|

|

||||||

|

|

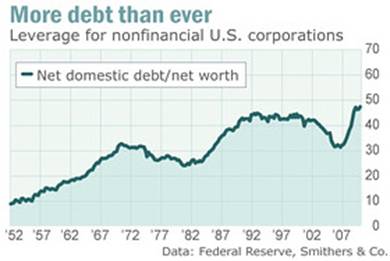

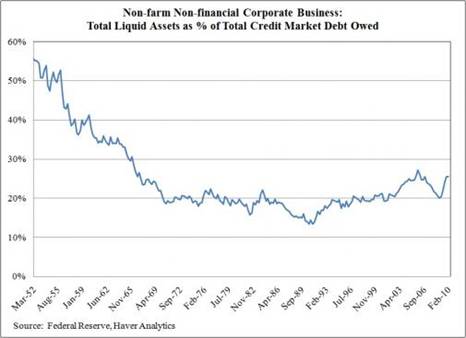

August 9, 2010 Corporate "Cash" - Cheering the Asset and Ignoring the Liability Just a note - if there is one weekly comment that I hope that regular readers of these comments will not miss, it is last week's piece - Valuing the S&P 500 Using Forward Operating Earnings. Economic risks and credit strains will come and go, but one thing that will remain important to investors over the very long-term is the ability to properly assess stock valuations. I know that last week's comment had more math than usual, which isn't everybody's cup of tea. But it's nothing that you can't do on a standard calculator, and even if you don't use the equations, I strongly encourage investors to read the comments carefully. It's not always obvious to the listener when an analyst's argument is full of holes, but you should always be on red alert when a single year of earnings is taken, at face value, as the basis for market valuation. If you passively accept that premise without training your neurons to revolt like little Frenchmen at the gates of the Bastille, you'll be at the mercy of all sorts of false and misleading claims about valuation based on models that have absolutely no predictive reliability in historical data. In the absence of historical evidence, people can say anything they want without accountability. If there is one thing that is singularly responsible for the abysmal returns of the S&P 500 over the past 12 years, it is the ludicrous set of valuation "models" that Wall Street has repeatedly foisted onto an uninformed public in order to sell them on the notion that dangerously overvalued markets were actually "cheap." Knowledge is your best defense. Valuation matters. Corporate "cash on the sidelines" Four years ago, in There's No Such Thing as Idle Cash on the Sidelines, I observed: "Investors should not believe that the "cash on the balance sheets" of corporations might suddenly be used, in aggregate, for new investments and capital spending. That cash on their balance sheets has already been deployed as loans to the Federal government and to other companies. Now, yes, if the government runs a surplus and retires its debt, in aggregate, or the other companies that borrowed the money generate new earnings and then pay off their debt, in aggregate, then those new savings that retire the T-bills and commercial paper then make it possible for the recipients to finance new investment, in aggregate. So as usual, savings equals investment, and new savings can finance new investment. But what investors often point to and call "cash on the sidelines" is really saving that has already been deployed and used either to offset the dissavings of government or to finance investments made by other companies. Once those savings have been spent, you can't, in aggregate, use the IOUs (in the form of money market securities) to do it again." Now, as then, analysts are pointing to an apparent pile of corporate "cash on the sidelines" as if these holdings of debt securities somehow make new corporate spending more likely. In order to evaluate this argument, it's necessary to understand that what is being called cash is actually a stack of IOUs for money that has generally already been spent by other companies or by the government. Don't get me wrong. At an individual company level, it's obvious that if DuPont has a bunch of marketable securities on its balance sheet, it is free to sell those securities and spend the money on new equipment and so forth. The issue is that somebody else has to buy those securities. At the end of the day, there is no less "cash on the sidelines" after that change of ownership than there was before. Put simply, there is a lot of apparent "cash on the sidelines" because the government and many corporations have issued enormous quantities of new debt, often with short maturities, while other corporations have purchased it. It is an equilibrium. The assets that are held in the right hand represent debt that is owed by the left. You cannot call that pile of short-term marketable securities an asset without calling it a liability. The cash on the sidelines is evidence of debt incurred to fund economic activity that is already in the past. It will remain "on the sidelines" until the debt is retired. The government debt has been issued to finance deficit spending. At the same time, a great deal of corporate debt has been issued over the past year apparently as a pre-emptive measure against the possibility of the capital markets freezing up again. What's fascinating about the "corporate cash" argument is that few observers recognize that a great deal of this cash is not retained earnings but new debt issuance. Brett Arends of MarketWatch puts present levels of corporate cash in perspective: "According to the Federal Reserve, nonfinancial firms borrowed another $289 billion in the first quarter, taking their total domestic debts to $7.2 trillion, the highest level ever. That's up by $1.1 trillion since the first quarter of 2007; it's twice the level seen in the late 1990s. Central bank and Commerce Department data reveal that gross domestic debts of nonfinancial corporations now amount to 50% of GDP." Andrew Smithers observes that the prevailing corporate debt burdens, " un derline the poor state of the U.S. private sector's balance sheets. While this is generally recognized for households, it is often denied with regard to corporations. These denials are without merit and depend on looking at cash assets and ignoring liabilities."

Similarly, Annaly Capital notes " in relation to their debt outstanding, corporations are less liquid than they were prior to the recession" (HT: The Pragmatic Capitalist / Business Insider)

As with job creation, new investment is not driven by the amount of cash on hand, but by anticipation of profitable activity and fear of excessive demand that exceeds capacity. There is little evidence that these considerations are powerful at the present time. [Geek's Note - One of the clear outliers in this regard is information technology, where inexpensive 64-bit computing and the ability to work with vastly more random access memory is a real bonus for number crunchers like us, and probably to a lot of other companies. For that reason, we would expect business investment on upgraded systems to remain strong. Unfortunately, that's a fairly small sliver of the economy. There are a few other pockets of growth potential as well, but at present, there's no "big idea" such as personal computers in the 1980's or internet/network expansion in the 1990's to drive a sustained economy-wide burst in corporate spending.] Market Climate As of last week, the Market Climate for stocks was characterized by unfavorable valuations, generally favorable trend action, weak price-volume sponsorship, strongly overbought conditions, moderate but not yet overbullish sentiment, and hostile economic pressures. Overall, this is not a favorable set of conditions in terms of the expected return/risk profile for the market, but urgent downside concerns would require more internal damage than we have at present. Over the short-term, the market appears likely to be driven by speculative considerations such as whether the S&P 500 crosses above or below some technical support or resistance level. This is clearly the most prevalent "game" that investors are playing at present, but that game is likely to end abruptly if we observe further deterioration in new unemployment claims, ISM data and other coincident measures. As I noted last week, the deterioration we've seen in various leading economic composites would be consistent with a sharp deterioration in the ISM figures for August and September, as well as a spike in new unemployment claims closer to the September - October time frame. Last week's jump in claims was still a bit "early" from the standpoint of typical lag times, so I'll actually be somewhat surprised if the data continue to deteriorate right away. Still, the overall weight of the data suggests a much greater likelihood of economic weakness than investors seem to be anticipating. If we don't observe clear weakness in the economic data in the next couple of months, we'll clearly move with the data toward a more constructive economic outlook - particularly if the leading measures improve as well. For now, however, regardless of very short-term speculative factors, I view the present window as a very dangerous one. The Strategic Growth Fund remains fully hedged. In bonds, the Market Climate remained characterized last week by moderately unfavorable yield levels and favorable yield pressures. The Strategic Total Return Fund has a duration of about 4 years, mostly in intermediate term, straight Treasury notes. Meanwhile, despite long-term inflationary implications of our fiscal imbalances, disinflationary pressures are likely to remain strong for a while. Dollar weakness is providing some good support for commodities here, but credit concerns would reverse that support quickly, so anyone speculating in commodities here had better pay very close attention to credit spreads and be ready to cut losses quickly. For our part, we prefer more durable investment opportunities, which I would expect some time after we observe weakness in coincident economic measures. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |