|

|

||||||

|

|

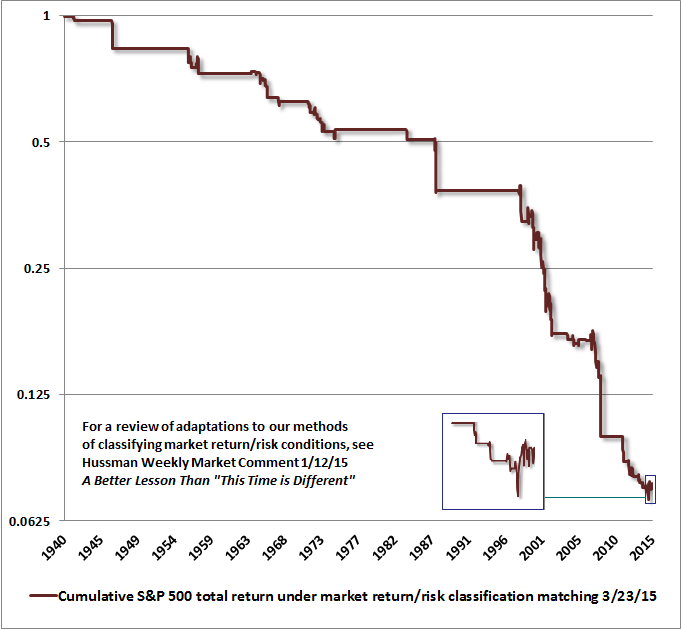

March 23, 2015 Monetary Policy and the Economy: The Case for Rules Versus Discretion Last week, the Federal Reserve Open Market Committee (FOMC) began its statement on monetary policy indicating that recent data “suggests that economic growth has moderated somewhat.” While the Fed removed the phrase that “it can be patient in beginning to normalize the stance of monetary policy”, the Fed’s weaker view of the economy prompted an immediate retreat in Treasury yields, an abrupt drop in the foreign exchange value of the U.S. dollar, a surge in stock prices, and an upward spike in the dollar price of gold and oil. The basic thesis of all of these moves is that the Fed may wait longer before increasing the rate of interest that it pays to banks on idle cash reserves (viz., “raising interest rates”). We agree – partly. As I noted a week ago, “From my perspective, it remains unclear whether the Fed will resist the temptation to defer hiking interest rates, given what we observe as a deteriorating economic landscape.” The problem for investors is that along with the initial moves in Treasury yields, the dollar, stocks, gold, and oil that followed the FOMC statement, we also saw credit spreads widen rather than narrow last week, while our measures of market internals continue to show divergences that indicate a shift investor preferences toward increasing risk aversion. Since mid-2014, when we completed the awkward transition that followed my 2009 insistence on stress-testing our methods against Depression-era data (see A Better Lesson than “This Time is Different”, Setting the Record Straight and Hard Won Lessons and The Bird in the Hand for a full review), I’ve emphasized that the response of the financial markets to overvalued conditions, and to Fed policy, is conditional on whether investor preferences are risk-averse or risk-seeking. While we do expect that the FOMC will be much slower to raise rates than some members would prefer, we strongly believe that the singular focus on interest rates is misguided in the first place. The following comments from early February (see Expect a Decade of 1.7% Portfolio Returns from a Conventional Asset Mix) draw the crucial distinction, and capture the central lesson that should be drawn from our own experience. “First and foremost, the response of the equity markets to Federal Reserve easing (and much other news) is conditional on the risk-tolerance of investors at the time, which we infer from observable market action such as internals and credit spreads, among other factors. Quantitative easing ‘works’ by creating default-free liquidity in an environment where that liquidity is viewed by investors as an inferior asset. That is, if investors are risk-seeking, as inferred from the uniformity of market action across securities, sectors and asset classes of all risk profiles, then yes – Fed easing will tend to support further advances in stock prices regardless of the level of valuation. On the other hand, once investors have shifted toward risk-aversion, overvalued markets become vulnerable to abrupt free-falls and crashes, and monetary easing is not materially supportive for stocks because default-free liquidity is desirable. “Again, as I noted in The Line Between Rational Speculation and Market Collapse, investors should remember that the Fed began cutting interest rates on February 11, 1930 – nearly two and a half years before the market bottomed. The Fed cut rates on January 3, 2001 just as a two-year bear market collapse was starting, and kept cutting all the way down. The Fed cut the federal funds rate on September 18, 2007 – several weeks before the top of the market, and kept cutting all the way down. “What will matter significantly for investors is the condition of market internals, credit spreads, and other risk-sensitive measures in the event that U.S. economic activity begins to further reflect the downturn that is already evident abroad. It is that evidence of investor risk-preferences that will determine the proper response to any change in Fed policy.” My impression is that while recent slowing is likely to deter the Fed from raising the interest rate on reserves, the enthusiasm of investors about this possibility is misplaced. In a context of widening credit spreads, extreme equity overvaluation, and divergent market internals, weaker economic evidence adds to downside concerns far more than the prospect of a continued zero interest rate compensates. The chart below shows the cumulative total return of the S&P 500 restricted to the same market return/risk classification that we identify at present. The small pullout shows recent quarters, with a sequence of quick but modest losses, a larger loss last October, and more recent churning action. While we’ve observed a recovery from the October low, such short-term behavior is not particularly uncommon, and similar churning has been indicative of top formation in previous instances (e.g. 1957, 1972, 1999-2000, and 2007). These choppy periods have generally been overwhelmed by the steep average market losses associated with these conditions.

Informed discipline I’ll emphasize as usual that our focus is decidedly on the complete market cycle, and we have no intention to dissuade investors from other personally suitable, well-understood and historically-informed disciplines. Our main advice for passive investors is to maintain your discipline, but also – please – make sure that your portfolio allocation is well-aligned with your investment horizon, that you recognize in advance and fully anticipate the likelihood of a few market losses during the coming decade in the 30-50% range (as Jack Bogle also encourages), and that you recognize that rich valuations after extended advances and record highs imply much more conservative assumptions about future returns than depressed valuations do. Investors that only become “enlightened” to espouse a buy-and-hold strategy after long market advances, who anticipate strong long-term gains from elevated valuations, and who limit their concept of “loss” to a shallow 20% decline, are often the same investors that abandon that strategy by the end of the cycle. It's useful to remember that passive investment strategies can seem nearly infallible after a multi-year advance half-way through a market cycle, and extreme valuations can seem irrelevant precisely because they have become extreme without consequence (recall 2000, 2007 and a litany of other cyclical peaks). Still, the completion the market cycle often results in a dramatic turn of the tables in the standing of buy-and-hold approaches relative to risk-managed alternatives. Meanwhile, understand that the transition from our pre-2009 methods to our present methods created a muddy connection between two spans of data: 1) The span until early 2009, when I doubt there was any question about the effectiveness of our discipline and; 2) the period since mid-2014, when we’ve been defensive for reasons much the same as we were prior to the 2000-2002 and 2007-2009 collapses. The muddy part is the intervening transition from our pre-2009 methods to our present methods of classifying market return/risk profiles (again, see A Better Lesson than “This Time is Different”). The fact is that both our pre-2009 methods and our present methods of classifying market return/risk profiles would have encouraged a constructive and often aggressive outlook during much of that transition period. I’ve regularly detailed this narrative, possibly to excess. But instead of criticizing me accurately for my 2009 stress-testing inclinations and the challenges that ensued, or understanding how we addressed those challenges, we see an (increasingly unoriginal) eagerness to present our experience as a case-study against evidence-based market analysis, unconventional views, and anything short of gratuitous acceptance of market risk – half-way into a market cycle, with prices at record highs, and with reliable valuation measures at obscene levels. This offers the wrong lesson, and it’s one that I expect will get investors into trouble because it encourages them to ignore legitimate risks here. One obtains the satisfaction of dispensing uninformed (or intellectually dishonest) criticism, but discards the benefit of a narrative that has valuable lessons for this and future cycles. As always, we encourage passive investors to adhere to their discipline, as we adhere to ours. Our hope, however, is that regardless of discipline, investors align their portfolios with their investment horizon and their ability to tolerate loss, approaching the market with a realistic understanding of where market conditions stand in a historical context, and – with reliable valuation measures higher than at any point in history except 2000 – an appreciation of the substantial risks that may emerge over the completion of the current market cycle. Monetary policy and the economy – the case for rules versus discretion The real-time estimate of first quarter real GDP growth published by the Atlanta Fed dropped again last week to just 0.3%. Broader measures are consistent with this deterioration, retreating considerably and in a familiar sequence that typically begins with market internals, credit spreads and industrial commodities; followed by the new orders and production components of regional purchasing managers indices and Fed surveys; followed by real sales; followed by real production; followed by real income; followed by new claims for unemployment; and confirmed much later by payroll employment (See Market Action Suggests an Abrupt Slowing in Global Economic Activity).

It’s still not obvious that the recent economic deterioration will continue, but a further retreat in the purchasing manager’s index below 50 and a drop in the S&P 500 below its level of 6 months ago (about the 2000 level), coupled with already widening credit spreads and the absence of a steep yield curve, would complete a recession warning composite with much stronger implications. Though we warned of the 2000-2001 and 2007-2009 recessions as they began in real-time, and quarters before they were broadly recognized, we also had persistent economic concerns between 2010 and 2012 that were at least deferred by monetary bazookas aimed at bringing future consumption forward as much as possible. We were in good company with Lakshman Achuthan at ECRI (the only other organization we know to correctly give early warning in both of those prior recessions). Neither I nor Lakshman (to my knowledge) see enough evidence to warn of a recession at present. My sense is that should we both warn of a recession in the future, dismissing those concerns as “crying wolf” will probably result in being eaten first. For now, suffice it to say that the economic data is going the wrong way, and the sequence of deterioration is familiar. Will a continuation of zero interest rates encourage a stronger economy? We can’t deny that grand announcements of projectile money issuance have, in recent years, been able to bring forward enough demand to spur a quarter or two of stronger economic growth. Yet even those episodes have been short lived. It’s often argued that “we can’t know what the economy would have done without extraordinary monetary policy,” but that’s not really true. One must remember that much of the economic recovery that occurs after a recession is ordinary mean reversion, and we can get quite a good sense of the baseline “counterfactual” using statistical tools such as vector autoregression. These allow us to estimate the economic activity that would have been expected solely on the basis of non-monetary variables. As we showed last week (see Extremes in Every Pendulum), economic growth in recent years has actually been slower than one would have predicted based on lagged values of non-monetary variables such as GDP growth and employment. We don’t dispute that the Fed had an essential role in providing liquidity to cash-strapped banks during the crisis, but the change in accounting rules by the FASB in March 2009 (abandoning the need for banks to mark their assets to market value) is what ended the crisis, not extraordinary monetary policy. Beyond the quite short-lived effect of monetary bazookas; beyond the massive financial distortion and malinvestment provoked by activist monetary policy; beyond the long-run damage to living standards that result from the failure to direct savings toward the accumulation of productive capital; beyond the repeated collapses that attend the unwinding of financial bubbles provoked by Fed-induced yield-seeking speculation; does the economy favorably respond to “extraordinary” monetary intervention? When we examine nearly 70 years of data, what we find is this: Deviations in monetary policy from what one would have predicted (using past non-monetary variables alone) have practically zero ability to explain subsequent GDP growth (versus the levels that would have been predicted by past non-monetary variables alone). In other words, once we allow for the component of monetary policy captured by a fixed linear rule (the Taylor Rule comes close – and currently indicates an appropriate Fed funds rate of about 3% here), one can find no evidence in the historical record that additional activist monetary policy is useful. It’s for that reason*, along with a great deal of macroeconomic literature on the benefits of rules versus discretion, that we strongly endorse policies that would require the Federal Reserve to articulate a Taylor-type rule, departing from it primarily during liquidity crises (and even then, ideally providing liquidity only to solvent institutions, and at higher than market interest rates in order to encourage prompt post-crisis repayment – Bagehot’s Rule). It’s notable that earlier this month, Professor Taylor himself objected to Yellen’s mischaracterization before Congress of his views. Taylor noted: “Hearings specifically about this reform and other hearings such as those with Chair Yellen last week have been useful for getting input and finding the best way forward. But concerns and misunderstandings persist. For example, in answering questions from Chairman Shelby last week, Fed Chair Yellen stated that ‘I am not a proponent of chaining the Federal Open Market Committee in its decision making to any rule whatsoever.’ And the next day she repeated that view to Chairman Hensarling, saying ‘I don’t believe that the Fed should chain itself to any mechanical rule.’ And in both hearings she quoted me saying that the Fed should not follow a mechanical rule. But the House monetary strategy bill, or similar proposals, would not chain the Fed to any rule. First, the Fed would choose and describe its own strategy, and it need not be a mechanical rule. Second, the Fed could change the strategy if the world changed, or it could deviate from the strategy in a crisis; so it would not be ‘chained.’ The Fed would have to report the reasons for the changes or departures, but, as in the example of departing from the policy rule during the stock market break in 1987, which Chair Yellen referred to, it would not be difficult to explain such adjustments.” NEW from Bill Hester: Is the Rush into European Stock Markets Warranted? *Geek's Technical Note: Let Y be a vector of non-monetary target variables such as output and employment. Estimate from the data a “typical” monetary policy response function of the form M = f(prior Y) + Em, where the “error” term Em represents extraordinary monetary policy beyond what would be predicted by that policy response function. Now compute the errors Ey as the deviations between actual Y and projections based on an autoregression of Y on prior values of itself, and compare those with errors Eym projecting Y using prior values of both Y and M. If extraordinary monetary policy is effective, the projection errors Eym should have a smaller variance than those of Ey alone, because the “extraordinary policy” term Em will be correlated with Ey (put simply, Em will help to explain Ey). In U.S. data since 1947, we estimate this correlation to be effectively zero, with "extraordinary" monetary policy explaining virtually none of the variance in GDP growth left unexplained by non-monetary variables alone. On purely statistical tests (e.g. Wald, L-M) one can reject the hypothesis of no relationship, but the practical size of that relationship appears economically meaningless. The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |