|

|

||||||

|

|

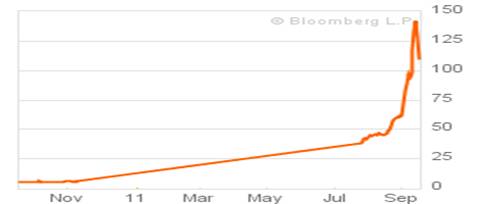

September 19, 2011 Preparing for a Greek Default The yield on 1-year Greek government debt ended last week at 110%, down slightly from a mid-week peak of 130%. Even with the pullback, the Greek yield structure continues to imply default with certainty. All the markets are really quibbling about here is the recovery rate - what percentage of face value investors can expect to obtain post-default. That figure was still hovering near 50% as of Friday, but was a bit higher than we saw a few days earlier. Despite a Greek 1-year yield that is already over 100%, it is still possible to kick the can down the road for another few months with another bailout, but the costs of that would now be extraordinarily high because of the low expected recovery rate. Much better to provide the funds to a post-default Greece, or to use them to recapitalize the banking system after losses that now appear inevitable. Doureios Ippos: Greek 1-year yields

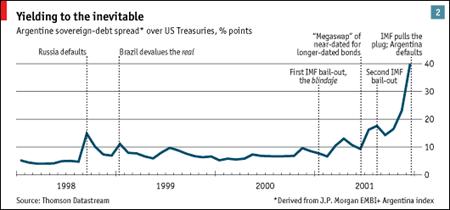

As a refresher on how all of this works, the following chart appeared years ago in the Economist, a chronicle of the frantic bail-outs in the months preceding the default of Argentine debt (which amounted to about $81 billion. Needless to say, the numbers involved in a potential Greek default are much larger, but the pattern we are seeing in Greece is identical to the signature of other historical sovereign defaults (see Uruguay, Russia and other countries as well ) - a sustained rise in yields, coupled with official statements about the "impossibility" of default, multiple bailout efforts that quickly fail, culminating in a vertical spike in yields (toward the inverse of the expected recovery rate, minus 1).

The case of Argentina is instructive because it was in a situation much like that of Greece. Argentina's currency was both pegged and officially convertible into the U.S. dollar, and most of Argentina's debt was denominated in U.S. dollars, creating a situation where its debt burden was in the form of a currency that it effectively could not print. The subsequent default was accompanied first by an abrupt devaluation of the peso to a new peg, and eventually to complete abandonment of the pegged exchange rate. From the history of sovereign defaults, we can already create something of a roadmap of the financial crisis that appears about to unfold, and the associated choices involved. Suppose first that Greece agrees to implement new austerity measures and receives another tranche of bailout funding. We already know that applying severe budget austerity in an economy that is in depression (as Greece essentially is) does not materially close the budget deficit, but instead produces further economic weakness and revenue shortfalls. The past year has been a clear example of that. By the end of the year, even with new bailout funding, Greece will have a debt-to-GDP ratio approaching 180%. This is an impossible debt burden to service, and would be even if interest rates in Greece were only a few percent. New bailout funding here means that we'll observe more rioting in Greece as new austerity measures are implemented, the Greek economy will largely shut down, and within a few months, we'll be facing the default issue again but at an even higher debt-to-GDP level and even lower anticipated recovery rates. Thus, a bailout today does not avert default, but at best defers it to a later date, and squanders funds that could otherwise be used to stabilize the European banking system once that inevitable default occurs. Of course, there is the implausible option for stronger countries such as France and Germany to literally pay off half of the government debt of Greece, taking those debt burdens upon themselves. But this clearly would not be tolerable politically, and would invite similar expectations from other teetering Euro-zone countries such as Portugal, undoubtedly also encouraging them to completely abandon any remaining fiscal discipline. So Greece will default, either now or within several months. In response, three actions will be critical: preventing contagion, preserving the euro, and stabilizing the banking system. First, and most immediately, European leaders will have to prevent contagion. As I noted two weeks ago, Italy and Spain are the most worrisome targets of contagion, but even though they are large and have high debt-to-GDP ratios, there is no credible risk of default in these countries in the foreseeable future. So the ECB should absolutely be willing to extend its purchases of Spanish and Italian debt. Even the U.S. Federal Reserve, which is authorized to purchase foreign government debt under Section 14 of the Federal Reserve Act could provide significant stability by initiating even modest purchases of Spanish and Italian obligations (purchasing Greek debt, on the other hand, would wander unconstitutionally into fiscal policy, since the likelihood of default is so high). The key to stopping a contagion is to delineate which countries absolutely belong behind the firewall, rather than behaving as if all of them do. As for the euro, the best chance for a durable currency is to restrict its membership to countries with similar macroeconomic characteristics that are actually capable of following a very uniform budget discipline. Neither a single central fiscal authority for all of Europe, nor the issuance of "Euro-bonds," are useful ways of achieving this goal. There is too much economic heterogeneity and too much cultural individuality in Europe for all of these countries to surrender their fiscal policy independence away from their own citizens. Meanwhile, "Euro-bonds" would represent an effective subsidy and guarantee from more stable European countries to less stable ones, and would encourage moral hazard and fiscal recklessness the likes of which the developed world has never seen. Ultimately, the only way to preserve the euro is to remove its fiscally unstable members from the formal currency arrangement. Peripheral European countries could potentially substitute that with a pegged exchange rate. Of course, even a pegged exchange rate can lead to a currency crisis if fiscal discipline is weak enough, as we saw a decade ago with Argentina. Still, it would be far better for countries such as Greece and Portugal to redenominate into their own currencies, and peg them to the euro, than to bring down a system that works very well for the majority of European citizens. The third policy response, of course, would be to stabilize the banking system. My own view has always been straightforward - investors and institutions that voluntarily accept risk in order to reach for extra yield should be prepared to suffer the losses if those investments fail. Nearly every major financial institution has enough shareholder capital and debt to its own bondholders to absorb losses without any loss to customers or counterparties. Financial institutions that become insolvent as a result of bad investments should be taken into receivership and recapitalized under new ownership - with the existing shareholders wiped out, and the existing bondholders receiving the residual (which in most cases is 100 cents on the dollar for senior debt anyway, and often close to that even for subordinate debt). In any event, however, whatever public funds Europe wishes to use in order to address this crisis should be directed to replenishing the capital of banks (ideally, restructured ones), and providing emergency capital to a post-default Greece. This is in Europe's best interests, and it is in Greece's best interests, because however longingly policy makers would like to imagine that further bailouts can prevent a Greek default at its current level of debt-to-GDP, the arithmetic simply does not work that way. The time for changes to fiscal policy was years ago, well before the Greek debt-to-GDP level scaled its current heights. Europe will now have to play the hand that has been dealt. So, unfortunately, will the United States. According to Fitch Ratings, the ten largest U.S. prime money market funds had total assets of $658 billion as of July 31, 2011. Of those assets, $309 billion - an unsettling 47% of the total - represented debt obligations issued by European banks. It is unclear what level of subordination these debt obligations take, but we can expect that in the event of a Greek default, this concentrated ownership of European bank debt by U.S. money market funds will be less than ideal for investor confidence. (As a side note, the money market assets held by the Hussman Funds are in U.S. Treasury funds.) I can't imagine what the yield-reaching managers holding European bank debt are thinking, but if last week's agreement by the Fed to provide dollar swaps to the ECB is any indication, my guess is that the eagerness to send dollar liquidity to Europe is abruptly drying up from private sources. In any case, the heavy allocation of U.S. savings to the European banking system strikes me as an awful example of "moral hazard" produced by two forces: the 2008-2009 bank bailouts, coupled with a European regulatory structure that doesn't require those banks to hold any capital against holdings of European government debt, including that of Greece. As we saw in the housing crisis, when a weak regulatory structure encourages unaccountable leverage, and irresponsible monetary policies encourage reaching for yield, the combined result is predictably disastrous. Market Climate As of last week, the Market Climate in stocks remained hard negative on the basis of a broad ensemble of evidence, including valuations, market action, economic pressures, and other factors. Growing bearish sentiment slightly mitigates the negatives, but the overall return/risk profile remains quite unfavorable on our measures. The Fed seems likely to initiate an "Operation Twist" later this week - extending the maturity of its holdings by substituting short-term Treasury holdings with longer-term notes. But with 10-year Treasuries already below 2% and mortgage rates at record lows, the purpose of that sort of operation is entirely obscure. Despite a long historical record showing no measurable "wealth effect" linking stock market fluctuations to GDP in practice, at least QE2 benefited from Bernanke's argument that it might work in theory. In contrast, it is difficult to imagine what benefit a Twist operation might have even in theory. Certainly, we should not expect any change in the volume of lending. A further slight reduction in long-term interest rates would relieve no binding economic constraints, and has little chance of reversing what now appears to be near-certainty of oncoming recession. Nor will Operation Twist "create wealth." Think about this for a moment. Treasury securities represent a fixed stream of future payments. Changing the price doesn't increase aggregate wealth. The buyer and seller simply exchange current purchasing power for future purchasing power, but no additional output is created. The transaction simply changes who consumes now and who consumes later. Moreover, at sub-2% yields going in, it will be challenging for the Fed to reverse these transactions except at lower prices and higher yields. Regardless, we'll take our cues from the data. If sentiment remains restrained, there are some conditions - largely related to improved market action - that could move us to a modestly constructive investment stance despite unfavorable economic evidence and rich valuations. At present, we don't observe that evidence, and I am much more concerned about abrupt market losses than about the possibility for significant market strength. But again, we'll move as the data moves, and we remain open to establishing at least a moderate exposure to market fluctuations at any point that the expected return/risk profile of the market peeks above negative levels. For now, Strategic Growth and Strategic International Equity remain tightly hedged. Strategic Total Return continues to carry a duration of about 1.5 years, with about 20% of assets in precious metals shares, about 4% of assets in utility shares, and about 2% of assets in non-euro foreign currencies. My own view is that a departure of Greece and other peripheral nations from the euro, far from destroying it, would make the European currency stronger and far more attractive, but as always, we'll take our evidence as it comes and set our investment positions accordingly. * Do not trust the horse, Trojans! Whatever it is, I fear the Danaans, even when bearing gifts. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |