|

|

||||||

|

|

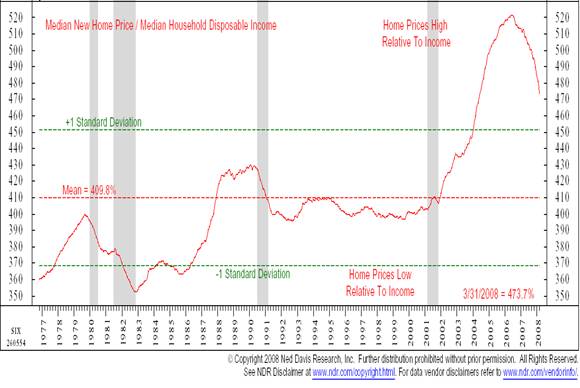

May 12, 2008 Round Two - Home Price Erosion With the U.S. stock market still relatively overbought in an unfavorable Market Climate, there is continued risk of substantial and possibly abrupt stock price weakness. As I've noted frequently, I rarely have much of an opinion on near-term direction except when conditions are either overbought in an unfavorable Climate or oversold in a favorable one. We observed some initial weakness late last week, but we remain braced for more significant trouble. At the same time, we have to recognize that the rebound through early last week brought market internals not far from the point that would begin to feed purely speculative "trend chasing." So while we're defensive here, you can think of us as having something of a "stop" at which we would cover part of our short-call option hedges (leaving the defensive puts in place) - effectively trading some risk of time decay in return for a modest exposure to rising prices in the event that investors become resolutely speculative. Again, here and now, we remain firmly hedged based on prevailing conditions, and my opinion (which we don't trade on) is that we should allow for fresh short-term trouble as well. Last week, CNBC aired an interview with Martin Feldstein, the president of the National Bureau of Economic Research (the group that officially dates U.S. recessions). Feldstein is a professor of economics at Harvard, was President Reagan's chief economic advisor, and is among the most respected U.S. economists across both political parties. He was the logical choice - and certainly my preference - for Federal Reserve Chairman (John Taylor from Stanford being the other), and was one of the only leading economists to have correctly gauged the scope of the oncoming credit crisis even in mid-2007 when the stock market was hitting fresh highs. Among Feldstein's comments was the observation that GDP is a quarterly average of 3 months, so the positive mark for GDP during the first quarter was actually quite misleading about the direction the economy has been taking. It reflects a rise from the average level during the fourth quarter of 2007 to the average level during the first quarter. He noted "if you compare where the economy was at the end of March with where the economy was at the beginning of the year, there's no question the economy is down by just about every measure." Feldstein reiterated the view he expressed in a Financial Times editorial on Wednesday: "Monthly data since January indicate that economic activity and GDP have been declining since the start of this year... The misstatement that the economy expanded in the first quarter creates an inappropriately sanguine view of the months ahead and therefore reduces the prospect of strong action to prevent the deep decline that may otherwise occur." Again - this from the head of the group that officially dates U.S. recessions. Equally important were his remarks about economic prospects, and the risk of placing too much faith in the Federal Reserve to manage those risks. These comments should not be missed: "To me, the big question is what happens as more and more homes move into negative equity - as more and more people see that the value of their mortgages exceeds the value of their homes. If we see a big increase in defaults, ultimately in foreclosures, that's going to push us definitely into a significant recession. "I think there's not much more that the Fed can do to help us in this situation. They've used up half their balance sheet setting up credit lines to take on questionable credits from the banks and the securities firms. They've brought interest rates down to the point where we have negative Fed Funds rates. So I think the policy shifts to the Administration and the Congress if we're going to put a floor under these house prices. "I'll tell you what worries me. We saw house prices overshoot by 60% relative to costs of building and relative to rents. And I worry about the possibility that they will keep falling; they will spiral downwards. In the same way that they went much too high, they could go much too low. And if that happens, then we are going to see individuals feeling a lot poorer, cutting back on their spending, defaulting on mortgages, and we're going to see the holders of those mortgages see their assets, their capital being cut and therefore their ability to make loans being cut. "So I think that there is a role to prevent this kind of downward overshooting of house prices. Prices have to fall somewhat from where they are today, but I think the danger is we have so many loan-to-value ratios greater than 100%, and those individuals are going to have a very strong temptation to simply turn in the keys and walk away because there's nobody to negotiate with. These mortgages have been securitized to the point where they cannot simply sit down across the table with the mortgage originator from their bank and work it out." The following chart, presenting the ratio of median home prices to median household income, is courtesy of Ned Davis Research. Note that the decline in home prices even through the first quarter is a fraction of what we can expect to observe over time. While the "mean" in this chart is biased higher by the elevated ratios we saw in recent years, the lower ratios observed prior to 1987 are also unlikely because they were associated with very high interest rates. Given those considerations, it appears that median home values as of 3/31/08 were probably 15%-20% above sustainable norms, though we may not observe the full adjustment in just one cycle. The relatively low level of short-term interest rates (though only partially translating to low rates on adjustable mortgages) will probably help to buffer the full extent of the potential decline, but there's little doubt that we'll observe further serious defaults, foreclosures, and credit losses.

From a public policy standpoint, Feldstein is suggesting that structured finance and securitization (i.e. chopping up different streams of mortgage payments into dozens of separately traded securities) has created what economists call a "coordination failure" that may require government intervention to address. Frankly, I don't think the prospects are good that government intervention will catch anything but the tail end of this problem, because policy takes time to develop, and the defaults are already largely baked in the cake. What happened here is that the markets tolerated a huge "principal/agent" problem, where the people who were originating the mortgages ("agents") didn't really have anything at stake, and could sell mortgage debt to willing buyers ("principals") who would fund those loans in the belief that they were getting nice AAA paper. A lot of the money that was lent simply can't be paid back, because it was used to buy assets that were priced far in excess of sustainable market value. In short, far from the credit crisis being over, it's likely that we will see a troublesome second round that eventually provokes government intervention. The financial markets shouldn't take too much comfort from the idea of intervention, since it will almost surely be of the sort that forces the lenders to take losses while providing some sort of reduced principal workout to homeowners. Some of these proposals are already being discussed, but with limited urgency. My guess is that all of that is likely to change in the months ahead. Market Climate As of last week, the Market Climate for stocks remained characterized by unfavorable valuations and unfavorable market action. On the positive side, market action is still near the point where further improvement could feed investor speculation, which we would respond to by removing a portion of our short index calls in order to establish a limited exposure to potential advances (without removing our downside put option protection in any event). On the negative side, the prevailing Climate remains unfavorable, and overbought conditions in unfavorable Climates often invite abrupt and sometimes spectacular short-term weakness. Suffice it to say that we align ourselves with prevailing conditions - so we remain fully hedged - but we will respond to shifts in the prevailing Market Climate if the evidence changes sufficiently. In bonds, the Market Climate remains characterized by somewhat unfavorable yield levels and unfavorable market action. We did see Treasury yields back off on fresh concerns from AIG and Citigroup, among other financials. As I noted last week, fresh demand for Treasuries as safe havens is probable in the months ahead, but prevailing yields are already low enough that taking positions in Treasuries on that basis represents speculation rather than investment. To the extent that we observe some improvement in yield pressures, particularly on the inflation front, there may be some basis for increasing our portfolio duration. Presently, however, the Strategic Total Return Fund remains invested primarily in Treasury bills, which is unusual, but will change as market conditions shift. On last week's rally in precious metals shares, we clipped our exposure further, to just about 5% of assets. This is about our lowest allocation to precious metals shares since the Strategic Total Return Fund's inception in 2002. Meanwhile, given recent weakness in the euro and British pound, we added an allocation of about 10% of assets to foreign currencies. My impression is that commodity prices and the U.S. dollar will become less correlated in the months ahead. Though commodity prices are still in a frothy blowoff (making the ultimate highs uncertain), I do expect that we will observe a standard, run-of-the-mill, predictable, routine, and I-can't-believe-investors-don't-see-it-coming-a-mile-away commodity price "spike top" over the next few months or even weeks (stare at some historical charts), off of which prices are likely to decline with very little in the way of relief rallies. At the same time, further dollar weakness is likely as the U.S. economy slows and our need for foreign capital persists. As the decline in commodities in terms of "global" prices will probably be faster than the decline in the dollar, U.S. investors are likely to observe an unusual pattern of weakness in both commodities (as priced in U.S. dollars) and the U.S. dollar itself. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |