thrilled that no such response has been observed. Looking more closely, we can see that this pleasant result is likely to be only temporary: the first quarter of 2013 saw one of the sharpest drops in household savings in history, with savings plunging by $349 billion to just 1.8% of GDP (one of the 12 lowest quarterly savings rates on record). Despite what would otherwise have been a “fiscal drag” on corporate profits, households dug into savings in order to maintain consumption, resulting in an even larger combined deficit than in the prior quarter. The problem here is that the fiscal drag will remain, but there is a very small likelihood that savings will remain so depressed. The fiscal drag has not been avoided, merely postponed. In August 2007, when Wall Street analysts were also arguing that “stocks are cheap on forward operating earnings” - just before the market plunged - I noted that this “valuation” approach, if one can even call it that, has an dismal long-term record, and a very weak association with subsequent returns (see Long Term Evidence on the Fed Model and Forward Operating P/E Ratios). Proponents of this approach tend to draw attention to individual data points rather than examining the full historical record. Investors should keel over in skepticism when analysts argue with a straight face that stocks are “cheaper” now than they were at the 2009 or 1982 lows, based on this or that adjustment to the data. In valuation work, proper “adjustments” to the data take only one form – they allow the model to better reflect the probable long-term stream of future cash flows that will be delivered to investors over time. As such, they should always result in a stronger correlation between the model’s valuation estimates and subsequent long-term investment returns. If an analyst can’t present decades (say 50-100 years) of data that demonstrate the link between their valuation approach and subsequent long-term (5-15 year) market returns, you are being sold something, not taught something. Most statements about market valuation on Wall Street are not implications of evidence, but evidence of ignorance. The same criticism, by the way, is true for estimates of “equity risk premiums” that rest on the use of forward operating earnings, and even those that rest on “growth rate plus dividend yield” arithmetic that implicitly assumes that prevailing yields will be sustained indefinitely even when they are extremely low. See Investment, Speculation, Valuation, and Tinker Bell for a comparison of several popular Wall Street approaches with several alternatives that actually do have a strong correlation with subsequent market returns. Recklessly as Any Amateur In short, we have one of the most overvalued, overbought, overbullish equity markets in history, but one where investors are under the illusion that stocks are appropriately priced, because they are being sold a valuation benchmark (forward operating earnings) that reflects profit margins 70% above historical norms – a direct result of unsustainably large deficits in combined government and household savings. As government deficits recede from the historic extremes that marked the post-crisis response to the worst economic downturn since the Depression, and household savings rebound from among the lowest levels in history, corporate profit margins cannot and should not be expected to persist at anywhere near recent record levels. A century of economic data provides evidence on both corporate profit margins and broader valuation measures. Wall Street is enthusiastic, once again, to argue that this time is different. I’m reminded of a decades-old passage from John Brooks, writing about the late-1960’s “Go-Go” market that ended with the 1969-70 plunge, and ushered in more than a decade of market weakness. Brooks was struck by the speculative recklessness of the time, even among those who should have known better. Didn’t the knowledge and integrity of Wall Street professionals protect the public? “Indeed, it had not – not when the nation’s most sophisticated corporate financiers and their accountants were constantly at work finding new instruments of deception barely within the law; not when supposedly cool-headed fund managers had become fanatical votaries at the altar of instant performance; not when brokers’ devotion to their customers interest was constantly being compromised by private professional deals or the pressure to produce commissions; and not when the style-setting leaders of professional investing were plunging as greedily and recklessly as any amateur.” Let’s be clear about something. Since 2000, the S&P 500 has achieved an average annual total return barely higher than 2% annually, and even then only by re-establishing overvalued levels at present. If there was any period since the Depression to be concerned about valuations and market risk, this has been the time – and it continues. Every valuation chart that I’ve shared in recent years should make it clear that the vast majority of history falls into a different class of valuations, a different set of prospective returns, and warranted a far more constructive investment stance than has characterized the period since 2000. Nobody who understands our investment discipline should doubt for a second our willingness, when appropriate, to advocate a constructive investment stance (e.g. 2003) or even a leveraged investment stance (as I did through much of the early 1990’s). It is worth repeating that though present conditions fall easily into the worst 5% of market history, conditions warranting a full hedge have historically occurred only about one-third of the time, while conditions warranting a leveraged position have historically occurred just over half of the time. I fear that investors may conclude that I’ve abandoned our risk-conscious investment discipline at the point in the coming market cycle that I advocate an aggressive investment stance. It’s worth observing now that conditions warranting such a position have historically been the norm and not the exception. In the context of a 13-year period of stock market returns averaging only about 2% annually, with two separate market losses of 50% and 55% in the interim, it's not entirely surprising to find good, risk-conscious value investors being mistakenly considered to be permabears. There’s no question that my fiduciary inclinations to stress-test against Depression-era data in 2009 resulted in a “miss” that our valuation measures and the resulting ensemble methods clearly could have captured. There’s no question that I’ve struggled with the distortions of quantitative easing. That’s partly because of an ingrained ethic – well supported by historical evidence – to pursue investment actions that will be of service to the economy rather than those that promise to do violence to it. When the Federal Reserve is hell-bent on doing violence by distorting financial markets, discouraging savings, and promoting speculation as a matter of policy – however well-intentioned that violence may be – we’re going to struggle some, because the eventual outcome of chasing an overvalued, overbought, overbullish market will be – and always has been – gruesome. Con Game Frankly, I still view QE as a confidence game that has no financial mechanism except to make investors uncomfortable holding Treasury bills, and no theoretically valid or empirically supported transmission mechanism to the real economy at all. I’m both surprised and a little bit disappointed that investors have again placed their confidence and financial security on what is the economic equivalent of a cheap parlor trick. Of course, as investors, the impact of QE has been quite real – even if it will ultimately be futile and destructive. Observing how loved the Fed has been at market tops, and how hated and blamed the Fed has been at bottoms, Bob Prechter aptly notes, “the Fed’s brilliance does not determine the market; the social mood behind the market determines the Fed’s brilliance.” Last week, Seth Klarman of Baupost observed “All these things that propel markets higher; that limit downside volatility; that drive perceptions of risk lower, sow the seeds for periodic collapses such as the one in 2008 that are far more devastating than would happen otherwise... Government effort to pump stocks higher is expensive and distortive. And if the impact will only be ephemeral, if what goes up is certain to come back down, then the consequence is bound to be increased volatility, more financial catastrophe, and possibly an endless cycle of propping up followed by collapse, perhaps with greater and greater amplitude and, looking back, ultimately without any purpose other than as a short-term palliative for psychological or political purposes.” To quote my friend John Mauldin, “We are watching the Fed employ a trickle-down monetary policy. They hope that if they pump up the banks and the stock market, increased wealth will lead to more investment and higher consumption, which will in turn translate into more jobs and higher incomes as the stimulus trickles down the economic ladder. The kindred policy of trickle-down economics was thoroughly trashed by the same people who now support a trickle-down monetary policy and quantitative easing. It is not working.” The challenges associated with QE have led us to narrow the set of conditions where our approach is defensive (in a way that can be validated as effective in other cycles across history), and to increase our responsiveness to trend-following considerations in the absence of overvalued, overbought, overbullish syndromes. Still, the recent market advance has not convinced us to try to “fix” our approach by simply chasing QE-induced speculation to the exclusion of all other evidence. This is largely because I am convinced that the effects of overvalued, overbought, overbullish conditions, particularly since September 2011, have been merely postponed by accumulating greater and greater downside risk. The historical record of the measures we follow, our successes, and our challenges in the extraordinary, unfinished speculative half-cycle since 2009 – all of these are an open book. This half-cycle is what it is, but it is also mature, strenuously overextended, and incomplete. For those who trust my judgment, I can tell you not only that we are far, far more inclined to encourage constructive and aggressive investment exposures over the course of the complete market cycle than casual observers may recognize – but I will also tell you that the stock market – here and now – is at a far, far more dangerous point in that cycle than investors can imagine. A final note – be aware that overvalued, overbought, overbullish periods often feature what I’ve called “unpleasant skew.” As I noted before significant corrections in 2010 and 2011: “If you look at overvalued, overbought, overbullish, hostile yield conditions of the past, you'll find that the most likely market outcome, in terms of raw probability, is a continued tendency for the market to achieve successive but slight marginal new highs. While this movement tends to be fairly muted in terms of overall progress, it can be somewhat excruciating for investors in a defensive position, because the market tends to pull back by a only a few percent, followed by bursts that recover that lost ground and achieve minor but widely celebrated new highs. That is the ‘unpleasant’ part. The ‘skew’ part is that although the raw probability tends to favor slight successive new highs, the remaining probability tends to feature nearly vertical drops, typically well over 10% over a period of weeks.” So for example, after a seemingly interminable series of marginal new highs, the initial decline off the market’s peak in late-April 2010 was a 2-week decline of about 9%. In 2011, a similar series of seemingly interminable new highs was followed by four consecutive down weeks containing a market loss of more than 16%. Both 2000 and 2007 had several such air pockets, including a 10.5% one-week decline in April 2000, just after the March peak in the S&P 500 of 1527.46 (the bull market high in index terms), and six consecutive down weeks containing a market loss of 10% following the September 2000 peak in the S&P 500 (the bull market high on a total return basis). As of Friday, the S&P 500 had advanced in 15 of the past 17 sessions. In the context of present overvalued, overbought, overbullish conditions, this is a familiar set-up. The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Only comments in the Fund Notes section relate specifically to the Hussman Funds and the investment positions of the Funds. Fund Notes As of last week, stock market conditions continued to reflect among the most strenuous overvalued, overbought, overbullish conditions that we have historically observed in our measures. I should be quick to emphasize that severity of conditions does not imply immediacy of outcomes (the rolling market tops of 2000 and 2007, for example, spanned close to 9 months). Still, from a return/risk standpoint, our present estimates are quite negative already, and our discipline is to align ourselves defensively in such environments. Strategic Growth remains fully hedged, with a staggered-strike position that places the strike price of the index put options side of its hedge near present market levels. Strategic International remains fully hedged. Strategic Dividend Value is hedged at about 50% of the value of its stock holdings. Strategic Total Return carries a duration of about 5.8 years (meaning that a 100 basis point move in interest rates would be expected to impact Fund value by about 5.8% on the basis of interest rate fluctuations), with about 6% of assets in precious metals shares and about 4% of assets in utility shares. I continue to view rising Treasury yields, suppressed inflation (for gold) and general equity risk as headwinds for precious metals and utilities stocks, despite our views that both sectors appear favorably valued. Our preference here is to accumulate on price weakness and reduced headwinds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |

{kind=link}