|

|

||||||

|

|

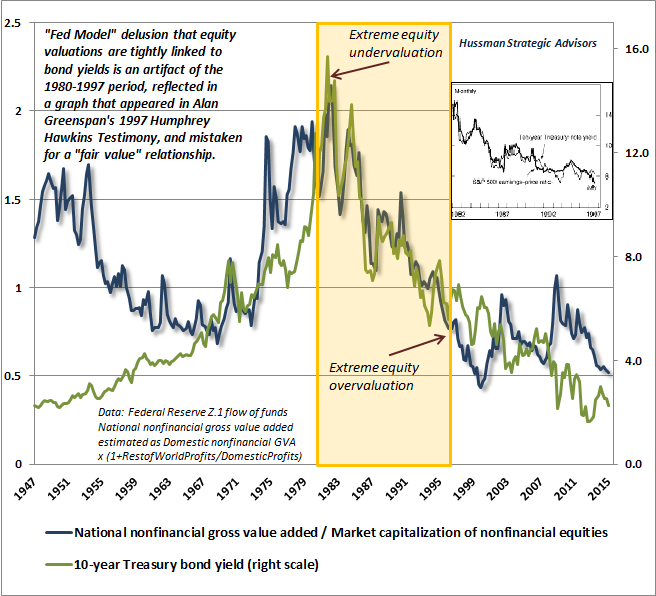

May 2, 2016 "Justified" Consequences Market conditions continue to be characterized by the likelihood of extremely poor long-term and full-cycle outcomes, with expected 10-12 year estimated S&P 500 nominal total returns in the 0-2% range, negative expected real returns on both horizons, and the continued likelihood of a 40-55% interim market loss over the completion of the current cycle; a decline that would represent only a typical run-of-the-mill cycle completion, based on valuation measures most tightly related with actual subsequent market returns across history. The degree of second-guessing regarding historically reliable valuation measures is perplexing, given that there has been no deterioration whatsoever in the correlation between these measures and subsequent market returns on a 10-12 year horizon (see the recent comment, Permanently High Plateaus Have Poor Precedents, and note that these measures have been just as reliable in recent cycles as they have been for the better part of a century). Yes, from a cyclical perspective, the psychological inclination of investors toward risk-seeking or risk-aversion, as conveyed by the uniformity or divergence of market internals, is essential in distinguishing overvalued markets that become more overvalued, and overvalued markets that drop like a rock. This is where the Federal Reserve regularly exerts its recklessly misguided and needlessly distorting impact, amplifying risk-seeking when investors when already inclined to speculate, and becoming impotent once investors shift to risk-aversion (see When an Easy Fed Doesn't Help Stocks), but this is a distinction that plays out over shorter segments of the market cycle. To a large extent, the second-guessing of historically reliable valuation measures revolves around the meaning of the word “justified.” Specifically, many investors have been led to accept the premise that current extreme valuations are justified by the today’s suppressed level of interest rates. There are two responses to this premise. First, the correlation between interest rates and equity valuations is far weaker than investors seem to believe, and even the modest inverse correlation in historical data (lower interest rates being associated with higher valuations) is fully attributable to the disinflationary period from 1980-1997. Outside of this period, the historical correlation between interest rates and valuations has been zero. If one excludes the full inflation-disinflation period from 1970-1997, the correlation between interest rates and valuations has actually been modestly positive; lower interest rates have been correlated with lower, not higher, valuations. The back-story here is that when interest rates are super-low, it's typically because nominal growth has been crummy. Whenever investors have responded to depressed interest rates by paying extreme valuations anyway, they've been sorry (see Rarefied Air: Valuations and Subsequent Market Returns, for more detail, including a mathematical decomposition). Extreme valuations, on historically reliable measures, are invariably associated with dismal subsequent returns on a 10-12 year horizon. As much as one might protest the historical evidence, there’s no use getting upset over a fact. The following chart, which I presented last May near the peak in the S&P 500, is a reminder that the assumed one-to-one relationship between valuations and 10-year Treasury yields (the so-called “Fed Model”) is wholly an artifact of the disinflationary period from 1980-1997. Of course, I made the same point at the market highs in 2007, before the global financial crisis (see Long Term Evidence on the Fed Model and Forward Operating P/E Ratios). Nobody believed it then, either. When market risk has been rewarding for an extended period of time, investors refuse to accept that “risk” truly means “risk” until they actually suffer a major loss. As I observed in that cycle, even in periods when lower yields have been associated with higher valuations, the meaning of that for investors has not been positive or even neutral. It has been decidedly negative because those elevated valuations have been reliably associated with poor subsequent market reutrns.

The second response to the second-guessing of reliable valuation measures is to ask investors to define the word “justified.” Are current valuations justified by the zero-interest policy of the Federal Reserve? Well, if “justified” means that U.S. equities should also be priced to deliver near-zero returns over the coming 10-12 year period, and if the prospect of coming out with no returns at all is fully acceptable compensation for the strong likelihood that the S&P 500 will lose half its value in the interim, on its way to those zero 10-12 year total returns, then sure, current market valuations are justified. Understand that this is the bargain, though, because there’s not a single instance in history when valuations have been similarly extreme - not 1901, not 1907, not 1929, not 1937, not 2000, not 2007, and not even lesser extremes such as 1973, when the S&P 500 did not complete its cycle from those valuation extremes by losing half of its value. Of course, those instances include periods prior to the 1960’s when interest rates did, in fact, regularly hover near levels similar to the present. From the perspective of the full market cycle, I continue to view the equity market as tracing out the arc of a large, extended top formation. Despite the strong rebound from the February lows, the S&P 500 remains that the same level it registered in November 2014, and the NYSE Composite is at the same level it registered in March 2014. The S&P 500 has fluctuated in a 14% range during this 18-month top formation. I’ve frequently noted that major market crashes have typically been preceded by a loss of about 14%, followed by a sharp rebound. It’s the later break below that threshold that has generally opened a trap-door on the downside, which I continue to be concerned would occur on a violation of the 1820-1850 level on the S&P 500. The other important threshold that could provoke concerted efforts by trend-followers to exit is probably the widely-followed 200-day moving average, which stands just below the 2020 level. Meanwhile, very near-term market conditions are again mixed, following a brief shift from neutral to hard-negative last week. Last week’s decline took a bit of steam off of bullish sentiment, and a bit of the edge off of strenuously overbought conditions. That combination was enough to make us again rather ambivalent about very short-term market prospects. If that doesn’t sound like a ringing endorsement of market risk, it’s for good reason. The most salient prospects for the market remain on the downside, and the greatest risk is that of profound losses, not of foregone gains. Still, our immediate view is again fairly neutral rather than hard-negative. As usual, our views will evolve as market evidence changes. Our primary source of optimism, of course, is the understanding that the strongest expected return/risk prospects for the market have always been associated with a material retreat in valuations that is then joined by an early improvement in market action. That opportunity has emerged during the completion of every market cycle in history. Contrary to my inadvertent mischaracterization as a “permabear”, I’ve responded to that opportunity by adopting a constructive outlook after every bear market loss in three decades as a professional investor. The challenge in the recent half-cycle is that, following a financial crisis and market collapse that we fully anticipated, our constructive shift in late-2008 was truncated by my insistence in 2009 on stress-testing our methods against Depression-era data - see the “Box” in The Next Big Short for the complete narrative, and how we’ve addressed and adapted to the challenges that followed. Please read and understand that narrative, lest our experience during the difficult transition from 2009 to mid-2014 leads you to ignore the severe cyclical and long-term risks that are inherent in obscene valuations here. In sum, our immediate, near-term view is rather neutral here. Our cyclical view remains that the market continues to trace out the arc of a broad top-formation, and we would view a 50% market loss as a wholly run-of-the-mill outcome over the completion of the current market cycle. Marginal new highs in the market would not change those views any more than the marginal new high in October 2007 changed our expectations prior to the global financial crisis. Our long-term estimate of expected 10-12 year S&P 500 nominal total returns remains in the range of 0-2% annually, with negative expected real returns on both horizons. Those who are comfortable with these prospects and attendant risks, believing that zero interest rate policy “justifies” historically obscene valuations on highly reliable measures (and the dismal long-term outcomes these valuations imply, and have always implied across history), are certainly welcome to view current market valuations as “justified.” Hey, knock yourself out.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |