|

|

||||||

|

|

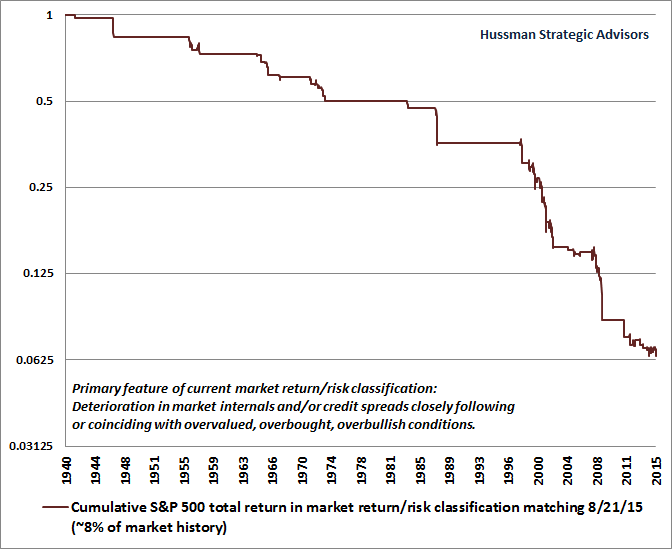

August 24, 2015 Risk Turns Risky: Unpleasant Skew, Scale Dilation, and Broken Lines Over the years, I’ve observed that overvalued, overbought, overbullish market conditions have historically been accompanied by what I call “unpleasant skew” – a succession of small but persistent marginal new highs, followed by a vertical collapse in which weeks or months of gains are wiped out in a handful of sessions. Provided that investors are in a risk-seeking mood (which we infer from the behavior of market internals), sufficiently aggressive monetary easing can delay this tendency, by starving investors of every source of safe return, and actively encouraging further yield-seeking speculation even when valuations are obscene. Once investors become risk-averse, as deteriorating market internals have suggested in recent months, vertical declines much more extreme than last week's loss are quite ordinary. The way to understand the bubbles and collapses of the past 15 years, and those throughout history, is to learn the right lesson. That lesson is not that overvaluation can be ignored indefinitely – we know different from the collapses that have regularly followed extreme valuations. The lesson is not that easy monetary policy reliably supports stock prices – persistent and aggressive easing did nothing to keep stocks from losing more than half their value in 2000-2002 and 2007-2009. Rather, the key lesson to draw from recent market cycles, and those across a century of history, is this: Valuations are the main driver of long-term returns, but the main driver of market returns over shorter horizons is the attitude of investors toward risk, and the most reliable way to measure this is through the uniformity or divergence of market internals. When market internals are uniformly favorable, overvaluation has little effect, and monetary easing can encourage further risk-seeking speculation. Conversely, when deterioration in market internals signals a shift toward risk-aversion among investors, monetary easing has little effect, and overvaluation can suddenly matter with a vengeance. Last week’s decline, while seemingly significant, was actually a rather run-of-the-mill example of “unpleasant skew” that has regularly followed similar market conditions throughout history. I’ve updated the chart I presented last week, which shows how contained last week’s market loss actually was in the context of present conditions. As I wrote a week ago, “It's the 8% of history that matches current conditions where most market crashes have occurred. The chart below shows the cumulative total return of the S&P 500 restricted to this subset of history. The chart is on log scale, so each horizontal line represents a 50% loss. The vertical lines straight down are actually 2-3 week air pockets, free-falls and crashes where stocks experienced losses of as much as 25%, often with continued (but less predictable) follow-on losses after exiting this particular return/risk profile. The past several months appear as a little congestion area in the lower right of the graph. Investors should emphatically not rule out progressive losses – even a straight line down – under present conditions.”

The 8% subset of history matching present conditions captures a cumulative loss in the S&P 500 equivalent to turning a dollar into less than 7 cents. Conversely, the remaining 92% of market history captures a cumulative gain in the S&P 500 of more than (1/.07=) 14 times the overall return in the index across history. You’ll note that I’ve added an additional segment below 0.0625 as a reminder that each horizontal bar lower represents a further 50% market loss. We’re probably going to need that extra room. The good news is that we’re not going to stay in this 8% subset of historical conditions indefinitely, and the current market return/risk profile is the only one where severe market losses should be strongly expected. Another 32% of return/risk conditions we identify are associated with relatively flat expected market returns (generally near or below Treasury bill yields, on average, but including both positive and negative fluctuations). In those conditions, significant market risk isn’t worth taking because the weak average returns still come with the potential for sizeable interim losses. That sort of condition encourages a neutral investment stance, or one that is “constructive with a safety net.” The remaining 60% of market conditions we identify are associated with strongly positive expected return/risk profiles, where an unhedged or aggressive outlook is reasonable. Our shift to that outlook will likely occur at the point when a material retreat in valuations is joined by an improvement in market internals. No specific forecasts or projections are required here. Our approach is to align our investment outlook with the prevailing return/risk classification we identify at each point in time. We’ll adjust our outlook as the observable evidence shifts. Causes versus Triggers We should distinguish between causes and triggers here. If you roll a wheelbarrow of dynamite into a crowd of fire jugglers, there’s not much chance things will end well. The cause of the inevitable wreckage is the dynamite, but the trigger is the guy who drops his torch. Likewise, once extreme valuations are established as a result of yield-seeking speculation that is enabled (1997-2000), encouraged (2004-2007), or actively promoted (2010-2014) by the Federal Reserve, an eventual collapse is inevitable. By starving investors of safe return, activist Fed policy has promoted repeated valuation bubbles, and inevitable collapses, in risky assets. On the basis of valuation measures having the strongest correlation with actual subsequent market returns, we fully expect the S&P 500 to decline by 40-55% over the completion of the current market cycle. The only uncertainty has been the triggers. We know that obscene valuation is the ultimate cause of the rather inevitable market loss we can expect over the completion of the present market cycle. We also know that conditions are most permissive for market collapses when overextended market conditions are joined by deterioration in market internals (signaling increased risk-aversion among investors). But what triggered the timing of last week’s abrupt decline? My impression is that trigger of last week’s market loss was not China’s yuan devaluation or even concern about the potential for a Federal Reserve rate hike. Rather, the trigger was most likely the sudden deterioration of leading economic measures, energy prices, and industrial commodities, both in the U.S. and globally. This weakness first became evident in February (see Market Action Suggests Abrupt Slowing in Global Economic Activity). After a brief rebound, the data has deteriorated abruptly once again. While extraordinary monetary interventions across the globe have certainly distorted the financial markets, they have done little to support the real economy, and developing economic weakness in the U.S. and abroad is beginning to clarify that ineffectiveness. Based on reports available through Friday, the chart below of regional Fed and purchasing manager surveys shows the fresh deterioration we observe here.

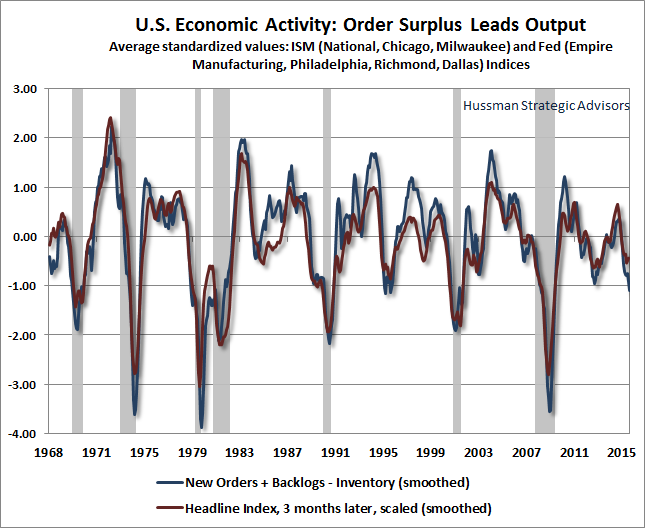

Remember the sequence I described in February, as credit spreads widened and industrial commodity prices fell: “Generally speaking, joint market action like this provides the earliest signal of potential economic strains, followed by the new orders and production components of regional purchasing managers indices and Fed surveys, followed by real sales, followed by real production, followed by real income, followed by new claims for unemployment, and confirmed much later by payroll employment.” The charts below illustrate this sequence. First, order surpluses lead output. The chart below measures order surplus as new orders plus backlogs, minus inventories, based on standardized values of regional Federal Reserve and purchasing managers surveys, compared with the “headline” indices of these surveys three months later. The recent dropoff in order surpluses is an important economic concern here.

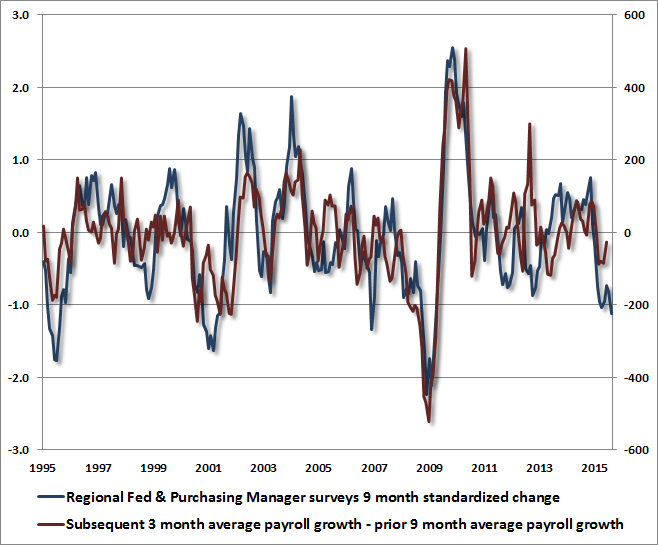

Similarly, it’s clear that the overall change in these regional surveys over the prior 9 month period tends to lead changes in employment. The chart below compares the 9 month standardized change in these surveys with the average change in payroll employment over the following 3 month period (measured as an increase or decrease from the pace of the prior 9 months). The recent deterioration in regional economic surveys is consistent with a shortfall of about 200,000 jobs from the average rate of job creation over the past 9 months. Since non-farm payrolls have been increasing by about 250,000 new jobs per month, it appears reasonable to expect substantially lower but still somewhat positive job growth in the coming quarter. Depending on the outcome, weaker employment growth may reduce the willingness of the Federal Reserve to raise interest rates, but the primary factor to monitor with respect to the stock market will not be the words or behavior of the Fed per se, but rather, whether market internals change in a way that indicates a shift toward greater risk-seeking by investors. Based on the response of investors during economic downturns after 2000 and 2007, we shouldn’t count on that.

Scale Dilation Among the features that make our world recognizable is that many things have the same basic shape, and the same basic movement patterns, regardless of their resolution. Trees, snowflakes, fern leaves and other objects often feature “self-similarity”; the smaller component parts look much like the whole. Likewise, a minute-by-minute chart of the stock market looks much like an hour-by-hour chart or a month-by-month chart. It’s just that the movements are on a different scale. Self-similarity is where the smaller parts of something resemble the whole.

A similar concept in geometry is the idea of “scale dilation.” But in this case, the relationship isn’t between the whole and its parts. Rather, scale dilation simply increases the size of the existing object by stretching it out. Here’s a nice example of scale dilation:

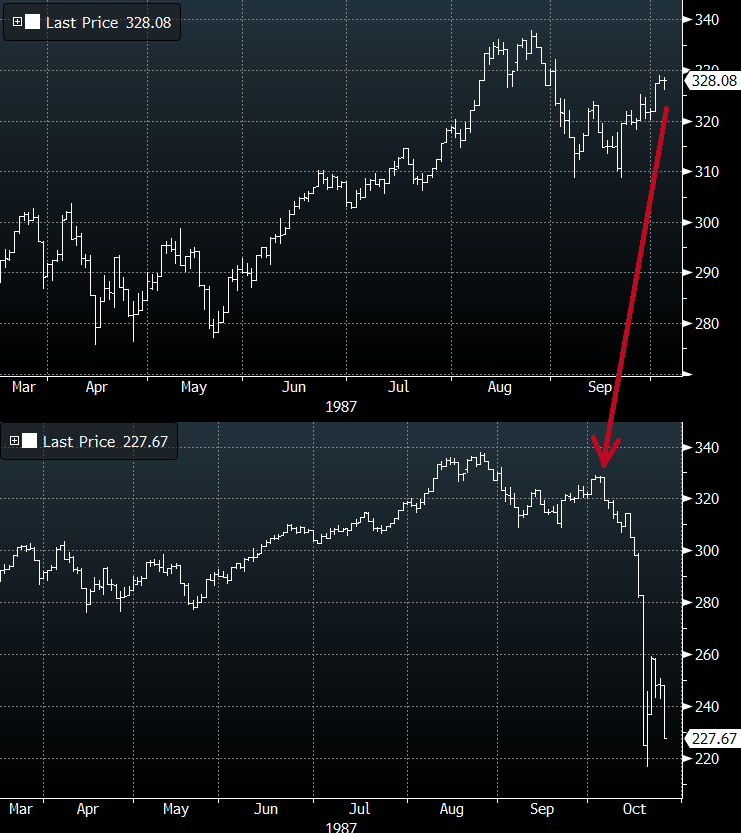

In my view, one of the reasons that market plunges feel so chaotic and disruptive is that investors don’t anticipate the scale dilation that typically occurs as risk premiums spike higher. In the stock market, this happens with regularity in every cycle. Put simply, the day-to-day market declines that investors have come to believe are significant today are child’s play relative to the range of movement that they should expect as the scale dilates over the completion of the current market cycle. In 30 years as a professional investor, I’ve watched many of those dilations in real time, including those that followed the 1987, 2000 and 2007 peaks. What happens is this: as the scale dilates, investors seem to mentally cling to their experience of smaller fluctuations, so the large initial declines of a bear market are frightening, but also seem extremely enticing, because the rebounds after those initial declines also tend to be large and encouraging. That’s often why investors are lured into “buying the dip” early in a bear market. Those initial declines can end up looking quite small once the full scope of the market loss unfolds. The following charts will give you a good idea of what I’m calling “scale dilation.” The first is from the 1987 market peak. What happened in 1987 was an abrupt spike in risk premiums. It was preceded by an extended period of overvalued, overbought, overbullish conditions that was joined by deterioration in market internals (conveying a shift toward greater risk-aversion among investors). The initial losses from the August peak seemed incredibly large, but the subsequent recovery into the first week of October gave the market the look of “resilience.” The red arrow shows that same point in early October from a broader perspective, after the scale dilation. Note in the lower chart how tiny those pre-October daily bars look like relative to the daily bars during and after the crash. Since the lower chart covers more time, it’s obvious that the bars will be closer together in that panel. The thing to compare is the range of daily fluctuations and the amount of ground covered before and after the scale dilation, as risk premiums and volatility spiked higher.

The next chart shows the same scale dilation after the 2000 market peak, on the way to 777 on the S&P 500. At the time, a 12% retreat in the S&P 500 seemed like a steep correction. The actual market loss would take the S&P 500 down by half.

In 2008, the market experienced a similar scale dilation as risk premiums spiked higher. After an initial selloff from the October 2007 highs, the market recovered within 10% of its peak by May 2008. In hindsight, the seemingly wide pre-May market range was nothing compared with the extreme market fluctuations – even day-to-day fluctuations – that would eventually take the S&P 500 below the 700 level, wiping out more than 55% of the market’s value.

While we can't rule out an improvement in market internals that might reduce our immediate downside concerns, my impression is that the relatively contained, low-volatility environment we’ve observed in recent months is not likely to persist. Over the completion of this market cycle, investors are likely to observe significant scale dilation – as risk premiums normalize in spikes and volatility increases. The dilation from contained losses to vertical losses is one of the primary causes of investor panic, because the dilated movements feel so out-of-character with recent experience. Factor this sort of behavior into your expectations. That’s not an encouragement to sell, provided you’re following a disciplined investment program and your risk exposures are carefully aligned with your investment objectives and horizon. Still, I very much hope that investors who are accepting market risk here are actually able to tolerate that risk. Dow Theory: The Line Breaks For nearly a year, we’ve observed a sideways congestion area in the market, characterized by extreme valuations, deteriorating internals, and widening credit spreads. In our view, recent trading activity has represented the distribution of stock from value-conscious and economically-sensitive sellers, with accumulation by price-insensitive corporate buyback programs and reflexive dip-buyers convinced that stocks can go nowhere but higher. Though every share sold must also be purchased, it is the relative eagerness of the buyer or the seller that determines which way prices move. For that reason, breaks out of these congestion areas are often viewed as significant, particularly when the breaks are confirmed by multiple averages. Century-old writings by Charles Dow, Robert Rhea, William Peter Hamilton, and others associated these narrow ranges with potential reversals in the major trend, where the balance between different groups of investors shifts from greater eagerness to accumulate shares to greater eagerness to distribute them (or vice versa, when the market enters a congestion area at depressed valuations after extended losses). We don’t use Dow Theory explicitly in our own work, largely because we find that the broad uniformity and divergence of market internals across numerous individual securities, industries, sectors, and security types are more informative than using only the Dow Industrials and the Dow Transports. Still, investors should be wary of simplistic “tests” of Dow Theory (such as comparing the performance of the Transports to the Industrials, as if that alone is meaningful). Having codified and tested our own interpretation of Dow Theory, I’m convinced that the underlying principles are useful. The essence of Dow Theory is to consider both valuation and market action – particularly joint new highs, joint new lows, and joint violations of prior support or resistance levels. On Friday, after an extended period of extreme valuations, both the Industrials and Transports jointly broke the initial correction lows that followed their joint bull market highs. Under our interpretation of Dow Theory, the major trend has turned negative. Dow Theory is often misunderstood as a purely "technical" approach. Charles Dow would disagree. More than a century ago, he wrote “The best way of reading the market is to read from the standpoint of values. The market is not like a balloon plunging hither and thither in the wind. To know values is to comprehend the meaning of the movements of the market. Stocks fluctuate together, but prices are controlled by values in the long run.” With regard to market action, the central consideration of Dow Theory is the uniformity of fluctuations across multiple indices, specifically the Dow Industrials and the Dow Transports. The basic idea is that confirmation by both indices is indicative of a robust trend, while non-confirmation and divergence should put investors on alert for changes in market direction. A joint high by both indices, followed by corrections of several percent in each, subsequent rebounds in each, and then a joint break below the prior correction lows, is the essential sequence that defines a trend shift. As William Peter Hamilton wrote in 1922: “We can satisfy ourselves from examples that a period of trading within a narrow range – what we have called a ‘line’ – gaining significance as the number of trading days increases, can only mean accumulation or distribution, and that the subsequent price movement shows whether the market has become bare of stocks or saturated with an oversupply.” Notably, it’s essential for strength or deterioration to be confirmed across multiple indices. Robert Rhea emphasized this concept in 1932: “Conclusions drawn from the movement of one average, not confirmed by the other, generally prove to be incorrect.” The same lesson has been learned and re-learned by investors across a century of market cycles. When a previously overvalued, overbought, overbullish market is joined by internal deterioration – with numerous securities, sectors, industries and securities simultaneously breaking down, accepting market risk is typically not rewarded, and stocks instead become vulnerable to air-pockets, free-falls, and crashes. Range-bound markets, particularly at elevated valuations, often offer a false sense of security; making investors believe that their risk is low because day-to-day volatility is contained. Last week's market loss was initial and quite contained from the standpoint of current valuations. My view is that under the market conditions we presently observe, investors face the continued potential for steep, vertical losses. That outlook will change as market conditions change. I’ll emphasize, as usual, that the message here is not “sell everything.” The message is to understand where we are in the market cycle from the standpoint of a century of reliable evidence, and to act in a way that meets your investment objectives. Align your portfolio with careful consideration for your tolerance for losses over the market cycle; with your willingness to miss out on interim market gains should they emerge; with the horizon over which you will actually need to spend from your investments; with the extent that you believe that history is actually informative for making investment decisions; with the extent to which alternative investment outlooks are supported by evidence, ideally spanning numerous market cycles. I am not encouraging buy-and-hold investors to depart from well-considered investment plans or to abandon their discipline; only that they take every step to ensure their portfolio is actually aligned with their true risk tolerance and investment horizon. The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |