|

|

||||||

|

|

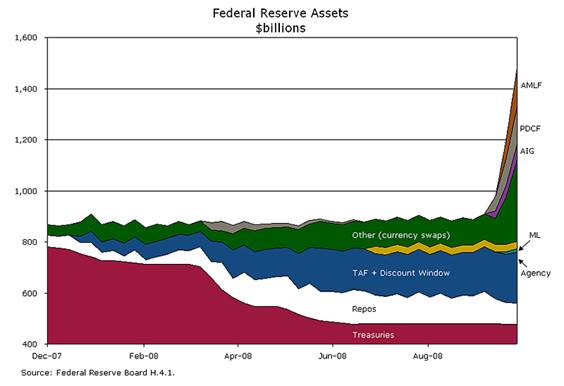

May 18, 2009 The Destructive Implications of the Bailout - Understanding Equilibrium One of the features that has enabled the bureaucratic abuse of the public during the past year has been the frantic, if temporary, flight-to-safety by investors. The Treasury has issued an enormous volume of debt into the frightened hands of investors seeking default-free securities. This has allowed the Treasury to finance a massive and largely needless transfer of wealth to bank bondholders so easily over the short-term that the longer-term cost has been almost completely obscured. But by transferring wealth from those who did not finance reckless loans to those who did - providing monetary compensation without economic production - the bureaucrats at the Treasury and Federal Reserve have crowded out more than a trillion dollars of gross investment that would have otherwise have been made by responsible people in the coming years, shifted assets to the control of those who have proven themselves to be irresponsible destroyers of capital, and have planted the seeds of inflation that will cut short any emerging recovery. In order to understand the impact of these interventions, you have to think in terms of equilibrium - recognizing that all securities that are issued must also be held by someone - and then follow the money. Initially, suppose you have a banking system with $12 trillion in assets, financed with about $7 trillion in deposits and other liabilities to customers, about $4 trillion in debt to the bondholders of the banks, and about $1 trillion in shareholder equity as a buffer against insolvency. Now, suppose that the value of the assets deteriorates by $1 trillion, effectively wiping out the shareholder equity and putting much of the banking system in an insolvent position. Suppose also that government bureaucrats refuse to properly take receivership of insolvent banks, to impose haircuts on the debt to bondholders or to require them to swap debt for equity. Instead, suppose these bureaucrats prefer to defend the private bondholders who funded the bad loans from experiencing any loss whatsoever, and are willing to use public funds to do it. In order to do this, the Treasury issues $1 trillion in government debt, with a preference toward shorter "money market" maturities (since it doesn't want to drive up long-term interest rates at the same time the Fed hopes to invigorate the housing market). It may seem like this means that there is $1 trillion of new "liquidity" in the economy, but you have to think carefully. If you look at various individuals in the economy, including yourself, notice that except for cold, hard currency in your wallet, whatever savings you have accumulated in the past have been allocated to finance investments that have already occurred. You may think that your stocks and bonds and bank CDs and money market securities represent your "savings," but they are actually securities that exist as evidence of money that has already been spent by some borrower, and on which you have some claim to future income or repayment. And this is crucial: the securities that represent those claims - the stocks, the bonds, the CDs - will all continue to exist until and those securities are retired. If you sell your stocks, or bonds, or money market securities, you have to sell them to someone who presently holds cash. In other words, in order for you to get cash that you can spend, you have to sell your securities to someone whose savings have not already been allocated to something. So where does the money come from to buy these new Treasury securities? Clearly, the sale of those securities must absorb the savings of someone in the economy whose savings have not already been claimed. Alternatively, the Fed can directly purchase those Treasury securities and literally print money. In practice, we have a third option. The Fed can acquire $1 trillion of commercial mortgage-backed securities and other assets from banks and create an equivalent amount of "reserves" (which is essentially printing money) at the same time that the Treasury issues the $1 trillion in new Treasury securities. In this case, which is in fact exactly what has happened, the banks that previously held $1 trillion in commercial debt securities can now use their newly acquired reserves to buy the $1 trillion in newly issued Treasuries. Having done this, they have no more money to lend than they had before. There is no more "liquidity" in the system than there was previously, except that the "quality" of the bank balance sheets has improved. The Fed has turned its balance sheet into a garbage dump, in order to accommodate all of the additional Treasury issuance required to finance the rescue of bank bondholders.

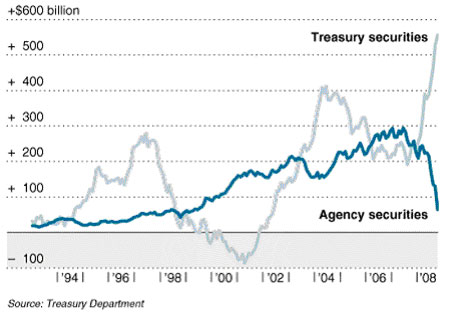

Incidentally, what we've observed in bank balance sheets (dumping mortgage related securities off on central banks and accumulating newly issued Treasury securities) is mirrored in the activity of foreign holders (year over year change in holdings depicted below):

In order to get these Treasury securities off the bank books so that the banks again have capital to lend, one of two things must happen: 1) Somebody other than the government would have to buy those Treasuries from the hands of the banks with new private savings that have not yet been allocated or spent. This means that in order to finance this bailout, the money that has been provided to make bank bondholders whole will have to come at the expense of crowding out more than $1 trillion of private investment that would otherwise have occurred, or; 2) The Federal Reserve would have to buy those Treasuries, in addition to the commercial securities it already holds, and create reserves to pay for them, which would add yet another $1 trillion to a base money supply that a year ago was less than $850 billion, and has already exploded to $1.8 trillion. In both cases, the bailout ensures that any incipient recovery will be cut short, because the only reason that our economy is able to absorb the present supply of government liabilities is extreme risk aversion that creates a demand for default-free instruments. If that risk aversion abates, it will quickly be replaced by higher short term interest rates, higher monetary velocity, and inflation that can be expected to be quite difficult to control. At that point all the Fed will be able to do is to swap one government liability (monetary base) for another (Treasury securities). The genie will not easily go back into the bottle. The bottom line is that the attempt to save bank bondholders from losses - to provide monetary compensation without economic production - is not sound economic policy but is instead a grand monetary experiment that has never been tried in the developed world except in Germany circa 1921. This policy can only have one of two effects: either it will crowd out over $1 trillion of gross domestic investment that would otherwise have occurred if the appropriate losses had been wiped off the ledger (instead of making bank bondholders whole), or it will result in a stunning and durable increase in the quantity of base money, which will ultimately be accompanied not by a year or two of 5-6% inflation, but most probably by a near-doubling of the U.S. price level over the next decade. As I've noted previously, the growth rate of government spending is better correlated with subsequent inflation than even growth in money supply itself, particularly at 4-year intervals. Regardless of near-term deflation pressures from a continued mortgage crisis, our present course is consistent with double digit inflation once any incipient recovery emerges. As Nobel economist Joseph Stiglitz recently noted, the bureaucrats that designed this bailout are "either in the pocket of the banks or they're incompetent. It's a real redistribution and a tax on all American savers. This is a strategy trying to recreate the bubble. That's not likely to provide a long-run solution. It's a solution that says let's kick the can down the road a little bit. They haven't thought enough about the determinants of the flow of credit and lending." Not that anyone is listening, unfortunately. The second fact is that as a result of more than a trillion dollars of new issuance of Treasury securities with relatively short durations, it is a tautology that there is a mountain of what is mistakenly viewed as "cash on the sidelines" invested in these securities. This mountain of "sideline cash" exists and must continue to exist as long as these additional government securities remain outstanding. It is an error to view outstanding debt securities as if they are "liquidity" poised to "flow back into the stock market." The faith in that myth may very well spur some speculation in stocks, but it is a belief that is utterly detached from reality. The mountain of outstanding money market securities is the result of government debt issuance that must be held by somebody until those securities are retired. It is not spendable "liquidity" - it is a pile of IOUs printed up as evidence of money that has already been squandered. The analysts and financial news reporters who observe this enormous swamp of short-term money market securities, and talk about "cash on the sidelines" as if it is spendable in aggregate immediately reveal themselves to be unaware of the concept of equilibrium and of the nature of secondary markets (where there must be a buyer for every security sold, and a seller for every security bought). If you sell your stocks or bonds or money market securities, they don't cease to exist. Somebody else has to purchase them. Somebody else has to hold them. As I've said numerous times, if Ricky wants to sell his money market funds and buy stocks, then his money market fund has to sell money market securities to Nicky, whose cash goes to Ricky, who uses the cash to buy stocks from Mickey. In the end, the cash that was held by Nicky is now held by Mickey. The money market securities that were previously held by Ricky are now held by Nicky. And the stocks that were once held by Mickey are now held by Ricky. There is exactly as much "money on the sidelines" after these transactions as there was before. Money doesn't go into or out of the stock market - it goes through it. Prices don't move because supply exceeds demand or demand exceeds supply. In equilibrium, the two are identical because that's exactly what a trade is. Prices move because the buyer is more eager than the seller, or vice versa. A note on savings and investment In recent months, we've increasingly heard analysts bemoaning the fact that the personal savings rate has increased, as if greater savings are inherently bad for the economy. Aside from the fact that the U.S. government has been running deficits (negative savings) that swamp any positive effect of personal savings, the larger issue is that analysts appear not to understand the importance of savings, or the link between savings and investment. Since the subject of this comment is equilibrium, a few notes about the savings-investment identity are appropriate. Let's begin with several basic premises (actually accounting definitions) Income that is not consumed represents "savings." Output that is not consumed represents "investment," even if it is unintentional "inventory investment." GDP can be defined as the total value of income or, equivalently, as the total value of output. These numbers are the same (aside from a purely statistical discrepancy). The total income in the economy is either consumed or it ends up financing "investment." The total output of the economy is either consumed or it represents "investment." Given these facts, total savings - by definition - are equal to total investment. In any economy, money flows from savers to investors will have occurred in a manner that makes this savings-investment identity true. If the money did not flow, then either the income was not earned, or the production and consumption did not happen. Whatever happens in the economy, and however it happens, we can be certain that when we add it all up at the end, total savings will have been equal to total investment. This is not a theory. It is algebra. It is an accounting identity. When people think of saving as something that depresses the economy, they are thinking of the Keynesian setup, where Keynes specifically and explicitly assumed that investment was constant. In that sort of setup, it is impossible for the economy as a whole to save more, since by definition, holding investment constant must also hold total savings constant. So the attempt to save a greater amount must fail. Let total savings S be equal to some percentage "s" of total income Y. Then S = sY. In Keynes' setup, the attempt to save a greater proportion of income as savings must result in a reduction in total income Y (or GDP). For example, suppose that total savings are $10 and GDP is $100, so that s = 10%. If you try to boost up s to 20% of income, but you're restraining total savings to $10, then GDP must fall to $50 (that is, $10 = 20% of $50). At present, it is not valid to say that the economy is weak because people are saving too much, because if gross savings were up, gross investment would also be up. One might say that the economy is weak because people are unsuccessfully attempting to save more, but it is far more accurate to say that the economy is weak because gross investment is collapsing despite a greater willingness of individuals to save. If we don't get those distinctions right, we'll end up with policies aimed at discouraging savings, which by their very nature will end up discouraging investment and will make the economy suffer interminably. Growth-oriented policies encourage new investment, and require an economy with the capacity to save in order to finance that investment. As long as we have a set of economic policies aimed at running massive government deficits at the same time individuals are encouraged not to save, we will risk driving this economy into the ground for a very, very long time. Market Climate As of last week, the Market Climate for stocks remained characterized by mixed valuations - modestly overvalued on the basis of most fundamental measures except those that assume a sustained return to the record profit margins of 2007, and slightly undervalued if one assumes that a return to those profit margins is a given. Market action was also mixed - volume continues to show fairly tepid sponsorship relative to durable market advances. Meanwhile, price action has been very favorable on the basis of breadth, but with the strongest leadership from industry groups with the least favorable balance sheets and financial stability. It is not typical for the industries that suffer worst in a bear market to be the ones that lead the subsequent bull market. That sort of "leadership by losers" however, is very characteristic of bear market rallies. That's not to say that we can immediately conclude that stocks are in a bear market advance as opposed to a new bull market, but as usual, we don't spend much of our energy making assumptions about things that aren't observable. At present, the observable evidence is that stocks are priced to deliver modestly sub-par long-term returns, but still in the range of about 8% annually over the coming decade, while market action is favorable enough for us to carry an index call option position in the range of 1-2% of assets here, in order to soften our hedge in the event that the market experiences a more sustained advance, without strongly compromising our defense against fresh weakness. Aside from that 1-2% in index calls, the Strategic Growth Fund continues to hold a strong hedge against the market risk of the stocks in the portfolio. In bonds, the Market Climate last week was characterized by modestly favorable yield levels and modestly unfavorable market action. From an investment standpoint, the prevailing yields on Treasury securities beyond about 5 years in duration are probably not sufficient to offset eventual inflation pressures, so longer maturities will function primarily as speculative as opposed to investment vehicles for a while. The Strategic Total Return Fund continues to emphasis TIPS, where real yields are still reasonable. Though there will probably not be much need for inflation compensation at short maturities, it will probably be important for longer maturities. The Fund also holds about 20% of assets divided between precious metals shares, foreign currencies and utility shares. The valuation of precious metals stocks remains generally favorable, particularly relative to gold prices, but the strongest returns are typically in environments where Treasury yields are falling and the rate of inflation is flat or rising (i.e. the combined environment features downward pressure on real yields and the U.S. dollar). Those pressures haven't been strong recently, so while we continue to hold precious metals shares here, the strongest returns are likely to emerge once downward pressure on the U.S. dollar picks up again. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |