|

|

||||||

|

|

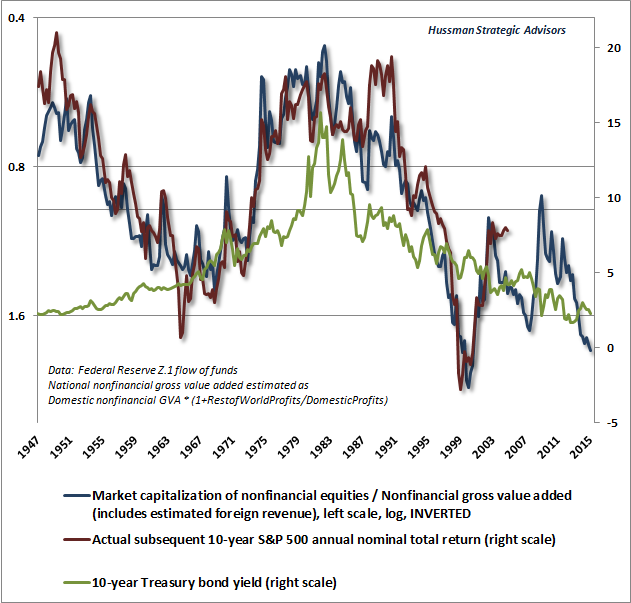

August 31, 2015 If You Need to Reduce Risk, Do it Now The single most important thing for investors to understand here is how current market conditions differ from those that existed through the majority of the market advance of recent years. The difference isn’t valuations. On measures that are best correlated with actual subsequent 10-year S&P 500 total returns, the market has advanced from strenuous, to extreme, to obscene overvaluation, largely without consequence. The difference is that investor risk-preferences have shifted from risk-seeking to risk-aversion. That may not be obvious, but in market cycles across history, the best measure of investor risk preferences is the behavior of market internals, as measured by the uniformity or divergence of market action across a wide range of individual stocks, industries, sectors, and security types, including debt securities of varying creditworthiness. Our observations on that are not new at all. Extreme overvaluation coupled with deterioration in market internals was the same set of features that allowed us to avoid the 2000-2002 and 2007-2009 market collapses. Given our success in prior cycles, why did we stumble in the advancing half of this one? The fact is that in 2009, I insisted on stress-testing our methods of classifying market return/risk profiles against Depression-era data, setting off a sequence of inadvertent but related challenges in the recent cycle, which we fully addressed last year. I’ve detailed the central lessons in nearly every weekly comment since mid-2014. The full narrative is detailed in our 2015 Annual Report. As I observed in the accompanying letter: If there is a single lesson to be learned from the period since 2009, it is not a lesson about the irrelevance of valuations, nor about the omnipotence of the Federal Reserve. Rather, it is a lesson about the importance of investor attitudes toward risk, and the effectiveness of measuring those preferences directly through the broad uniformity or divergence of individual stocks, industries, sectors, and security types. In prior market cycles, the emergence of extremely overvalued, overbought, overbullish conditions was typically accompanied or closely followed by deterioration in market internals. In the face of Fed induced yield-seeking speculation, one needed to wait until market internals deteriorated explicitly. When rich valuations are coupled with deterioration in market internals, overvaluation that previously seemed irrelevant has often transformed into sudden and vertical market losses. It may not be obvious that investor risk-preferences have shifted toward risk aversion. It’s certainly not evident in the enthusiastic talk about a 10% correction being “out of the way,” or the confident assertions that a “V-bottom” is behind us. But a century of history demonstrates that market internals speak louder than anything else – even where the Federal Reserve is concerned. Why did stocks lose half their value in 2000-2002 and 2007-2009 despite aggressive and persistent monetary easing? The answer is that monetary easing doesn’t reliably support speculation when investors have turned toward risk aversion, as indicated by the state of market internals. Why was I admittedly wrong in having such a defensive outlook during much of the advance in recent years? Because regardless of obscene overvaluation and historically offensive extremes in sentiment and overbought conditions, market internals suggested that investors and speculators were buying every shred of the risk-seeking recklessness that the Fed was selling. Why has the market become much more vulnerable to vertical losses since last summer? Because market internals have turned negative, indicating that investors have subtly become more risk averse, removing the primary support that has held back the consequences of obscene overvaluation. If the Fed is going to launch QE4 and QE5 and QE6, or if zero interest rate conditions are going to support speculation as far as the eye can see, those policies will only have their effect on stocks by shifting investors back toward risk-seeking, and the best measure of that shift will be through the observable behavior of market internals. We don’t expect that sort of shift at these valuations, but we can’t rule it out, and in any event we’ll respond to the evidence as it emerges. Given continued extremes in valuation, our own response would likely be to shift our outlook to something that could be described as “constructive with a safety net.” For now, our outlook remains hard-negative. If you need to reduce risk, do it now It’s important to recognize that the S&P 500 is down only about 6% from its record high, while the most historically reliable valuation measures are double their historical norms; a level that we still associate with expected 10-year S&P 500 nominal total returns of approximately zero. We fully expect a 40-55% market loss over the completion of the present market cycle. Such a loss would only bring valuations to levels that have been historically run-of-the-mill. Investors need not expect, but should absolutely allow for, a market loss of that magnitude. If your investment portfolio is well-aligned with your actual risk tolerance and the horizon over which you expect to spend the funds, do nothing. Otherwise, use this moment as an opportunity to set it right. Whatever you're going to do, do it. You may not get another opportunity, and if you're taking more equity risk than you wish to carry over the completion of this cycle, you still have the opportunity to adjust at stock prices that are close to the highest levels in history. The chart below offers a good idea of how little conditions have changed in response to the recent market pullback. The blue line shows the ratio of nonfinancial market capitalization to corporate gross value added, on an inverted log scale (so that equal movements represent the same percentage change). The slight uptick at the very right hand edge of the chart is barely discernable. That's the recent market selloff. Current valuations remain consistent with expectations of zero nominal total returns for the S&P 500 over the coming decade.

A final note on the impact of interest rates on expected and actual subsequent market returns, also from our Annual Report: “It is important to recognize that while depressed interest rates may encourage investors to drive risky securities to extreme valuations, the relationship between reliable valuation measures and subsequent investment returns is largely independent of interest rates. To understand this, suppose that an expected payment of $100 a decade from today can be purchased at a current price of $82. One can quickly calculate that the expected return on that investment is 2% annually. If the current price is given, no knowledge of prevailing interest rates is required to calculate that expected return. Rather, interest rates are important only to address the question of whether that 2% expected return is sufficient. If interest rates are zero, and an investor believes that a zero return on other investments is also appropriate, the investor is free to pay $100 today in return for the expected payment of $100 a decade from today. The investor may believe that such a trade reflects ‘fair value,’ but this does not change the fact that the investor should now expect zero return on the investment as a result of the high price that has been paid. Once extreme valuations are set, poor subsequent returns are baked in the cake.” Be careful to understand that argument correctly. Yes, low interest rates may encourage investors to drive stocks to extremely high valuations that are associated with low prospective equity returns. We certainly believe that as long as investor preferences are risk-seeking (as we infer from market internals), monetary easing and QE can encourage yield-seeking speculation that drives equities to recklessly extreme valuations. The point is that once valuations are driven to those obscene levels, low interest rates do nothing to prevent actual subsequent market returns from being dismal in the longer term. The low subsequent returns are baked in the cake. One might like to think that, well, maybe interest rates will be just as low a decade from now too, so valuations can remain high indefinitely. The problem is that there is a very strong correlation between the interest rates at the end of any 10-year period and nominal economic growth over that same period. So even if low rates a decade from now might support higher valuation multiples, interest rates will remain this low only if economic growth turns out to be dismal (our total return estimates generally assume nominal growth of 6% annually – see Ockham’s Razor and the Market Cycle for details on that arithmetic). Because those two effects tend to cancel out, it turns out that the relationship between reliable valuation measures and actual subsequent returns is highly insensitive to the level of interest rates. Again, yes – low interest rates may encourage higher valuations. But once those rich valuations are established, the nearly direct correspondence between valuation levels and actual subsequent market returns is largely unaffected by the level of interest rates. The following chart from May is a reminder of two things. First, the relationship between interest rates and valuations is much weaker than many observers seem to assume; and second, the close relationship between valuations and actual subsequent market returns is largely unaffected by the level of interest rates.

The upshot is this. Current valuations continue to imply approximately zero nominal total returns for the S&P 500 over the coming decade, coupled with the risk of a 40-55% market loss over the completion of the present market cycle – a loss that would only bring valuations to run-of-the-mill historical norms. An improvement in market internals would suggest a shift back to risk-seeking speculation among investors, and would defer the immediacy of our concerns. In the absence of that improvement, we continue to view the market as vulnerable to steep losses. As I noted early this year (see A Better Lesson than “This Time Is Different”), market crashes “have tended to unfold after the market has already lost 10-14% and the recovery from that low fails.” Prior pre-crash bounces have generally been in the 6-7% range, which is what we observed last week, so I certainly don’t see that bounce as having removed any of our concerns. We remain extremely alert to the prospect for much more extended market losses. Our outlook will change as the evidence does. Again, if your portfolio is well aligned with your risk-tolerance and investment horizon, given a realistic understanding of the extent of the market losses that have emerged over past market cycles, and may emerge over the completion of this cycle, then it's fine to do nothing. Otherwise, use this opportunity to set things right. If you're taking more equity risk than you can actually tolerate if the market goes south, setting your portfolio right isn't a market call - it's just sound financial planning. It's only fun to be reckless if you also turn out to be lucky. Market conditions are now more hostile than at any time since the 2007 peak. If you want to be speculating, and you can tolerate the outcome, then you're not taking too much equity risk in the first place. But it's one or the other. Can you tolerate a 40-55% market loss over the next 18 months or so? If not, take this opportunity to set things right. That's not the worst-case scenario under present conditions; it's actually the run-of-the-mill historical expectation. The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |