|

|

||||||

|

|

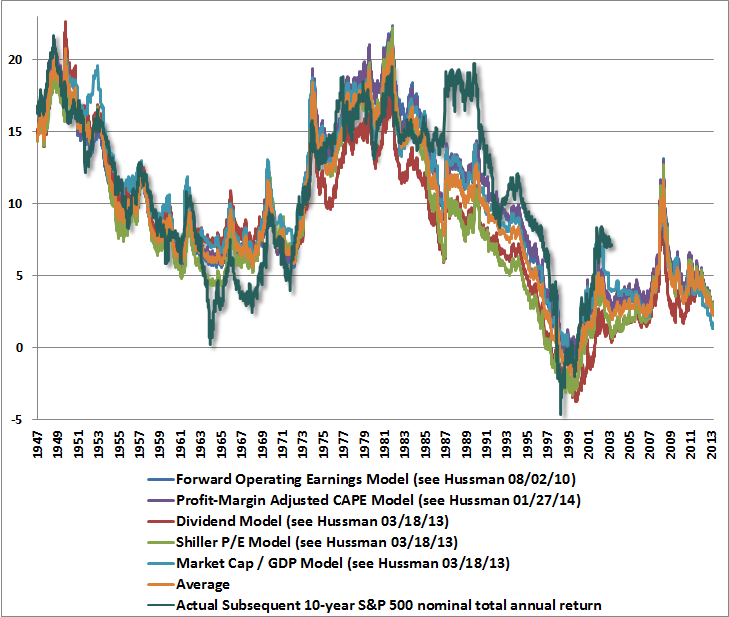

February 3, 2014 Pushing Luck Just a note - I'll be speaking at the Wine Country Conference in Sonoma, CA on May 1st & 2nd, 2014, along with Mike "Mish" Shedlock, David Stockman, Stephanie Pomboy, Steen Jakobsen, Chris Martenson, Mebane Faber, Jim Bruce and others. This year's conference will benefit high-impact programming for individuals on the autism spectrum and their families, primarily local efforts through the Autism Society of America. As many of you know, my 19-year old son JP has autism, so the cause is very close to my heart. Last year's conference benefited the Les Turner ALS Foundation. It's a great event in a beautiful location. Hope to see you there. For more information, please visit www.winecountryconference.com. Thanks - John The latest data from the NYSE shows equity margin debt at a new all-time high. Relative to GDP, the current 2.6% level was eclipsed only once – at the March 2000 market peak. In the context of the most extreme bullish sentiment in decades, and reliable valuation metrics about double their historical norms prior to the late-1990’s bubble (price/revenue, market cap/GDP, Tobin’s Q, properly normalized price/forward operating earnings, price to cyclically-adjusted earnings), we view present market conditions as dangerously speculative. Before it’s too late, I should note – as I also did at the 2007 market peak just before the market collapsed – that unadjusted forward operating P/E ratios and the Fed Model are both quite unreliable indications of value or prospective returns (see Long-Term Evidence on the Fed Model and Forward Operating P/E Ratios). Even the shallow 3% retreat from the market’s all-time highs may be enough to prompt a reflexive “buy-the-dip” response in the context of extreme bullish sentiment here, as the S&P 500 bounced off of a widely monitored and steeply ascending trendline last week that connects several short-term market lows over the past year. Regardless, the potential for short-term gains is overwhelmed by the risk of deep cyclical and secular losses. We presently estimate prospective 10-year S&P 500 nominal total returns averaging just 2.7% annually, with negative expected total returns on every horizon shorter than 7 years. Could the stock market’s valuation really be double its historical norm? Yes, this is presently the case for numerous historically reliable measures, including price/revenue, market cap/GDP, Tobin’s Q, and a variety of properly normalized earnings-based measures. [Geek’s Note: Think of the market’s overvaluation this way. Suppose that a security achieves a 10% long-term return when it is priced at “fair value,” and that the security is expected to trade at fair value X a decade from today. In order to achieve a 10% return over the coming decade (ignore dividends for a second), the security must be priced at X/(1.10)^10 = 0.386X today. Now suppose that the security is actually priced to achieve annual returns of just 2.7% over the coming decade. In that case, the price would be X/(1.027)^10 = 0.766X today. Of course 0.766/0.386 is 1.98, so at a 2.7% 10-year expected return, the price is 98% above the level at which the security would achieve a 10% rate of return. Alternatively, if one argues that a 5% annual rate of return would be perfectly acceptable for the next decade, it follows that the price should be X/(1.05)^10 = 0.614X. In that case, the security is only 25% overvalued at 0.766X. Indeed, if one argues that a 2.7% annual rate of return is perfectly acceptable, it follows that the security is appropriately priced at 0.766X. To say that we view stocks as strenuously overvalued is to assert that a 2.7% annual return for the S&P 500 over the next decade is unacceptable relative to the probable risks, even given currently depressed interest rates. But that’s how stocks are priced here. One can show that similar calculations apply in the presence of cash payouts. For example, begin with an arbitrary payout growing at 6% over time. Suppose that for a decade the expected total return k = 2.7%, with k = 10% thereafter. Under those assumptions, the security will be priced 82% above the level at which it would achieve a consistent 10% rate of return]. There are certain points in history where the projections of S&P 500 total returns have differed somewhat depending on which fundamental measure one uses. At present, a wide range of valuation methods that are actually historically reliable show very little variation. Uniformly, and across fundamentals that have reliably correlated with actual subsequent market returns, we project likely S&P 500 total returns in the range of 1-3% annually over the coming decade. Given a 2% dividend yield, this implies that we fully expect the S&P 500 to be no higher a decade from today than it is at present. These are, of course, the same methods that led us to correctly anticipate a decade of negative total returns in 2000, and significant market weakness in 2007. In contrast, note that these same methods were quite favorable toward equities in 2009 (our stress-testing concerns were not driven by valuations). A passive, equally balanced portfolio of stocks, bonds, and cash can be expected to return about 2% annually over the coming decade. If this seems to be an untenable long-term rate of return, understand that the security prices underlying those expected returns are equally untenable. Also, remember that historical evidence is sufficient to distinguish between competing valuation approaches.

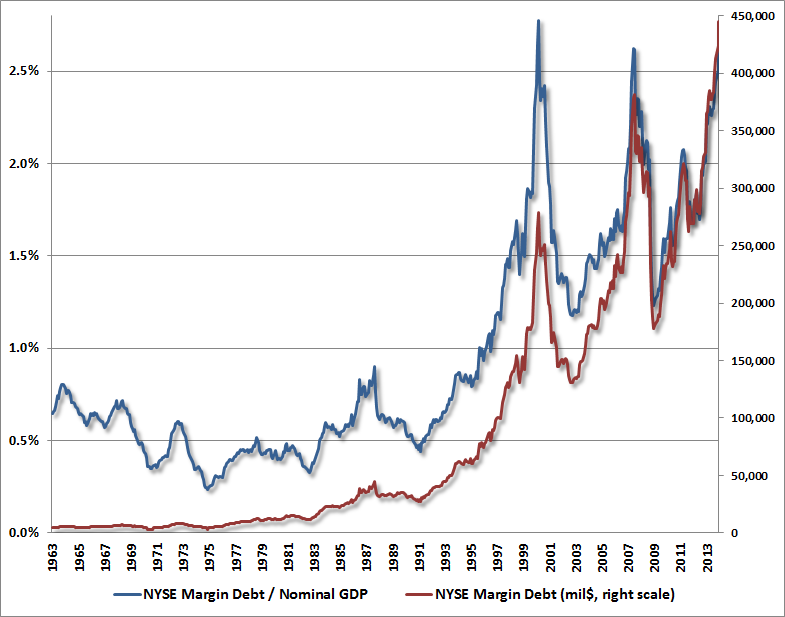

None of this ensures that stocks will decline rather than advance over the near term, but any expectation of adequate longer-term returns in equities from present valuation levels taxes the historical evidence. What accelerates our concerns is the extreme level of speculation in the present market environment. For example, the chart below shows NYSE margin debt both in dollar terms and relative to nominal GDP. We use GDP here because margin debt to GDP has a much higher correlation with actual subsequent market returns than say, margin debt / market capitalization (which destroys information by muting the indicator exactly at points when prices are extremely elevated or depressed). That said, the main usefulness of this measure isn’t for any fixed correlation with subsequent returns – numerous valuation measures do much better – but for its extremes. This is particularly true when margin debt advances rapidly over a span of several quarters relative to prices, GDP and other measures.

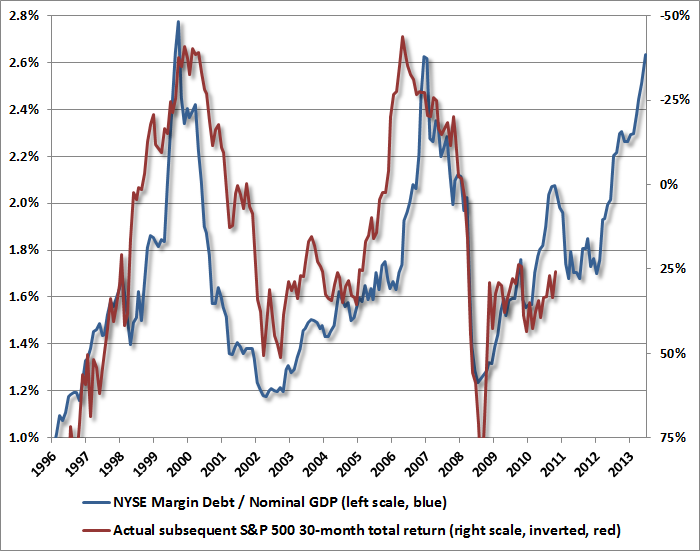

Points of rampant speculation on margin strongly overlap points of extreme bullish sentiment and extreme valuation. For that reason, and also because numerous valuation measures have a more direct relationship with subsequent market returns, margin debt is best used as a confirming indicator of cyclical market extremes. Prior spikes in margin debt / GDP in June 1968, December 1972, August 1987, March 2000, and October 2007 were followed by a bear market losses of at least one-third of market value shortly thereafter. A couple of peaks like 1978 and 1984 occurred at quite reasonable valuation levels, and were uneventful. The April 1964 spike is interesting in that it was uneventful over the near term, but the S&P 500 was lower even a decade later. My impression is that this result owes far more to the general overvaluation of the market in the mid-1960’s than it does to the elevated level of margin debt at the time. Of course the peaks are only observable after the fact. But it’s easy enough to define a spike as a significant advance from the prior low. The spikes that accompany extreme bullishness and rich valuation are most notable. Examine points in history where margin debt / GDP was more than 70% above its 5-year low, the 2-week average of advisory bulls exceeded 53% with bears less than 27%, and the price/peak earnings ratio was greater than 18 (price/peak earnings is the S&P 500 divided by the highest level of index earnings achieved to date – I created that measure a couple of decades ago and use it here because the Shiller P/E is presently spurned out of dislike for its implications). There are only five instances, all at or in the final few months preceding the market peaks of 1972, 1987, 2000, and 2007 (and of course today). With the caveat that pre-1990’s data does not normalize as well, the chart below shows the more recent relationship between margin debt/GDP and S&P 500 returns over the subsequent 30-month period (most historical spikes in margin debt/GDP have been followed by subsequent bear market troughs within that time-frame). Note that returns (red) are inverted, so higher points imply more negative outcomes. Of course, the red line ends 30 months ago.

Needless to say, there are endless arguments as to why this time is different, just as there were at each of those other peaks. The present, uncompleted half-cycle is being used to argue that historical full-cycle relationships no longer hold. It’s certainly true that quantitative easing has allowed the market to ignore even extreme variants of overvalued, overbought, overbullish conditions that have historically been resolved much more quickly. Similarly extreme conditions emerged in February and May of 2013 without consequence, and lesser variants have appeared sporadically for 2-3 years. There’s no question that the suspension of historical regularities in this uncompleted half-cycle has destroyed my credibility with those who don’t take historical evidence seriously in the first place – despite losing half of their assets in 2000-2002 and 2007-2009, and I expect will shortly do so again. Speculators have been luckier than they may realize, and are now pushing their luck. Still, nearly all of the current disputes about valuations, profit margins and so forth can be settled by an evaluation of the historical evidence. The unsettled arguments are the ones that require the present to depart from history against a century of evidence. There are two main beliefs here: that profit margins will remain elevated dramatically above norms that have been revisited in every cycle, including the two most recent ones; and that strenuously overvalued, overbought, overbullish conditions can be sustained indefinitely. These beliefs are identical to those in 2007 that we thought were settled by the 55% market plunge that followed. Investors have become speculators, and now rely on both, in the face of the same conditions that have repeatedly emerged at the most memorable market peaks in history. As I’ve frequently observed, such extremely overvalued, overbought, overbullish conditions often feature “unpleasant skew” – a tendency toward small, persistent market advances followed by very steep and abrupt declines that wipe out weeks or months of prior gains in one swoop. In the options market, recent prices have reflected the greatest amount of implied “skew” on record (measured using the difference in prices between significantly “out of the money” put options versus equally distant call options). The problem is always that historical outcomes are easy to observe in hindsight, but the outcome of the present instance is still unseen – even if the underlying conditions are the same. As we saw in 2000 and again in 2007, until unseen risks become observable reality in hindsight (and by then, it’s too late), all of these concerns are quickly dismissed and ignored by investors. Quantitative easing has distorted not only financial markets, but financial memory. The awakening is not likely to be gentle. The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Only comments in the Fund Notes section relate specifically to the Hussman Funds and the investment positions of the Funds. Fund Notes We continue to estimate prospective S&P 500 total returns of just 2.7% annually over the coming decade, with negative expected returns on horizons of less than 7 years. That said, valuations alone are not our concern. What concerns us is the combination of rich valuations with dramatically lopsided bullish sentiment, a steep and mature market advance, record NYSE margin debt (higher as a percentage of GDP than at any point except March 2000), and growing internal divergences in our measures of market action. Keep in mind that a 50% loss in the stock market (which has occurred twice since 2000) is roughly equivalent to losing 30% of one's assets, and then losing 30% yet again. None of the Hussman Funds, including Strategic Growth, has experienced a 30% loss even once since inception - our worst loss in Strategic Growth has been nowhere near what the market has repeatedly experienced. That's not to suggest that outcome as impossible, but we occasionally receive notes that fail to take Fund distributions into account. For example, the value of an investment in Strategic Growth since 2007, including reinvested distributions, is nearly 20% greater than one might infer if those distributions are ignored. There's no question this speculative episode has been frustrating, and we have our own ground to recover. But that ground is less than the market itself has repeatedly needed to recover from its own bear market losses. It's just that bear markets for us don't necessarily coincide with bear markets for everyone else. I should also observe that we have no reservations about entirely removing our hedges at the point where a significant in valuations meets an early improvement in market action. Our present defensiveness is a response to market conditions that have historically been strikingly hostile to investors. The necessity of stress testing against the possibility of Depression-era outcomes in 2009-early 2010 may have left a misleading impression about how our investment stance can be expected to evolve over future market cycles. Looking over history, our investment approach would easily have supported an aggressive investment stance more often than a hedged one. One must remember that the period since 2000 is one where the S&P 500 has struggled even to achieve a 3% total return, and has lost half its value - twice - in the interim. I have strong concerns that such a loss is again likely. Still, we have no downside target that must be achieved, nor do we require a move to undervaluation to justify a significantly invested stance. A good example is early 2003, when we removed 70% of our hedges in Strategic Growth despite valuations that were objectively still rich. Despite our awkward stress-testing transition in the uncompleted half-cycle since 2009, we manage risk with the objective of significantly outperforming a passive investment strategy over complete market cycles. The full-cycle objectives of the Hussman Funds are only suitable for investors who can tolerate periods where our returns do not "track" general market fluctuations. We strongly encourage investors who share a full-cycle perspective and an appropriate tolerance for "tracking risk" to stay this course, particularly near what we believe is the end of a remarkably speculative market advance. The Hussman Funds remain strongly defensive toward equities, and are only modestly constructive toward bonds and precious metals shares here. Risk concerns predominate, and we believe the present market cycle will create far better opportunities to accept market risk at significantly higher prospective returns per unit of risk. At present, we estimate that a passive, equally-weighted portfolio of stocks, bonds, and cash can be expected to return only about 2% annually over the coming decade, from current prices. We don’t view this situation as tenable for much longer, particularly in equities. It follows that we don’t view current prices as tenable either. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |