|

|

||||||

|

|

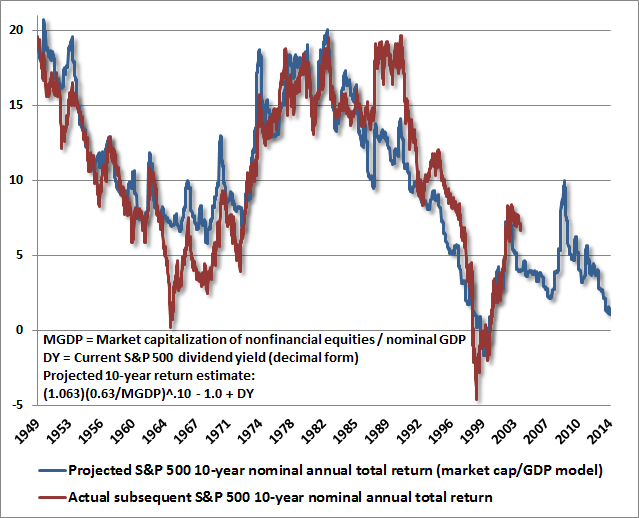

September 15, 2014 A Warning from Graham and Dodd “During the latter stage of the bull market culminating in 1929, the public acquired a completely different attitude towards the investment merits of common stocks... Why did the investing public turn its attention from dividends, from asset values, and from average earnings to transfer it almost exclusively to the earnings trend, i.e. to the changes in earnings expected in the future? The answer was, first, that the records of the past were proving an undependable guide to investment; and, second, that the rewards offered by the future had become irresistibly alluring. “Along with this idea as to what constituted the basis for common-stock selection emerged a companion theory that common stocks represented the most profitable and therefore the most desirable media for long-term investment. This gospel was based on a certain amount of research, showing that diversified lists of common stocks had regularly increased in value over stated intervals of time for many years past. “These statements sound innocent and plausible. Yet they concealed two theoretical weaknesses that could and did result in untold mischief. The first of these defects was that they abolished the fundamental distinctions between investment and speculation. The second was that they ignored the price of a stock in determining whether or not it was a desirable purchase. “The notion that the desirability of a common stock was entirely independent of its price seems incredibly absurd. Yet the new-era theory led directly to this thesis... An alluring corollary of this principle was that making money in the stock market was now the easiest thing in the world. It was only necessary to buy ‘good’ stocks, regardless of price, and then to let nature take her upward course. The results of such a doctrine could not fail to be tragic.” Benjamin Graham & David L. Dodd, Security Analysis, 1934 Fourteen years ago, the S&P 500 reached what still stands as its most overvalued point in history. At the time, on the basis of a variety of valuation measures, we projected negative 10-year total returns for the S&P 500 over the following decade, even under optimistic assumptions. The general arithmetic behind these estimates is detailed in Ockham's Razor and the Market Cycle. The ratio of market capitalization to GDP reached 1.54 in 2000, which also offered a reasonably good indication of likely prospective total returns for the index over the decade to come. A fairly simple rule-of-thumb using market capitalization to GDP is presented in The Federal Reserve’s Two Legged Stool. In 2000, that rule-of-thumb estimate of prospective S&P 500 10-year nominal annual total returns would have been: (1.063)(0.63/1.54)^(1/10) – 1.0 + .011 = -1.7% annually. As is generally the case over time (though not always over short horizons), these estimates worked out swimmingly. By 2010, even after an 80% rebound from the March 2009 low, the S&P 500 had still posted a negative total return from its 2000 peak. While investors presently dismiss the potential for valuations to remain well-correlated with actual subsequent market returns, and there’s no assurance that they will, the foregoing rule-of-thumb has historically had a nearly 90% correlation with S&P 500 nominal total returns over the following decade. The chart of this relationship (from the April 21 comment) is shown below. Note that secular valuation lows as we saw in 1949 and 1982 have generally occurred at levels that have implied near-20% annual 10-year total returns for the S&P 500. The 2009 low was certainly a great improvement from the 2000 extreme, bringing prospective 10-year returns to about 10% annually (and slightly higher on several other reliable valuation measures), but current valuations are no longer consistent with prospective 10-year returns anywhere near those levels.

At present, even assuming nominal GDP growth of 6.3% over the coming decade, the same estimate of prospective 10-year S&P 500 nominal annual total returns based on market capitalization to GDP works out to: (1.063)(0.63/1.34)^(1/10) - 1.0 + .020 = 0.5% annually. Based on a broader set of historically reliable valuation methods, our consensus estimate is closer to 1.5% annually. Given a dividend yield of 2% for the S&P 500, it follows that we expect the S&P 500 Index to be lower a decade from now than it is today. A legendary value investor, Benjamin Graham insisted that "operations for profit should be based not on optimism but on arithmetic." Careful arithmetic is important in order to resist the temptation to rely on what Graham called "some generalized statement, sound enough within its proper field, but twisted to fit the speculative mania." For example, many investors casually dismiss valuations today by parroting "lower interest rates justify higher valuations." But they do so without doing the associated arithmetic, and without recognizing that even those higher "justified" valuations will still be associated with poor subsequent equity returns. As I detailed in Optimism versus Arithmetic, if we assume that short-term interest rates will remain at zero for another 3-4 years instead of a more normal 4%, one can justify stock valuations 12-16% above where they otherwise might be. That 12-16% elevation would in turn shave about 4% annually from equity returns over that same 3-4 year perod. Unfortunately, the most reliable valuation measures we identify are more than double pre-bubble historical norms, so the "justified valuation" argument is exactly the sort of twisted statement that Graham warned about. The fact is that the most reliable valuation measures we identify are generally within just 15-20% of their 2000 extremes, and are already at or beyond levels observed in 1929, 1972, and 2007. Of course, that same advance to extreme overvaluation is also what has raised the total return of the S&P 500 from 2000 until today up to about 3.9% annually. We believe that even that total return is transitory, and presently estimate negative total returns for the S&P 500 on every horizon less than 8 years. It’s useful to understand that it was Graham and Dodd that originated the practice of normalizing earnings over the business cycle, which is a practice embedded in the most historically reliable valuation measures we identify. You’ll repeatedly see the phrase “average earnings” in their discussion of earnings power. As Roger Lowenstein observes: “In estimating future earnings (for any sort of business), Security Analysis provides two vital rules. One, as noted, is that companies with stable earnings are easier to forecast and hence preferable. The world becoming more changeable, this precept might be modestly updated, to wit: the more volatile a firm’s earnings, the more cautious one should be in estimating its future and the further back into its past one should look. Graham and Dodd suggested 10 years. The second point relates to the tendency of earnings to fluctuate, at least somewhat, in a cyclical pattern. Therefore, Graham and Dodd made a vital (and oft-overlooked) distinction. A firm’s average earnings can provide a rough guide to the future; the earnings trend is far less reliable. But investors get seduced by the trend; perhaps they want to be seduced, for as Graham and Dodd observed, ‘Trends carried far enough into the future will yield any desired result.’” Indeed, Graham and Dodd cite this sort of seduction as one of the central factors leading up to the 1929 bubble peak and subsequent crash: “That the average earnings had ceased to be a dependable measure of future earnings must indeed be admitted. But it does not follow at all that the trend of earnings must therefore be a more dependable guide than the average; and even if it were more dependable, it would not necessarily provide a safe basis, entirely by itself, for investment... the value placed upon a satisfactory trend must be wholly arbitrary, and hence speculative, and hence inevitably subject to exaggeration and later collapse.” The renaissance of “buy-and-hold regardless of price” The uncorrected half-cycle advance since 2009 has been accompanied by a resurgence of proponents advocating that stocks should simply be bought and held indefinitely, regardless of price. Some of these proponents have also used this mid-cycle victory-at-halftime as an opportunity to be rather impolite about it. On this subject, Graham and Dodd offer a useful warning in their 80-year old masterpiece, Security Analysis, speaking about the advance to the 1929 peak (whose valuations the present speculative episode has already matched or surpassed): “Irrationality could not go further; yet it is important to note that mass speculation can flourish only in such an atmosphere of illogic and unreality. The self-deception of the mass speculator must, however, have its element of justification. This is usually some generalized statement, sound enough within its proper field, but twisted to fit the speculative mania... In the new-era bull market, the ‘rational’ basis was the record of long-term improvement shown by diversified stock holdings. There was, however, a radical fallacy involved in the new-era application of this historical fact. This should be apparent from even a superficial examination of the data contained in the small and rather sketchy volume from which the new-era theory may be said to have sprung. The book is entitled Common Stocks as Long Term Investments, by Edgar Lawrence Smith, published in 1924. “In fact their rush to take advantage of the inherent attractiveness of common stocks itself produced conditions entirely different from those which had given rise to this attractiveness and upon which it basically depended [viz. much lower starting valuations in previous years]... But as soon as the price was advanced to a much higher price in relation to earnings, this advantage disappeared, and with it disappeared the entire theoretical basis for investment purchases of common stocks.” I have no intention to throw stones at buy-and-hold advocates. We’ve certainly had our own stumbles in the half-cycle since the 2009 low, partly because of my 2009-2010 insistence on stress-testing our approach against Depression-era outcomes, and partly because overvalued, overbullish, overbought syndromes that have been a crucial warning in prior market cycles have persisted much longer without consequence in this (spectacularly distorted) cycle, as a result of Fed-induced yield-seeking speculation. Still, we do encourage buy-and-hold investors to understand and mentally prepare for the potential depth of interim losses inherent in that strategy (we would presently allow 40-55%). We also urge investors to align the proportion of assets in equities with the date that they’ll actually need the money. For funds that will be spent an average of 15 years into the future, with no new investment contributions, we believe that passive equity holdings should not exceed 30% of assets, in order to match those expenditures with the duration of assets that must finance them (the S&P 500 presently has an estimated duration of about 50 years). While we believe there is some scope for active equity holdings, provided that market exposure is varied in proportion to expected market returns, this is typically not a component of passive buy-and-hold investing, and even if it were, we would suggest that expected returns are not even positive at horizons less than 8 years, and we estimate only very low single-digit total returns for the S&P 500 even over a 15-year horizon from current valuations. Following Graham, we go back to the importance of arithemetic in understanding why buy-and-hold strategies regularly reach their height of popularity at moments like the present. The returns that major stock market indices achieve over time can be reliably understood from the standpoint of where valuations stand at the start of a given window, and where they are at the end. At extremely elevated valuations, as we presently observe (on measures that are actually historically reliable), the past total returns of a buy-and-hold approach will always look quite favorable, because the backward-looking performance window ends at a quite favorable point. But this also generally means that the forward-looking performance window starts at the worst possible point, and unless valuations also happen to be elevated at the end of that window, future total returns are likely to be quite disappointing. From this perspective, it is only because present valuations are so extreme that the total returns of the S&P 500 since the similarly extreme 2000 peak have worked out to be even modestly positive, at about 3.9% annually. We would suggest that this is a temporary artifact of severely elevated valuations at both the start and end of the 2000-2014 window. Whatever benefits investors perceive from the extreme elevation of mid-cycle valuations today are likely to be transitory. Following a largely uncorrected multi-year diagonal advance, it's exactly the illusion that risk is riskless and elevated valuations have reached a "permanently high plateau" that does so much violence to investors over the completion of the market cycle. It's a regularity that prompted me to quote from the Wallace Stevens poem Sunday Morning as the market approached the 2007 peak: Does ripe fruit never fall? Or do the boughs As in every cycle, we expect there will be very good opportunities to establish constructive or even aggressive exposure to market fluctuations, typically at the point that a material retreat in valuations is coupled with an early improvement in market internals. In the half-cycle since 2009, we admittedly missed those opportunities in the interim of our stress-testing response to the financial crisis. The absence of any material consequence of increasingly extreme overvalued, overbought, overbullish conditions – largely driven by speculative yield-seeking in response to quantitative easing – has been equally humbling. Those stress-testing considerations are behind us, and we’ve adapted to the potential for recurrent Fed-induced speculation in ways that we certainly expect to be evident as the present cycle is completed and future ones unfold. But what can actually be expected to be a predominantly bullish bias to our investment discipline is simply not going to be evident at an overvalued, overbought, overbullish extreme like we observe at present. I can only say that investors who view me as a permabear understand nothing about our discipline if they fail to understand the context behind our experience in the half-cycle since 2009. Now, if one wishes to cite our experience during the half-cycle since 2009 as a justification to ignore overvalued, overbought, overbullish extremes indefinitely, that’s actually both welcome and useful, as someone will have to hold stocks through the completion of the present cycle. It’s best for those bag-holders to be people who have at least evaluated and voluntarily dismissed our concerns. Persistent and unconditional bullishness allows other investors – particularly those with short investment horizons – some window of opportunity to defend capital and reduce their portfolio risk to appropriate levels. Frankly, we’re not looking for investors to agree with us, or even to convert to our investment discipline. Our approach has always been to speak our truth clearly, and to do our utmost to maintain and encourage a value-conscious, historically-informed, risk-managed investment discipline for those who trust our efforts. Despite fiduciary stress-testing inclinations that, in hindsight, were not helpful during this half-cycle, we’ll let time sort out the misperceptions that investors have adopted in recent years about valuations, speculation without consequence, and even the inherent bullishness or bearishness of our own approach. Meanwhile, we don't require an epic market loss in order to justify a shift to greater market exposure, and we expect that a significant portion of future opportunities will be on the constructive side (particularly once a material retreat in valuations is coupled with an early improvement in market internals). Here and now, however, we do remain concerned that there is a cliff at the edge of what appears to be a permanently high plateau. The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Only comments in the Fund Notes section relate specifically to the Hussman Funds and the investment positions of the Funds. Fund Notes As of last week, the Hussman Funds remain defensive toward equities, and are moderately constructive toward Treasury securities and precious metals shares. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |