|

|

||||||

|

|

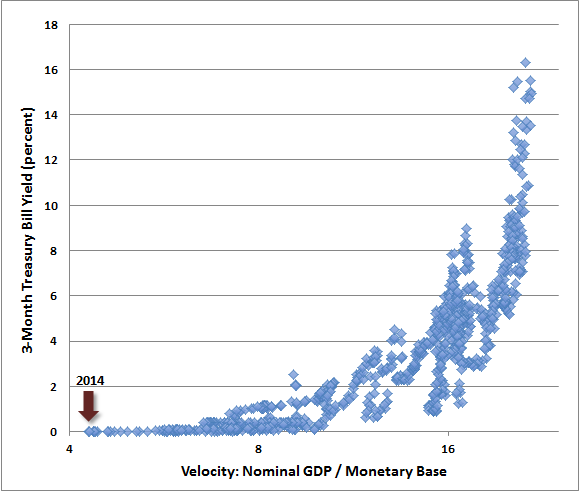

November 3, 2014 Losing Velocity: QE and the Massive Speculative Carry Trade On Friday, the Bank of Japan promised a fresh round of quantitative easing, prompting a collapse in the yen, a surge in the U.S. dollar, and marginal new highs in several stock market indices. Presently, internal dispersion and credit spreads remain wide – keeping our measures of market internals negative, at least for now. As I noted last week, “we remain quite agnostic about near-term market behavior. The next several sessions could contain a significant further short-squeeze or a vertical collapse, and we have very little predictive basis for that distinction.” That view hasn’t changed. Last week’s advance brought the recent spike beyond the short squeezes that normally clear the first “air pocket” breakdown in market internals following overvalued, overbought, overbullish conditions (see Fast, Furious, and Prone-to-Failure). Those squeezes normally don’t take the major indices to fresh highs, though two central bank events in a single week undoubtedly played a role, and neither the Russell 2000 nor the NYSE Composite confirmed. The closest historical correlate to the recent short-squeeze is the spike that quickly brought the market from its May 1901 “air pocket” low to a fresh high in June of that year. That peak reached a Shiller P/E of 24 (S&P 500 divided by the 10-year averaged of inflation-adjusted earnings). The stock market still went on to lose half of its value from that June high (a fact that Steven Hochberg at EWI has also noted in a slightly different context). From a full-cycle perspective, we continue to view present conditions as among the most hostile in history. But we have no view at all about the near-term outlook except that the growing instability should be taken seriously, volatility may be quite high, and direction may shift on a dime. At present, the entire global financial system has been turned into a massive speculative carry trade. A carry trade involves buying some risky asset – regardless of price or valuation – so long as the current yield on that asset exceeds the short-term risk-free interest rate. Valuations don’t matter to carry-trade speculators, because the central feature of those trades is the expectation that the securities can be sold to some greater fool when the “spread” (the difference between the yield on the speculative asset and the risk-free interest rate) narrows. The strategy relies on the willingness of market participants to equate current yield (interest rate or dividend yield) with total return, ignoring the impact of price changes, or simply assuming that price changes in risky assets must be positive because low risk-free interest rates offer “no other choice” but to take risk. The narrative of overvalued carry trades ending in collapse is one that winds through all of financial history in countries around the globe. Yet the pattern repeats because the allure of “reaching for yield” is so strong. Again, to reach for yield, regardless of price or value, is a form of myopia that not only equates yield with total return, but eventually demands the sudden and magical appearance of a crowd of greater fools in order to exit successfully. The mortgage bubble was fundamentally one enormous carry trade focused on mortgage backed securities. Currency crises around the world generally have a similar origin. At present, the high-yield debt markets and equity markets around the world are no different. As we’ve detailed previously, zero-interest rate policy has very little historical evidence or compelling theory to recommend it. Rather, the policy is based on 1) the misguided belief that people consume on the basis of fluctuations in volatile asset prices and other transitory forms of income (a concept that Milton Friedman won a Nobel Prize largely for debunking), and 2) a view of the global economy as nothing more than one big interest-sensitive demand curve. See Broken Links: Fed Policy and the Growing Gap Between Wall Street and Main Street to review the reasons why suppressed interest rates have had such weak impact on global growth, despite fueling the third equity market bubble in 15 years. Are Suppressed Interest Rates “Stimulative”? The Federal Reserve ended its program of QE on Wednesday. Even here, however, the members of the FOMC appear to believe that below-equilibrium short-term interest rates are somehow supportive to the economy. It doesn’t seem to even cross their minds to examine the historical evidence that no such relationship exists in the data. For example, go ahead and estimate the quarterly change in U.S. real GDP using lagged (prior) quarterly changes in real GDP, lagged changes in short-term interest rates, the current level of short-term interest rates, the year-over-year CPI inflation rate, and the unemployment rate. Now, completely drop the current level of short-term interest rates and those lagged interest rate changes from your explanatory variables. You’ll get a nearly identical fit. In other words, information about short-term interest rates has no incremental ability to predict subsequent economic growth. Whatever relationship interest rates have to subsequent economic growth is already contained in prior changes in GDP, unemployment and inflation. Interest rate changes are largely the results of prior measures of economic activity, not the causes of future economic activity. Now, it’s certainly true that the Fed has lowered actual interest rates far below what GDP, employment and inflation would indicate. In fact, given present economic conditions, one would expect from historical relationships that short-term Treasury bills would otherwise be about 2.4% here. So zero interest rates are obviously the Federal Reserve’s doing. The question, then, is do deviations of actual short-term interest rates from expected interest rates provide information about subsequent economic growth? That is, can we find evidence that driving interest rates down more than justified by economic conditions is stimulative to economic activity? The answer: not at all. In fact, those deviations have literally zero explanatory power about subsequent economic activity. The fact is that financial repression – suppressing nominal interest rates and attempting to drive real interest rates to negative levels – does nothing to help the real economy. This is certainly not a new revelation. In part, this fact can be understood by thinking about how interest rates are related to the productivity and quantity of real investment in the economy. More than a decade ago, economist Alan Gelb (Financial Policies, Growth and Efficiency, 1989) examined historical economic performance for thirty-four countries, and found that the productivity of real investment (as measured by incremental output per unit of capital) is highly and positively correlated with real interest rates. Notably, however, the level real interest rates had very little to do with the observed quantity of real investment as a share of GDP (if anything, in U.S. data, we actually observe a tendency for fluctuations in gross domestic investment/GDP to precede changes in short-term interest rates with the same direction). Gelb demonstrated that real interest rates have an ambiguous relationship with the amount of investment that occurs in the economy, but higher real interest rates are clearly associated with higher productivity of investment and faster economic growth. One should be careful not to interpret this relationship as a cause-effect link that can be manipulated. Rather, it cautions against attempted manipulations. The best way to think about real interest rates is to think about the economic context that produces them. High real interest rates generally reflect strong demand for borrowing, driven by investment opportunities that are seen as productive enough to justify borrowing at those rates. They also encourage savings that can be directed to those productive investments. As a result, higher real rates are generally associated with more efficient investment and faster economic growth. In contrast, depressed real interest rates are symptomatic of a dearth of productive investment opportunities. When central banks respond by attempting to drive those real interest rates even lower to “stimulate” interest-sensitive spending such as housing or debt-financed real investment, they really only lower the bar to invite unproductive investment and speculative carry trades. We wouldn’t suggest that the Fed target above-equilibrium interest rates, but we are also entirely convinced that below-equilibrium interest rates are harmful to long-term economic and financial stability. Despite the ability of these policies to create short-term bursts of demand – enough to hold the global economy at growth rates that remain just at the border that has historically delineated expansions from recessions – the ultimate and rather predictable result of these policies will be another round of financial chaos. Losing Velocity From a monetary perspective, it’s easy to understand why replacing Treasury securities with zero-interest money (currency and bank reserves) does little to “stimulate” the economy. We may wish to believe that putting more zero-interest money into the economy would lead people to go out and spend those idle balances, but that imagines some fixed ratio between economic activity and the amount of money outstanding. That’s the error. The velocity of money (nominal GDP / monetary base) isn’t fixed at all. What happens in practice is that as the Fed creates more zero-interest money, holders try to get rid of it by buying financial assets that provide a higher potential return – driving prices up and expected future returns down until they are indifferent between an overpriced financial asset and zero-interest money. The closest alternative to currency is Treasury bills. So as the Fed creates more zero interest money, investors bid up Treasury bills, which lowers their interest rate. That’s how Fed actions move short-term yields. As the central bank creates more money and interest rates move lower, people don’t suddenly go out and consume goods and services, they simply reach for yield in more and more speculative assets such as mortgage debt, and junk debt, and equities. Consumers don’t consume just because their assets have taken a different form. Businesses don’t invest just because their assets have taken a different form. The only activities that are stimulated by zero interest rates are those where interest rates are the primary cost of doing business: financial transactions. To see what’s actually going on here, the chart below shows the relationship between monetary velocity (nominal GDP per dollar of monetary base) and Treasury bill yields, in Federal Reserve data since 1929. The horizontal axis is log scale to better demonstrate what has happened in recent years. Normally, as the Fed creates more monetary base, short-term interest rates fall in a fairly smooth way. But having hit zero interest rates some $1.5 trillion ago, further increases in the monetary base have simply pushed us further and further to the left, and velocity has simply declined in direct proportion to base money. At this point, further monetary easing does nothing for short-term interest rates, and nothing for nominal GDP. It just pushes velocity lower and lower.

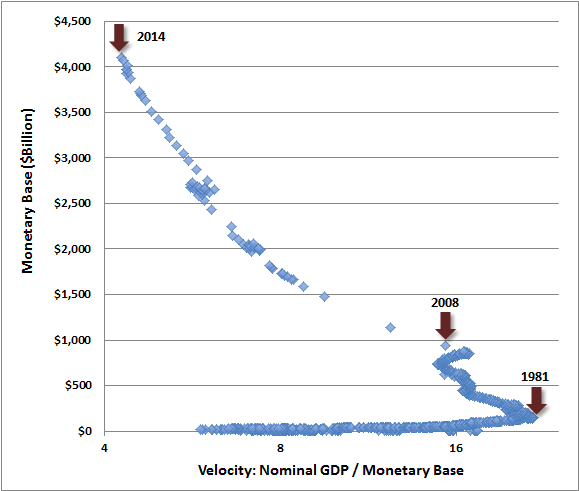

Notice something important. You can’t increase inflation by creating more money if velocity falls proportionately. Money creation, velocity, and short-term interest rates are all tied together in a joint relationship where knowing two of those variables basically informs you of the third. In order to create inflation, something exogenous has to occur that encourages revulsion toward risk-free money and raises velocity – even holding the money stock constant. For example, suppose that market interest rates of 1% were available, but the interest rate earned on base money (currency and bank reserves) was still held to zero. In that environment, velocity would nearly double, and while we doubt that real GDP would change by much, one would expect the consumer price level to also nearly double. There might be a way to engineer this outcome, but we’re not evil enough to spend time thinking about such schemes. To understand velocity another way, the following chart – again in Federal Reserve data since 1929 – shows monetary velocity (log scale) versus the monetary base itself. Notice that monetary velocity peaked in 1981 when short-term interest rates were pushing above 15%. In that environment, zero-interest base money was costly to hold, so money turned over quite rapidly. In 2008, the Federal Reserve embarked on its policy of quantitative easing. Not surprisingly, velocity has collapsed to historic lows. The result is dramatically more monetary base, dramatically less turnover, and no material change in economic activity.

What central banks around the world seem to overlook is that by changing the mix of government liabilities that the public is forced to hold, away from bonds and toward currency and bank reserves, the only material outcome of QE is the distortion of financial markets, turning the global economy into one massive speculative carry trade. The monetary base, interest rates, and velocity are jointly determined, and absent some exogenous shock to velocity or interest rates, creating more base money simply results in that base money being turned over at a slower rate. Economic growth and inflation do not arise from changing the mix of these government liabilities. Growth arises primarily from a) the channeling of scarce saving to productive investment that b) generates useful goods and services that c) can be purchased because the income paid to factors of production can – in a circular flow – be used to pay for that output. QE does nothing to aid this dynamic unless scarce bank liquidity is a binding constraint on productive investment or spending, which it presently is not. QE does not spur new demand in an environment where productive investment opportunities are satiated by the existing availability of loanable funds. It just provides cheap finance for speculative carry trades in the financial markets. Meanwhile, inflation and hyperinflation typically do not arise from simply from changing the mix of government liabilities toward more currency. Inflation emerges primarily from supply constraints or an exogenous shock that reduces supply, coupled with fiscal policy where large government deficits are being used to finance consumption and transfer payments. In that environment, the marginal value of goods surges relative to the marginal value of a currency unit, and the mix of government liabilities held by the public doesn’t particularly matter. Financing the deficits with debt instead of money still results in exogenous upward pressure on interest rates and monetary velocity. Hyperinflation results when there is a complete loss in the confidence of currency to hold its value, leading to frantic attempts to spend it before that value is wiped out. I expect we’ll observe significant inflationary pressures late in this decade, but present conditions aren’t conducive to rapid inflation without some shock to global supply. With regard to the recent move by the Bank of Japan, seeking to offset deflation by expanding the creation of base money, the move has the earmarks of a panic, which is counterproductive. The likely response of investors to panic is to seek safe, zero-interest money rather than being revolted by it. The result will be a plunge in monetary velocity and a tendency to strengthen rather than reduce deflationary pressures in Japan. In our view, the yen has already experienced a dramatic Dornbusch-type overshoot, and on the basis of joint purchasing power and interest parity relationships (see Valuing Foreign Currencies), we estimate that rather than the widely-discussed target of 120 yen/dollar, value is wholly in the other direction, and closer to 85 yen/dollar (the current exchange rate is just over 112). The Japanese people have demonstrated decades of tolerance for near-zero interest rates and the accumulation of domestic securities without any material inclination to spend them based on the form in which those securities are held. Rather than provoking strength in the Japanese economy, the move by the BOJ threatens to destroy confidence in the ability of monetary authorities to offset economic weakness – in some sense revealing a truth that should be largely self-evident already. A final note We’ve always been committed to several principles: historically-informed analysis, value-conscious investment, relentless discipline, and open communication. I built my reputation not only on bearish outlooks such as anticipating the 2000-2002 and 2007-2009 collapses, but by bullish ones such as a leveraged stance early in the 1990’s bull market and a shift to a constructive stance in early-2003 as a new bull market was emerging. I’ve clearly damaged that reputation - at least temporarily - in the increasingly speculative half-cycle since 2009. In the interim of my 2009 decision to stress-test our methods against Depression-era data (following a financial crisis that we clearly anticipated) we missed what both our pre-2009 and our present methods would have identified as the most constructive opportunity in the present half-cycle. Then, in the face of relentless quantitative easing, even those resulting stress-tested methods ultimately required trend-sensitive overlays similar to those we implemented during the late-1990’s bubble. See Setting the Record Straight for more details on those challenges and how we’ve addressed them. Having addressed and adapted to the challenges we’ve faced in the half-cycle since 2009, I am more confident in our full-cycle discipline than at any point in nearly three decades of investment work, but overvalued bull market peaks may still be drawn-out and frustrating. They can seem endless (see The Journeys of Sisyphus) and then suddenly unravel far more rapidly than it seems they should (see Chumps, Champs, and Bamboo) at which point the “lagging” features of a defensive stance are often reversed with striking speed. As the late MIT economist Rudiger Dornbusch once observed, “The crisis takes a much longer time coming than you think, and then it happens much faster than you would have thought.” Recall that the 2000-2002 decline wiped out the entire total return of the S&P 500 – in excess of Treasury bill returns – all the way back to May 1996. The 2007-2009 decline wiped out the entire total return of the S&P 500 – in excess of Treasury bill returns – all the way back to June 1995. As I’ve noted before, the problem with what we call the Exit Rule for Bubbles – “you only get out if you panic before everyone else does” – is that you also have to decide whether to look like an idiot before the crash or an idiot after it. I have no particular desire to convince anyone that our view is the right one. Go your own way. Those who value historically-informed analysis, value-conscious investment, relentless discipline, and open communication know where to find us. With the recent overvalued, overbought, overbullish extreme now followed by a deterioration in market internals (that as yet has not been reversed), history informs us to be very cautious here. That evidence will change, and our outlook will change as the evidence does. As for the near-term, I’ll reiterate again that we have no pointed views, but as in 2000 and 2007, we believe history clearly informs us about how this cycle is likely to end, and that we should not be surprised to see years of market gains wiped out during that completion. In the meantime, we’re mindful that the financial markets move not based on what is true, but by what is perceived. On that point we remain attuned to the quality and uniformity of market action across a wide range of market internals. Our view remains that this is a recklessly speculative market, but we also recognize the potential to fight somewhat less strongly against that speculation if internal deterioration becomes less evident. Aside from the expectation of broad volatility and abrupt reversals, I have no views about short-term market direction here. We’ll take our evidence as it arrives.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |