|

|

||||||

|

|

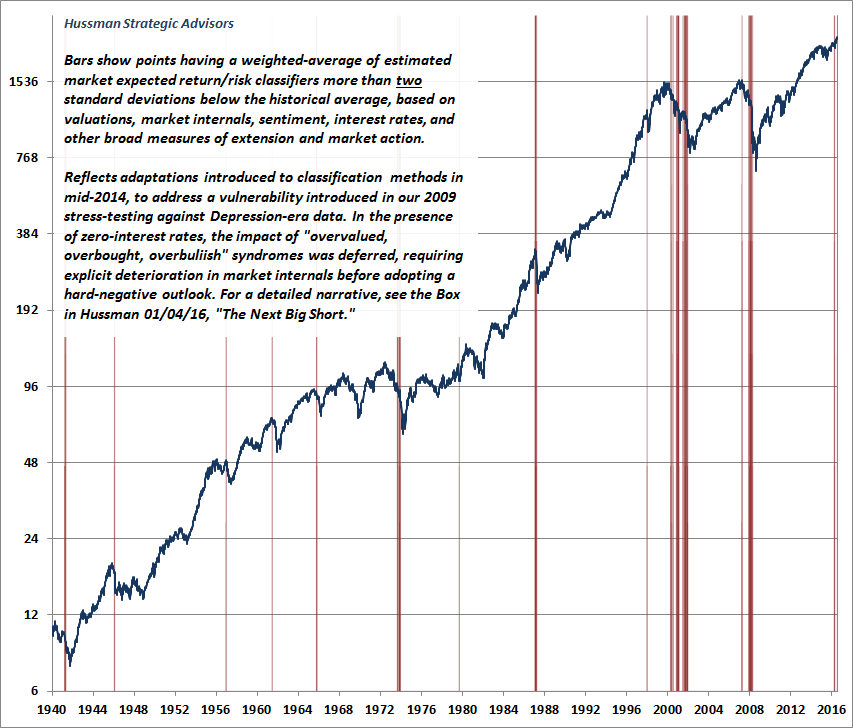

February 6, 2017 Portfolio Strategy and the Iron Laws A few weeks ago, we observed the single most extreme syndrome of “overvalued, overbought, overbullish” conditions we identify (see Speculative Extremes and Historically Informed Optimism) at a level on the S&P 500 4% higher than the syndrome we observed in July. The S&P 500 has climbed about 1.5% further since then, and all of the features of this syndrome remain in place. As I noted in December, except for a set of signals in late-2013 and early-2014 (when market internals remained uniformly favorable as a result of Fed-induced yield-seeking speculation), an overextended syndrome this extreme has only emerged at the market peaks preceding the worst collapses in the past century. Prior to the advance of recent years, the list of these instances was: August 1929, the week of the bull market peak; August 1972, after which the S&P 500 would advance about 7% by year-end, and then drop by half; August 1987, the week of the bull market peak; July 1999, just before an abrupt 12% market correction, with a secondary signal in March 2000, the week of the final market peak; and July 2007, within a few points of the final peak in the S&P 500, with a secondary signal in October 2007, the week of that bull final market peak. Two weeks ago, we observed a fairly rare set of “crash signatures” that we associate with the risk of market losses in excess of -25%, generally over a period of about 6 months. No single variable drives these signatures. Rather, they capture infrequent combinations of market conditions that may include offensive valuations, dispersion across market internals, credit market weakness, lopsided bullish sentiment, Federal Reserve tightening, or other features which, in combination, have historically preceded steep and compressed plunges in the market. These signatures are designed to identify the most hostile points in a market cycle. The last three times these features were in place to the same extent were: Apr-Oct 2008, Mar-May 2002, and Aug-Sep 1987. Last week, an additional class of risk signatures, typically active in only a small percentage of historical data, shifted to warning mode. To offer some idea of the risk profile we are estimating here, the chart below reflects a blend of several types of classifiers we’ve developed over the years. These include estimates of the expected market return/risk profile on horizons ranging from 2 weeks to 18 months, as well as signatures we associate with specific “events,” such as air-pockets, panics and crashes. The bars show points where a blended composite of these estimates was at least two standard deviations below average, as it is presently. There's no assurance that future outcomes will be similar, but most of these instances were rather challenging for investors.

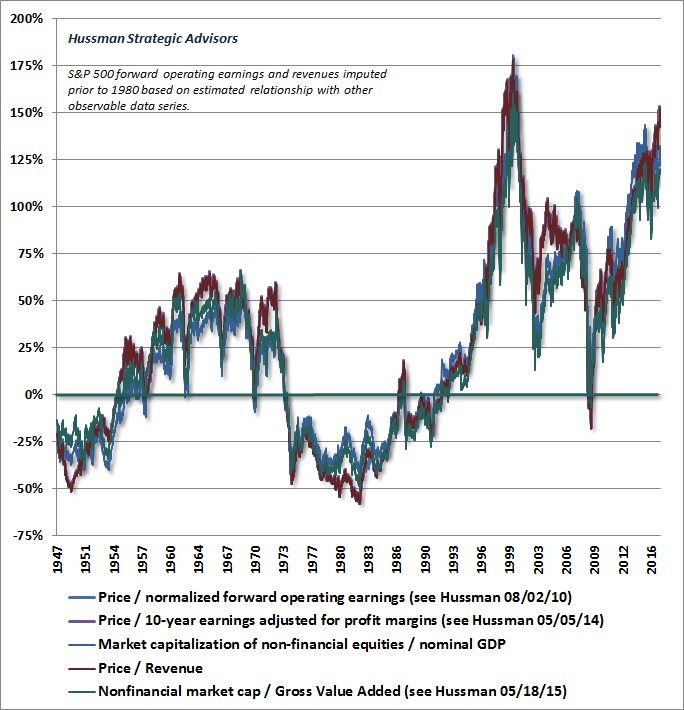

Still, as I noted several weeks ago, it’s important to recognize that these are not forecasts. They are signatures of causes and conditions that create a permissive environment for what would otherwise be highly unusual events. The difference is that a forecast says “we expect this particular outcome in this specific instance,” while a classifier says “we identify the same signature of conditions that has regularly preceded this particular outcome in the past.” It’s a subtle distinction, but an important one. We needn't rely on forecasts. Rather, we continue to align ourselves with the prevailing evidence at each point in time, and our outlook will shift as the evidence does. On the advancing half-cycle since 2009, and the completion ahead Having anticipated both the 2000-2002 and 2007-2009 market collapses, and having advocated a constructive or even leveraged investment outlook after every bear market decline across three decades in the financial markets, we’ve come out admirably over the course of complete market cycles - the notable exception being the advancing half-cycle since 2009. It’s impossible to appreciate present market risks without recognizing the difference between present conditions and those that prevailed during most of the period from 2009 through 2014. As I’ve frequently noted, our own difficulty in the recent half-cycle followed my insistence in early 2009, after a market collapse that we fully anticipated, to stress-test our methods against Depression-era data. The resulting methods improved the robustness of our discipline to Depression-like outcomes, but they also captured a historical regularity that turned out to be our Achilles Heel in the face of the Federal Reserve’s zero interest rate policy. In prior market cycles across history, the emergence of extreme “overvalued, overbought, overbullish” syndromes was regularly accompanied or quickly followed by a shift toward risk-aversion among investors (which we infer from the uniformity of market action across a wide range of securities and security types). Because of that overlap, these “overvalued, overbought, overbullish” syndromes, in and of themselves, could historically be taken as reliable warnings of likely air-pockets, panics, or crashes. Unfortunately, the Federal Reserve’s zero interest rate policies disrupted that overlap. With the relentless encouragement of the Fed, investors came to believe that there was no alternative to speculating in stocks, and even obscene valuations and overextended conditions were followed by further speculation. In the face of zero interest rates, it was necessary to wait until market internals deteriorated explicitly before adopting a hard-negative market outlook. We implemented that restriction to our approach in 2014. While that adaptation could have substantially postponed our shift to a durably negative outlook in recent half-cycle, even our adapted methods have been defensive since late-2014. This makes it tempting to infer that nothing has changed. Be careful. One should distinguish between defensive action taken in the presence of counteracting factors (zero-interest rate policy of an easing Fed, uniformly favorable market internals) and the identical action once those factors are removed. It would take only a modest correction to wipe out the gain in the S&P 500 since late-2014. Our expectation is that far deeper market losses are ahead. Our current defensiveness is driven by the same causes and conditions that allowed us to anticipate the 2000-2002 and 2007-2009 collapses. Interest rates have moved off the zero bound, and we observe market conditions that rank among the most overvalued, overbought, and overbullish in history, in an environment where our key measures of market internals lack the uniformity that was evident during the majority of the period from 2009 through late-2014. All of that opens the prospect for enormous downside risk. Even if changes in economic policy are effective in producing a percent or two more growth (and my concern is that the present direction is more likely to produce instability), it would not matter much to a market where the most reliable valuation measures are about 2.5 times their historical norms. Don’t assume that Fed easing will prevent the completion of the present cycle either. The Fed eased persistently and aggressively through the entire course of the 2000-2002 and 2007-2009 declines. It’s not Fed easing itself that matters, but the state of investor risk preferences. Recall that I shifted to a constructive outlook in late-2008 after the market had lost more than -40% of its value, on the view that stocks had become undervalued. By that point, we had capably and repeatedly demonstrated the advantages of a value-conscious, historically-informed, risk-managed, full-cycle investment discipline. Without my 2009 insistence on stress-testing our methods against Depression-era data, and the inadvertent challenges that resulted, I can’t imagine that anyone would view our increasing concerns since late-2014 as unreasonable, particularly the face of one of the most offensive speculative extremes in history. As things are, pointing at our own difficulties during the recent this half-cycle is a convenient way to ignore the repeated lessons drawn from a century of market evidence. Yet given current valuation extremes and an onslaught of extreme risk signals and crash signatures, I expect it will also prove to be a convenient way to lose 50-60% of one’s assets over the completion of the current market cycle. That loss estimate for the S&P 500 Index may seem preposterous, but our risk projections in 2000 and 2007 seemed equally preposterous. As I noted in prior cycles, adhering to a value-conscious discipline can feel excruciating during a late-stage bull market advance, but the market tends to be very forgiving of early exit by the time the cycle is complete. I’ve spoken my truth. Investors are free to do with it what they will. Portfolio strategy and the Iron Laws I’ve often emphasized principles of investing that I call the “Iron Laws”. The Iron Law of Valuation is that every security is ultimately a claim to some future set of cash flows. The higher the price an investor pays for a given set of future cash flows, the lower the long-term return the investor will enjoy as those cash flows are delivered. Valuations are the primary determinant of investment outcomes on a 10-12 year horizon, as well as prospective market risks over the completion of a given market cycle. Over shorter segments of the market cycle, however, the difference between an overvalued market that becomes more overvalued, and an overvalued market that crashes, has little to do with the level of valuation and everything to do with investor risk preferences. The Iron Law of Speculation is that the near-term outcome of speculative, overvalued markets is conditional on investor preferences toward risk-seeking or risk-aversion, and those preferences can be largely inferred from observable market internals and credit spreads (when investors are inclined to speculate, they tend to be indiscriminate about it). Investors and even financial professionals rarely recognize asset bubbles while they are in progress. As the price of a financial asset rises, investors have an increasing tendency to use the past returns and the past trajectory of the asset as the basis for their future return expectations. The more extended the advance, and the higher valuations become, the more stable and promising the investment can appear to be, when judged through the rear-view mirror. That extrapolation was at the root of the tech bubble that ended in 2000, and the mortgage bubble that ended in 2007. It is also at the root of the very mature bubble that has again been established today. The exodus of investors from flexible investment disciplines to passive investing and indexing, at valuations that are among the most obscene in history, is a symptom of a performance-chasing mentality dressed in the clothing of prudence. I’ve detailed the relationship between multiple, historically reliable valuation measures in scores of prior weekly comments, but the following two charts will suffice to highlight present risks. The first presents several of the most reliable measures we identify (those having the strongest correlation with actual subsequent S&P 500 total returns in market cycles across history). These are shown as percentage deviations from their historical norms. At present, the most reliable valuation measures across history rival the extremes observed in 2000, and range between 125-150% above (2.25 to 2.5 times) historical norms. No market cycle in history has been completed without taking these measures at least 40-50% below present levels. Our actual expectation is a market retreat on the order of 50-60% over the completion of the current cycle.

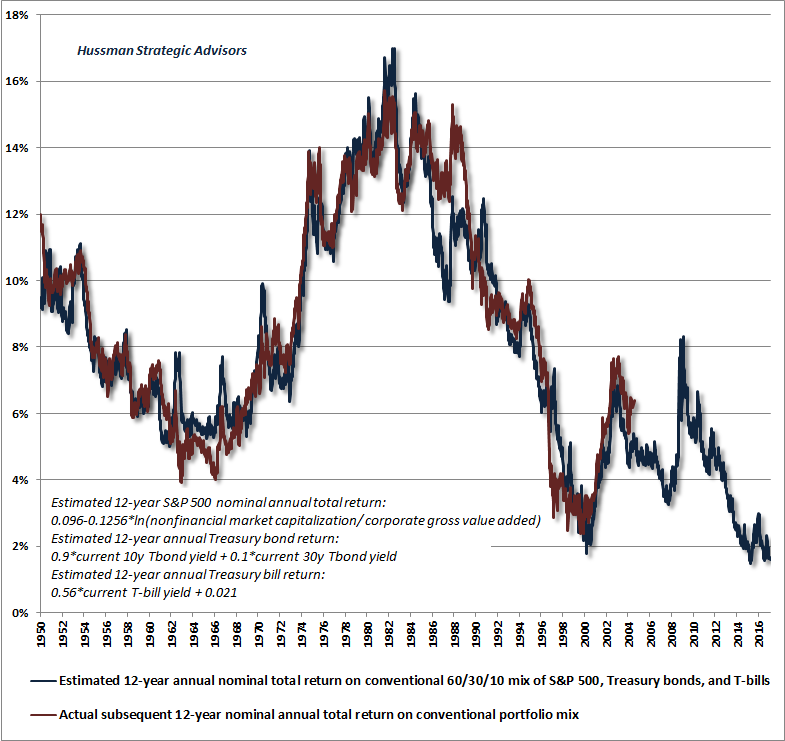

With respect to conventional investment strategies, understand that holding a fixed, static allocation to stocks and other investment classes, regardless of their valuations, is implicitly an active investment strategy. At rich valuations, it is a strategy that lengthens the effective maturity of the portfolio and increases exposure to risk, even though prospective long-term returns have diminished. At depressed valuations, it is a strategy that shortens the effective maturity of the portfolio and reduces exposure to risk, even though prospective long-term returns have increased. A static allocation does that automatically, as a consequence of how discounted cash flows operate. Failing to rebalance simply amplifies this outcome. See, as a bond increases in price and its yield-to-maturity falls, the effective duration of that bond increases, as does its sensitivity to risk (in the limit, a zero-coupon bond has a duration equal to the number of years to maturity). Likewise, we’ve shown elsewhere that the effective duration of the stock market is essentially the price/dividend ratio, which is presently close to 50. Given current market valuations, a portfolio allocated 60% to stocks, 30% to bonds, and 10% to cash has an effective duration of about 33 years. At historically normal valuations, the same portfolio would have an effective duration of roughly half that. Understand that the identical portfolio allocation may be appropriate for investors with very different investment horizons and risk tolerances, depending on the prevailing level of valuations. Moreover, rich valuations embed poor prospective long-term returns, while depressed valuations embed high prospective long-term returns. Investors, pension funds, and investment committees who are presently adopting passive, indexed, fixed-allocation strategies are effectively locking in both high risks and dismal expected returns. The chart below presents estimated and actual subsequent total returns for a conventional 60-30-10 mix of stocks, bonds and cash. On a 12-year horizon, we estimate likely nominal total returns on such a portfolio to average about 1.6% annually. The Iron Law of Equilibrium is that someone will have to hold these assets, at every point in time, until they are retired. Accordingly, there is no way for investors, in aggregate, to avoid present market risks, and there is no point in encouraging them to sell. What I do strongly encourage is that investors carefully assess their own investment horizon and risk tolerance, allowing for what we view as a strong potential for market losses similar to those we anticipated in 2000-2002 and 2007-2009. If you can accept rather weak long-term return prospects, and the risk of interim losses on the order of 50-60% in the S&P 500, do nothing and stick to your discipline. Otherwise, carefully examine your risk exposures and establish a portfolio that would allow you to maintain your discipline in the event these expectations are realized (whether you share these expectations or not). In any case, recognize that a static-allocation strategy quietly embeds an active component that automatically elevates risk exposure at rich valuations. This elevated risk is now coupled with the poorest long-term return prospects in history.

The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |