|

|

||||||

|

|

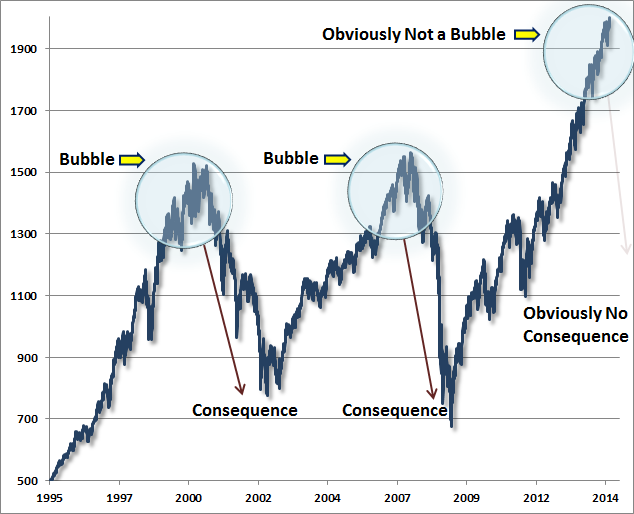

September 8, 2014 The Two Pillars of Full-Cycle Investing Despite my reputation in recent years as a “permabear,” I’ve actually had quite a variable relationship with equity risk across three decades in the financial markets, and that relationship has always depended on market and economic conditions. It’s difficult to judge stocks as “good” or “bad” investments without reference to valuations and other factors. For example, after the 1990 bear market, I had a reputation as a “lonely raging bull” and advocated a leveraged stance in equities for years, based on a combination of reasonable valuation and strong market internals. While investors worried about weak consumer confidence, I frequently noted that weak confidence is correlated with strong subsequent market returns. It’s the combination of high confidence, lopsided bullishness, overvaluation, and overbought multi-year advances that opens a chasm into which the market ultimately plunges. History is remarkably consistent on this point, and it requires discipline to avoid that damage. Reducing exposure to risk in these conditions the first pillar of full-cycle investing. Accordingly, I was no fun at all by the 2000 market peak. It was impossible to justify equity valuations except on assumptions that were wholly outside of historical experience. We keep a talking Pets.com sock puppet in the office as a reminder of that bubble. A little squeeze and he says things like “Hey, you’re a good lookin’ fella. I like your shorts.” By the time the 2000-2002 decline partially unwound the bubble, the S&P 500 had lagged Treasury bills all the way back to May 1996. As I’ve often observed, the best time to accept market risk is when a material retreat in valuations is coupled with an early improvement in market action across a range of market internals, industry groups and security types. On that basis (and even though valuations were still rich from a historical perspective), we removed the majority of our hedges in early 2003 as a new bull market took off. I actually got complaints as some investors thought I had somehow abandoned our discipline. Please understand this now so that you are not surprised later: shifting to a constructive or leveraged position following a material retreat in valuations, coupled with an early improvement in market action, is part of our discipline. Accepting exposure to market risk in these conditions is the second pillar of full-cycle investing. Not surprisingly, the combination of high confidence, lopsided bullishness, overvaluation, and an overbought multi-year advance made me again no fun at all by the 2007 peak. The narrative of what followed was the same – by the time the market bottomed in early 2009, the decline had wiped out the entire total return of the S&P 500 – in excess of Treasury bills – all the way back to June 1995. It’s at that point that I made the decision that sent my reputation to hell, at least for the advancing portion of the current cycle. As economic and financial losses during the crisis stopped resembling anything observed in post-war data, and began to resemble Depression-era outcomes much more closely, I insisted on stress-testing our methods against that data. Our existing methods of classifying market return/risk profiles (which were based on post-war evidence) did well in that Depression-era data overall, but experienced more whipsaws and far deeper interim losses than I was willing to contemplate in real-time. In hindsight, the main outcome of those stress-tests was that more demanding variants of what we call “early improvement in market action” were needed to navigate Depression era outcomes. The trouble with hindsight, of course, is that we identified that distinction too late to benefit from it. Our post-war measures of market action had encouraged us to respond constructively in late-October 2008 after the market plunged (as I observed at the time, on a material retreat in valuations coupled with early improvement in market action – see Why Warren Buffett is Right and Why Nobody Cares). The stress-tested ensemble methods that ultimately resulted would have deferred that response to early-2009. But in the interim of that “two data sets” uncertainty and stress-testing, we entirely missed the 2009-2010 opportunity to do what we have done in past market cycles, and expect to do in every future market cycle, which is to shift to a constructive or leveraged position following a material retreat in valuations, coupled with an early improvement in market action. Which brings us to the present, when I have again become no fun at all, largely because of a combination of high confidence, lopsided bullishness, overvaluation, and an overbought multi-year advance. There’s no question that the absence of consequences – to date – has led investors to believe that those consequences simply will not emerge. Once the consequences arrive, the preceding bubble seems obvious, but it’s a regularity of history that speculative episodes are only completely clear in hindsight. The following chart is a reminder of where we stand. The index is the S&P 500.

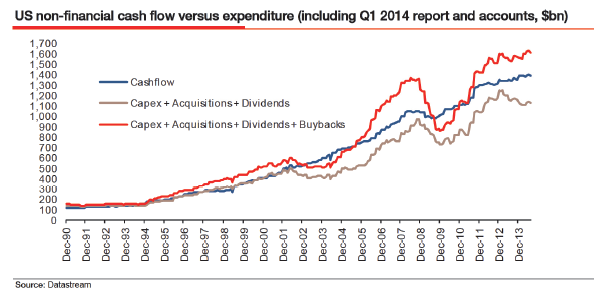

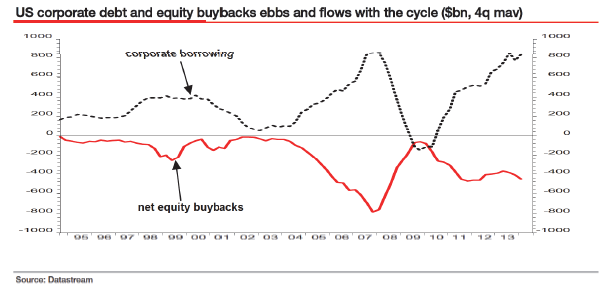

History teaches clear lessons about how this episode will end – namely with a decline that wipes out years and years of prior market returns. The fact that few investors – in aggregate – will get out is simply a matter of arithmetic and equilibrium. The best that investors can hope for is that someone else will be found to hold the bag, but that requires success at what I’ll call the Exit Rule for Bubbles: you only get out if you panic before everyone else does. Look at it as a game of musical chairs with a progressively contracting number of greater fools. Why won’t most investors get out? The answer is that in equilibrium, they can’t. On any given trading day, only a fraction of 1% of total market capitalization changes hands, and the vast majority of that is high-frequency trading and portfolio reallocation between existing equity holders. Think about it – the only way for an investor to get out of stocks without someone else getting in is for the stock to be literally removed from the market. That source of net removal of stock is corporate repurchase activity, which recently hit a year-over-year pace of about $500 billion. That’s still less than 4% of total market cap in an entire year, and it’s a fairly good upper limit on the percentage of investors who will successfully get out of this bubble without the appearance of a miraculous multitude of greater fools at the very moment existing holders decide to sell. Notably, the heaviest repurchase activity is associated with market peaks – repurchases actually dwindle at market lows. As our friend Albert Edwards across the pond in England points out, corporate cash flow alone is not enough to finance buybacks and other corporate expenditures, so buybacks are instead typically funded primarily through debt issuance. When you recognize that most corporate debt has a maturity of less than 8 years and that market valuations presently imply negative total returns for the S&P 500 over this horizon by our estimates, we believe that corporate repurchases are doing violence, not good, to investors. Moreover, a good chunk of repurchases are used to offset dilution from stock and option grants to corporate insiders. This is like someone saying, “Hey! I made you a pizza!” and then eating that pizza right in front of you.

Notice that heavy equity buybacks (negative values on the red line below) are regularly financed by the issuance of corporate debt (a mirror image of positive values on the black line). Those debt-financed equity buybacks have been heaviest at market peaks like 1999-2000, 2007, and today. Put simply, the history of corporate stock buybacks is a chronicle of corporations buying stock with borrowed money at market tops, and retreating from buybacks at the very points that stocks are most reasonably valued.

In any event, the reason most investors won’t get out of this bubble is that it will require other investors to get in by taking the stock off their hands – and with bearishness running at the lowest level in 27 years, those potential buyers increasingly represent value-conscious investors like us whose demand is likely to emerge only at materially lower valuations. The good news here is that history also provides every reason to believe that we will encounter repeated opportunities where a material retreat in valuations is coupled with an early improvement in market action. That’s an opportunity that we clearly missed in the most recent market cycle, and my fiduciary inclinations to stress-test our methods clearly did not serve us well under the illumination of hindsight. But one should also remember that to experience a 55% loss, as the S&P 500 did during 2007-2009, one must first lose 30% of one’s funds, and then follow that with an additional loss of over 35%. We don’t intend to take a bath anywhere near what buy-and-hold investors have to brace themselves to endure. Last week, Investors Intelligence reported that the percentage of bearish advisors has dropped to a 27-year low of 13.3%, a level last seen in 1987 a few months prior to the market crash of that year. Needless to say, investors do not like to hear cautious voices in a speculative market that rewards the absence of caution. We’ve seen a few fairly rude attack pieces by guys who themselves were saying “just buy the market, and wait” at the 2000 peak, and “ignore the calls to action you hear” at the 2007 peak. Though my teenage daughter calls these postings “cyberbullying for adults,” those pieces (minus the incivility) are understandable if one misreads our experience since 2009. That narrative can be understood in context of the two pillars: my stress-testing response to the “two data sets” problem between post-war and Depression era data in 2009 resulted in our missing the best opportunity in this cycle to follow one of those pillars – shifting to a constructive or leveraged position following a material retreat in valuations, coupled with an early improvement in market action. Meanwhile, we are patiently and deliberately adhering to the other pillar – avoiding market risk in the face of an extreme combination of high confidence, lopsided bullishness, overvaluation, and an overbought multi-year advance. The splice of those two invites an oversimplified impression that we are simply permabears. Given that the predictable market losses that follow bubble conditions also have uncertain timing, it’s natural for many to believe that those consequences will simply not arrive. We know that most dismissed those same concerns in 2000 and 2007. I actually agree very much with the principle that investors committed to a buy-and-hold discipline should stick to that discipline through thick and thin. It’s just that they should understand that “thin” is likely to include another market loss on the order of 40-55% in the next few years, and that the percentage of assets allocated to passive buy-and-hold investments should be aligned with how soon they will need to spend the funds. The S&P 500 presently has an estimated duration of about 50 years, so investors who expect to spend their assets an average of about 15 years in the future should probably not have more than about 30% of assets in unhedged equities. Investors with a 50 year horizon, or who expect to add significant new amounts to their investments over time, can reasonably have a larger allocation. Long-term investors should also recognize that on the basis of historically reliable valuation measures, we estimate 10-year nominal total returns for the S&P 500 of only about 1.5% annually from current prices, so given a 2% dividend yield, we actually expect the index to be lower a decade from now than it is today (see Ockham's Razor and the Market Cycle for a review of these measures). As value investor Howard Marks observed last week: “Today I feel it’s important to pay more attention to loss prevention than to the pursuit of gain. Although I have no idea what could make the day of reckoning come sooner rather than later, I don’t think it’s too early to take today’s carefree market conditions into consideration. What I do know is that those conditions are creating a degree of risk for which there is no commensurate risk premium.” So while many observers pronounce victory at halftime, in the middle of a market cycle, at record highs and more extreme market valuations than at any point except the 2000 peak, remember the two pillars. First, the combination of high confidence, lopsided bullishness, overvaluation, and overbought multi-year advances has predictably been resolved by steep market losses, time and time again across history. Second, strong market return/risk profiles warranting constructive or leveraged investment positions emerge in every market cycle, generally following a material retreat in valuations, coupled with an early improvement in market action. We believe that one of these is descriptive of present market conditions, and the other is well worth our patience. The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Only comments in the Fund Notes section relate specifically to the Hussman Funds and the investment positions of the Funds. Fund Notes The Hussman Funds remain defensive toward equities, and are mildly constructive toward Treasury bonds and moderately constructive toward precious metals shares. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |