|

|

||||||

|

|

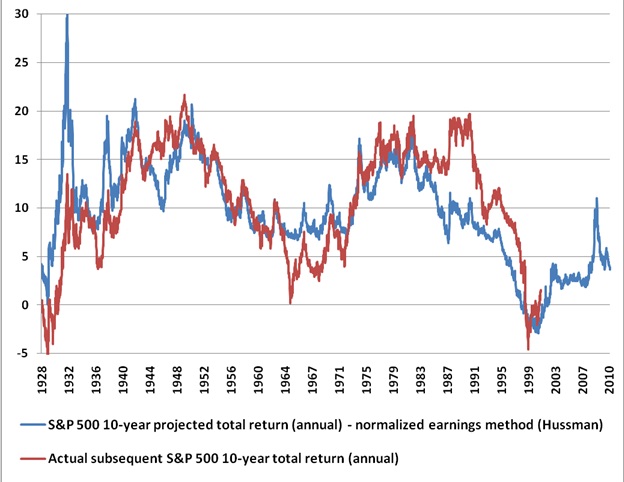

January 17, 2011 Borrowing Returns from the Future It will come as no surprise that we continue to anticipate poor 10-year total returns for the S&P 500 over the coming decade. Our present estimate is about 3.3% annually, which includes dividends. That is about 1% less than the 10-year total return that we estimated just a few months ago, but this should make sense: historically, to the extent that the S&P 500 appreciates at an annualized rate of more than about 6% (which is about the long-term growth rate of revenues, nominal GDP and other smooth fundamentals), the expected future total return for the index declines as the market advances. Just like bonds. It is easily understood, but often ignored, that a short-term market advance of 10% - leaving fundamentals relatively unchanged in the interim - cuts about 1% annually off of subsequent 10-year market returns. This can be demonstrated both algebraically and in historical data. The chart below plots our projections for 10-year annual total returns on the S&P 500 (standard methodology) versus actual subsequent 10-year total returns.

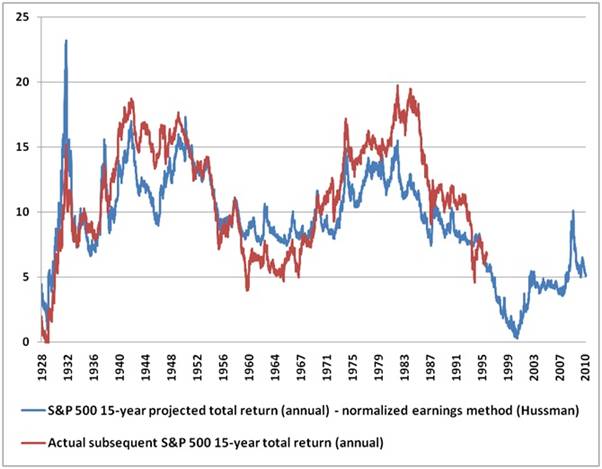

You may notice that unlike the charts we regularly present, which display post-war data, I've included data back to 1928 in the chart above in order to provide as much historical perspective as possible. While the comments below discuss the potential for a further extension of the recent speculative advance, a quick tour of historical market valuations provides some very instructive context. Looking at 1929, it's clear that although the projected 10-year return (blue) for the S&P 500 actually dropped below zero prior to the 1929 crash, the stock market performed even worse than expected over the following decade, with an actual loss of about -5% annually (which compounds to a 10-year total loss of 40%, even including the fairly high dividend yields that were earned following the initial decline). As the stock market plunged following the 1929 peak, the expected 10-year total return spiked higher. Once the S&P 500 had lost half of its value, the projected 10-year total return finally moved above 10% annually. Unfortunately, that was not the end of the decline, but just the beginning. By the time the S&P 500 hit its trough in 1932, it was less than one-third the level it was at the point that the projected total return reached 10%, and was more than 80% off of the 1929 peak. The S&P 500 followed the 1932 bottom with annual returns averaging nearly 14% annually over the following decade, but it would actually take until about 1950 and beyond for the market to fully realize the undervaluation that was present at the 1932 low. By the mid-1960's, stocks were again priced to achieve poor long-term returns. Again, however, the market overshot over the following decade, achieving much poorer returns over the following decade than would have been predicted by valuations alone. Since the losses were excessive on a valuation basis, you'll note that by the mid-1970's, the expected 10-year return for the S&P 500 had increased to more than 16% - a return that was, in fact, achieved despite enormous inflation pressures over the next few years. Now consider the effect of a market bubble. If you skip forward to 1990, you'll see that the actual total return over the following decade was much stronger than one would have anticipated on the basis of valuations at the time. That overshoot of valuation was not retained by investors, however, because it led to a situation where stocks were priced to predicably achieve negative total returns over the decade from 2000 to 2010, which is again precisely what we observed. At the 2009 low, the projected 10-year total return for the S&P 500 briefly spiked above 10%. In the context of economic conditions that had no post-war counterpart, the issue was whether that projected level of return was sufficient to accept a materially invested position in stocks. History had not been kind to that assessment following lesser credit crises, and certainly not during the Depression. But in hindsight, that brief foray above 10% projected returns set the 2009 market low. The subsequent advance in the market has compressed the majority of those prospective 10-year returns into much shorter time frame, leaving little prospect for significant additional returns in the next several years - at least, not additional returns that can be expected to be retained by investors. For a slightly longer-term view, the chart below presents projected 15-year total returns for the S&P 500 Index, again using our standard methodology. At present, we project the 15-year total return for the S&P 500 at about 5% annually.

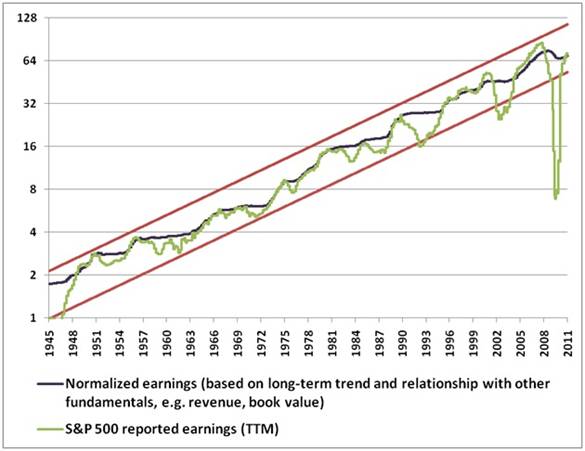

We already know that the negative expecation for 10-year total returns in 2000 turned out to be accurate. Above, you can see that the 15-year projection in 2000 implied roughly zero total returns out to 2015. Notice how this works - a 0% total return over 15 years, given a depressed dividend yield near 2%, implies an annual loss of about -2% on the basis of price alone, which compounds to a roughly 26% overall price loss. We're now 11 years into that 15-year horizon. Given that the S&P 500 peaked above 1550 in 2000, the implied projection for the S&P 500 2015 works out to about 1150. From present levels, that would imply a slightly negative annual loss averaging -2.9% annually. Adding dividends, this works out to the expectation of a slightly negative total return for the S&P 500 over the coming 4 years. While total returns over 4-year horizons tend to be less predictable than over 7-15 year horizons, the overall implication strikes us as just about right. It's not that stocks can't advance, nor that they can't plunge. It's just that the recent advance, in our view, has left stocks with little prospect for durable returns for several years to come. Learning the right lesson So market returns in excess of the growth of smooth fundamentals are simply displaced from the future. For buy-and-hold investors, this fact matters a great deal for the profile of returns they can expect to achieve over time. Buy-and-hold investors faced predictably negative 10-year total returns in 2000, and the prospect of dismal total returns from the 2007 valuation peak. They should certainly revel in their recent returns as measured from the 2009 low, but should also brace for a profile of future long-term returns that has again turned against them to an extent that has historically been distressing. For investors who can vary their market exposure in response to changes in expected returns, the variation in expected returns constantly creates new opportunities over time, some having greater risk than others, but forgiving of risk-management provided that steep losses are avoided. We've outperformed the S&P 500 over every complete market cycle (bull and bear market combined), with smaller periodic losses, since the inception of the Strategic Growth Fund, and we remain ahead of the S&P 500 since its 2007 peak. Still, my concerns about the "out of sample" economic strains of 2009 resulted in a missed opportunity to capture the recovery that followed market losses that we largely avoided. With respect to the present market cycle measured from the 2009 low, it's clear that the some bullish observers would like to call "game over" here while the market is strong. But this isn't how market cycles work. As the song goes, "You don't count your money while you're sittin' at the table." As I've noted before, many speculative factors can drive short-term fluctuations, but they don't change the algebra of long-term returns. A variety of pure trend-following models have performed reasonably well in the window since March 2009. Still, I am convinced that ignoring valuations, economic factors and other evidence in preference for pure trend-following would be the wrong lesson to learn from this period. As I've noted many times, these alternatives are easy to test - if they performed better historically that the methods we use, they would be the methods we use. Likewise, I am suspicious that the proper lesson from 2009 is that we should have ignored everything but post-war data - even though that approach would have been beneficial, in hindsight. In response to the "two data sets" challenge we faced in 2009, we've expanded the set of Market Climates we identify, which better use the evidence from multiple data sets and allow more "shades of grey." Taking a weighted-average of post-war and Depression era implications, as we did in 2009, was inadequate. The ensemble methods that we've implemented allow us to distinguish "risk" (the spread of individual outcomes from the average) from "uncertainty" (the possibility that the average itself is unknown) in a more satisfactory way. So there have certainly been lessons to learn. But it would be a very misguided "lesson" to attempt to correct that missed opportunity in 2009 by suddenly abandoning our long-standing and repeatedly validated practice of avoiding risk in overvalued, overbought, overbullish, rising-interest rate environments, which is what we have at present. That said, I do expect that we'll take on some moderate, periodic exposure to risk before the bull portion of the present cycle is complete - most likely upon clearing some element of the present overvalued, overbought, overbullish, rising-yields syndrome, provided that the market internals remain fairly intact. "Longer than you can stay solvent" Two aphorisms regularly become popular during speculative periods in the market. One is the statement by John Maynard Keynes that "the market can stay irrational longer than you can remain solvent." The other is Warren Buffett's remark that "a pack of lemmings looks like a bunch of individualists compared with Wall Street once it gets a concept in its teeth." It is widely understood that markets can experience extended periods of irrational speculation and valuation bubbles. This becomes problematic when people begin to rely on the irrationality of others as a justification for continuing to speculate, because at that point, they require the assistance of increasingly "greater fools" in order to sustain the advance. Keynes was quite right in the sense that one should never maintain a leveraged position against the market, because leveraged losses certainly do threaten solvency. But investors are not forced to accept risk just because other investors are speculating - there is no great risk in positions that accept no great risk. Moreover, investors cannot safely ignore valuations, because once valuations become rich, the returns from continuing to speculate are not easily retained even if they emerge for a while. If actual returns did not periodically overshoot the returns that are warranted by fundamentals, we would never observe the extended periods of predictably excellent or dismal market returns that have historically corrected those overshoots. Presently, the probable outcome over the coming years leans moderately toward the "dismal" side, but nowhere as negative what we observed in 1929, 2000 or even 2007. We have to be realistic that projected returns were actually driven to negative levels at the peaks of 1929 and 2000, so we can't rule out a further price advance that would compress projected long-term market returns to even lower levels than we observe here. Still, both of those valuation extremes were produced by multi-year periods of rapid, low-volatility economic growth, coupled with the introduction of revolutionary new technologies. A Federal Reserve policy that amounts primarily to rhetoric seems to be an awfully thin substitute at present. Even here, we would expect some opportunity to accept market risk at the point where we clear some component of the present overvalued, overbought, overbullish, rising yields syndrome. So we have the flexibility to deal constructively with yet another bubble if it emerges, but we still expect to hedge against market fluctuations when we observe demonstrably unfavorable sets of market conditions. We face a particularly hostile syndrome now. Normalized earnings, peak-earnings, and discounted cash flows As a reminder of how we approach market valuation, we strongly believe that securities are a claim to a stream of future cash flows that can actually be expected to be delivered to investors over time. As a result, we have little sympathy (and history demonstrates little sympathy) for the popular but misguided practice of applying arbitrary valuation multiples to forward analyst estimates of earnings. Generally, these "forward earnings" estimates fail to normalize for fluctuations in profit margins, return on equity, and other factors that have historically driven short-term earnings temporarily above and below levels that that would have a stable, proportional relationship with the present value of subsequent cash flows. Forward operating earnings estimates are more volatile and more influenced by recent short-term behavior than can properly be used as a basis for valuation, and the resulting earnings "misses" can be particularly extreme at turning points. In the graph below, you'll notice that the prior peak for S&P 500 trailing net earnings has often been a reasonable "rule of thumb" estimate of normalized earnings, but in recent years, temporary spikes in profit margins have periodically driven peak earnings briefly above properly normalized levels. For that reason, as I wrote several years ago, prior peak earnings have become increasingly unreliable. This is particularly true given the actual destruction of book value and revenue in recent years. It's certainly possible to debate the precise level of normalized earnings here, but somewhere in the $70-$75 range, which is where we are at present, is roughly accurate on a trailing net basis. Our estimates also assume continued future long-term growth of slightly more than 6% annually, as reflected by the red channels.

Importantly, since our normalized figure tends to run with earnings peaks rather than earnings troughs, the corresponding multiple applicable to these earnings has historically been less than 14 (and was actually closer to 12 in pre-bubble data, which was typically associated with long-term total returns near 10% annually). Since "forward operating" earnings are typically about 20% higher than trailing net, the resulting historical P/E "norms" should also be adjusted accordingly (which analysts rarely do). None of this is to say that the earnings peak during the current economic cycle has to be limited to the present level of normalized earnings - just that more elevated earnings would not be an appropriate basis on which to compute the long-term value of stocks. Market Climate As of last week, the Market Climate for stocks remained characterized by an overvalued, overbought, overbullish, rising-yields syndrome that has historically been hostile for the market, but is often accompanied by an "unpleasant skew" in that there is a high probability of persistent small advances to marginal new highs, which are generally resolved by abrupt vertical declines that can wipe out weeks or months of upside progress in a few sessions. Long-term readers of these comments have observed several times how these tend to resolve. Frankly, we never know exactly what the news will be that resolves them. Back in 1987, the "news" was actually just a bad trade balance number - so traders would nervously run for cover for months whenever a trade number was about to be released. In 1998 the Asian crisis provided a more substantial news item, but the plunge was not as extreme as 1987, and certainly nowhere near the larger adjustment that occurred beginning in 2000. That means that we have to take our evidence as it comes. If we can remove some component of that syndrome, without incurring clear internal damage (which would probably require something around the 1120 - 1140 level on the S&P 500), we will have the latitude to accept a moderate exposure to market fluctuations on a portion of our holdings, while retaining a line of put defense around the low-to-mid 1100's as a safety net against a sharp deterioration in prices and market internals. Presently, both Strategic Growth and Strategic International Equity are fully hedged. We can expect to perform best when we've got both engines firing - one being stock selection, the other being the ability to accept market fluctuations at a favorable return/risk tradeoff. Despite temporary periods where low-quality, speculative stocks dominate, and overvalued, overbought, overbullish, rising-yields conditions persist uncorrected, we expect good opportunities to fire on both. In bonds, the Market Climate deteriorated slightly last week, as we observed some slight additional yield pressures at the short end. As I'll detail more extensively in a few weeks, monetary policy is operating quite close to its limits, because extaordinarily low short-term interest rates are required to avoid inflationary pressures given the size of the Fed's balance sheet. Even an uptick of 15-25 basis points in Treasury bill yields would provoke either inflationary pressures or the need to contract the monetary base through a reversal of the Fed's Treasury and possibly even GSE debt purchases. I don't anticipate such pressures in the near term, and continue to expect inflation pressures to be deferred, but it's a situation we're monitoring. Strategic Total Return continues to carry a duration of less than 2 years. In precious metals, the Market Climate actually tends to be best when Treasury yields are in a declining trend and economic measures are weak. Still, we've seen some clear price weakness in the past several weeks, and on the basis of valuation and other factors, we would expect to modestly (not aggressively) accumulate precious metals shares on further weakness. In honor and remembrance of Dr. Martin Luther King, Jr. Dr. King noted that he tried to speak on the subject below at least once a year, so although I've reprinted this text in previous years, it still seems an appropriate way to honor him. If you've never read Dr. King's writings, this talk is a good place to start. Loving Your Enemies "I want to use as a subject from which to preach this morning a very familiar subject, and it is familiar to you because I have preached from this subject twice before to my knowing in this pulpit. I try to make it a, something of a custom or tradition to preach from this passage of Scripture at least once a year, adding new insights that I develop along the way out of new experiences as I give these messages. Although the content is, the basic content is the same, new insights and new experiences naturally make for new illustrations. "So I want to turn your attention to this subject: "Loving Your Enemies." It's so basic to me because it is a part of my basic philosophical and theological orientation—the whole idea of love, the whole philosophy of love. In the fifth chapter of the gospel as recorded by Saint Matthew, we read these very arresting words flowing from the lips of our Lord and Master: "Ye have heard that it has been said, 'Thou shall love thy neighbor, and hate thine enemy.' But I say unto you, Love your enemies, bless them that curse you, do good to them that hate you, and pray for them that despitefully use you; that ye may be the children of your Father which is in heaven." "Over the centuries, many persons have argued that this is an extremely difficult command. Many would go so far as to say that it just isn't possible to move out into the actual practice of this glorious command. But far from being an impractical idealist, Jesus has become the practical realist. The words of this text glitter in our eyes with a new urgency. Far from being the pious injunction of a utopian dreamer, this command is an absolute necessity for the survival of our civilization. Yes, it is love that will save our world and our civilization, love even for enemies. "Now let me hasten to say that Jesus was very serious when he gave this command; he wasn't playing. He realized that it's hard to love your enemies. He realized that it's difficult to love those persons who seek to defeat you, those persons who say evil things about you. He realized that it was painfully hard, pressingly hard. But he wasn't playing. We have the Christian and moral responsibility to seek to discover the meaning of these words, and to discover how we can live out this command, and why we should live by this command. "Now first let us deal with this question, which is the practical question: How do you go about loving your enemies? I think the first thing is this: In order to love your enemies, you must begin by analyzing self. And I'm sure that seems strange to you, that I start out telling you this morning that you love your enemies by beginning with a look at self. It seems to me that that is the first and foremost way to come to an adequate discovery to the how of this situation. "Now, I'm aware of the fact that some people will not like you, not because of something you have done to them, but they just won't like you. But after looking at these things and admitting these things, we must face the fact that an individual might dislike us because of something that we've done deep down in the past, some personality attribute that we possess, something that we've done deep down in the past and we've forgotten about it; but it was that something that aroused the hate response within the individual. That is why I say, begin with yourself. There might be something within you that arouses the tragic hate response in the other individual. "This is true in our international struggle. Democracy is the greatest form of government to my mind that man has ever conceived, but the weakness is that we have never touched it. We must face the fact that the rhythmic beat of the deep rumblings of discontent from Asia and Africa is at bottom a revolt against the imperialism and colonialism perpetuated by Western civilization all these many years. "And this is what Jesus means when he said: "How is it that you can see the mote in your brother's eye and not see the beam in your own eye?" And this is one of the tragedies of human nature. So we begin to love our enemies and love those persons that hate us whether in collective life or individual life by looking at ourselves. "A second thing that an individual must do in seeking to love his enemy is to discover the element of good in his enemy, and every time you begin to hate that person and think of hating that person, realize that there is some good there and look at those good points which will over-balance the bad points. "Somehow the "isness" of our present nature is out of harmony with the eternal "oughtness" that forever confronts us. And this simply means this: That within the best of us, there is some evil, and within the worst of us, there is some good. When we come to see this, we take a different attitude toward individuals. The person who hates you most has some good in him; even the nation that hates you most has some good in it; even the race that hates you most has some good in it. And when you come to the point that you look in the face of every man and see deep down within him what religion calls "the image of God," you begin to love him in spite of. No matter what he does, you see God's image there. There is an element of goodness that he can never slough off. Discover the element of good in your enemy. And as you seek to hate him, find the center of goodness and place your attention there and you will take a new attitude. "Another way that you love your enemy is this: When the opportunity presents itself for you to defeat your enemy, that is the time which you must not do it. There will come a time, in many instances, when the person who hates you most, the person who has misused you most, the person who has gossiped about you most, the person who has spread false rumors about you most, there will come a time when you will have an opportunity to defeat that person. It might be in terms of a recommendation for a job; it might be in terms of helping that person to make some move in life. That's the time you must do it. That is the meaning of love. In the final analysis, love is not this sentimental something that we talk about. It's not merely an emotional something. Love is creative, understanding goodwill for all men. It is the refusal to defeat any individual. When you rise to the level of love, of its great beauty and power, you seek only to defeat evil systems. Individuals who happen to be caught up in that system, you love, but you seek to defeat the system. "The Greek language, as I've said so often before, is very powerful at this point. It comes to our aid beautifully in giving us the real meaning and depth of the whole philosophy of love. And I think it is quite apropos at this point, for you see the Greek language has three words for love, interestingly enough. It talks about love as eros. That's one word for love. Eros is a sort of, aesthetic love. Plato talks about it a great deal in his dialogues, a sort of yearning of the soul for the realm of the gods. And it's come to us to be a sort of romantic love, though it's a beautiful love. Everybody has experienced eros in all of its beauty when you find some individual that is attractive to you and that you pour out all of your like and your love on that individual. That is eros, you see, and it's a powerful, beautiful love that is given to us through all of the beauty of literature; we read about it. "Then the Greek language talks about philia, and that's another type of love that's also beautiful. It is a sort of intimate affection between personal friends. And this is the type of love that you have for those persons that you're friendly with, your intimate friends, or people that you call on the telephone and you go by to have dinner with, and your roommate in college and that type of thing. It's a sort of reciprocal love. On this level, you like a person because that person likes you. You love on this level, because you are loved. You love on this level, because there's something about the person you love that is likeable to you. This too is a beautiful love. You can communicate with a person; you have certain things in common; you like to do things together. This is philia. "The Greek language comes out with another word for love. It is the word agape. And agape is more than eros; agape is more than philia; agape is something of the understanding, creative, redemptive goodwill for all men. It is a love that seeks nothing in return. It is an overflowing love; it's what theologians would call the love of God working in the lives of men. And when you rise to love on this level, you begin to love men, not because they are likeable, but because God loves them. You look at every man, and you love him because you know God loves him. And he might be the worst person you've ever seen. "And this is what Jesus means, I think, in this very passage when he says, "Love your enemy." And it's significant that he does not say, "Like your enemy." Like is a sentimental something, an affectionate something. There are a lot of people that I find it difficult to like. I don't like what they do to me. I don't like what they say about me and other people. I don't like their attitudes. I don't like some of the things they're doing. I don't like them. But Jesus says love them. And love is greater than like. Love is understanding, redemptive goodwill for all men, so that you love everybody, because God loves them. You refuse to do anything that will defeat an individual, because you have agape in your soul. And here you come to the point that you love the individual who does the evil deed, while hating the deed that the person does. This is what Jesus means when he says, "Love your enemy." This is the way to do it. When the opportunity presents itself when you can defeat your enemy, you must not do it. "Now for the few moments left, let us move from the practical how to the theoretical why. It's not only necessary to know how to go about loving your enemies, but also to go down into the question of why we should love our enemies. I think the first reason that we should love our enemies, and I think this was at the very center of Jesus' thinking, is this: that hate for hate only intensifies the existence of hate and evil in the universe. If I hit you and you hit me and I hit you back and you hit me back and go on, you see, that goes on ad infinitum. It just never ends. Somewhere somebody must have a little sense, and that's the strong person. The strong person is the person who can cut off the chain of hate, the chain of evil. And that is the tragedy of hate - that it doesn't cut it off. It only intensifies the existence of hate and evil in the universe. Somebody must have religion enough and morality enough to cut it off and inject within the very structure of the universe that strong and powerful element of love. "I think I mentioned before that sometime ago my brother and I were driving one evening to Chattanooga, Tennessee, from Atlanta. He was driving the car. And for some reason the drivers were very discourteous that night. They didn't dim their lights; hardly any driver that passed by dimmed his lights. And I remember very vividly, my brother A. D. looked over and in a tone of anger said: "I know what I'm going to do. The next car that comes along here and refuses to dim the lights, I'm going to fail to dim mine and pour them on in all of their power." And I looked at him right quick and said: "Oh no, don't do that. There'd be too much light on this highway, and it will end up in mutual destruction for all. Somebody got to have some sense on this highway." "Somebody must have sense enough to dim the lights, and that is the trouble, isn't it? That as all of the civilizations of the world move up the highway of history, so many civilizations, having looked at other civilizations that refused to dim the lights, and they decided to refuse to dim theirs. And Toynbee tells that out of the twenty-two civilizations that have risen up, all but about seven have found themselves in the junk heap of destruction. It is because civilizations fail to have sense enough to dim the lights. And if somebody doesn't have sense enough to turn on the dim and beautiful and powerful lights of love in this world, the whole of our civilization will be plunged into the abyss of destruction. And we will all end up destroyed because nobody had any sense on the highway of history. "Somewhere somebody must have some sense. Men must see that force begets force, hate begets hate, toughness begets toughness. And it is all a descending spiral, ultimately ending in destruction for all and everybody. Somebody must have sense enough and morality enough to cut off the chain of hate and the chain of evil in the universe. And you do that by love. "There's another reason why you should love your enemies, and that is because hate distorts the personality of the hater. We usually think of what hate does for the individual hated or the individuals hated or the groups hated. But it is even more tragic, it is even more ruinous and injurious to the individual who hates. You just begin hating somebody, and you will begin to do irrational things. You can't see straight when you hate. You can't walk straight when you hate. You can't stand upright. Your vision is distorted. There is nothing more tragic than to see an individual whose heart is filled with hate. He comes to the point that he becomes a pathological case. For the person who hates, you can stand up and see a person and that person can be beautiful, and you will call them ugly. For the person who hates, the beautiful becomes ugly and the ugly becomes beautiful. For the person who hates, the good becomes bad and the bad becomes good. For the person who hates, the true becomes false and the false becomes true. That's what hate does. You can't see right. The symbol of objectivity is lost. Hate destroys the very structure of the personality of the hater. "The way to be integrated with yourself is be sure that you meet every situation of life with an abounding love. Never hate, because it ends up in tragic, neurotic responses. Psychologists and psychiatrists are telling us today that the more we hate, the more we develop guilt feelings and we begin to subconsciously repress or consciously suppress certain emotions, and they all stack up in our subconscious selves and make for tragic, neurotic responses. And may this not be the neuroses of many individuals as they confront life that that is an element of hate there. And modern psychology is calling on us now to love. But long before modern psychology came into being, the world's greatest psychologist who walked around the hills of Galilee told us to love. He looked at men and said: "Love your enemies; don't hate anybody." It's not enough for us to hate your friends because—to to love your friends—because when you start hating anybody, it destroys the very center of your creative response to life and the universe; so love everybody. Hate at any point is a cancer that gnaws away at the very vital center of your life and your existence. It is like eroding acid that eats away the best and the objective center of your life. So Jesus says love, because hate destroys the hater as well as the hated. "Now there is a final reason I think that Jesus says, "Love your enemies." It is this: that love has within it a redemptive power. And there is a power there that eventually transforms individuals. That's why Jesus says, "Love your enemies." Because if you hate your enemies, you have no way to redeem and to transform your enemies. But if you love your enemies, you will discover that at the very root of love is the power of redemption. You just keep loving people and keep loving them, even though they're mistreating you. Here's the person who is a neighbor, and this person is doing something wrong to you and all of that. Just keep being friendly to that person. Keep loving them. Don't do anything to embarrass them. Just keep loving them, and they can't stand it too long. Oh, they react in many ways in the beginning. They react with bitterness because they're mad because you love them like that. They react with guilt feelings, and sometimes they'll hate you a little more at that transition period, but just keep loving them. And by the power of your love they will break down under the load. That's love, you see. It is redemptive, and this is why Jesus says love. There's something about love that builds up and is creative. There is something about hate that tears down and is destructive. So love your enemies. "There is a power in love that our world has not discovered yet. Jesus discovered it centuries ago. Mahatma Gandhi of India discovered it a few years ago, but most men and most women never discover it. For they believe in hitting for hitting; they believe in an eye for an eye and a tooth for a tooth; they believe in hating for hating; but Jesus comes to us and says, "This isn't the way." "As we look out across the years and across the generations, let us develop and move right here. We must discover the power of love, the power, the redemptive power of love. And when we discover that we will be able to make of this old world a new world. We will be able to make men better. Love is the only way. Jesus discovered that. "And our civilization must discover that. Individuals must discover that as they deal with other individuals. There is a little tree planted on a little hill and on that tree hangs the most influential character that ever came in this world. But never feel that that tree is a meaningless drama that took place on the stages of history. Oh no, it is a telescope through which we look out into the long vista of eternity, and see the love of God breaking forth into time. It is an eternal reminder to a power-drunk generation that love is the only way. It is an eternal reminder to a generation depending on nuclear and atomic energy, a generation depending on physical violence, that love is the only creative, redemptive, transforming power in the universe. "So this morning, as I look into your eyes, and into the eyes of all of my brothers in Alabama and all over America and over the world, I say to you, "I love you. I would rather die than hate you." And I'm foolish enough to believe that through the power of this love somewhere, men of the most recalcitrant bent will be transformed. And then we will be in God's kingdom." --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |