|

|

||||||

|

|

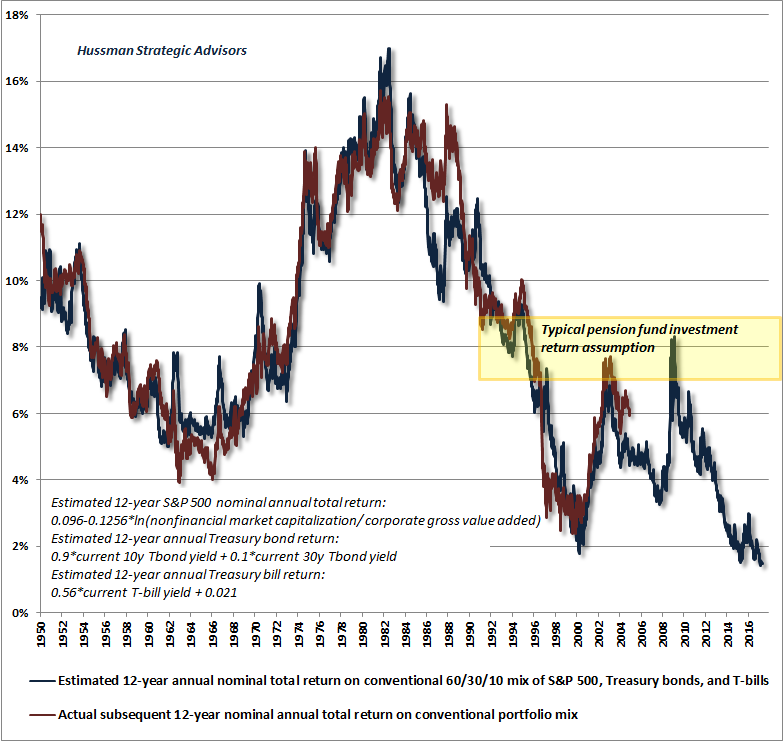

April 3, 2017 Stalling Engines: The Outlook for U.S. Economic Growth Imagine driving a car moving down the road at 20 miles an hour. You hold a rope out the window. At the other end of that rope is a skateboard. If the skateboard is behind the car, yanking the rope pulls the skateboard forward, so the skateboard might temporarily speed ahead until it gets way ahead of the car and the rope tightens again. At that point, yanking the rope will pull the skateboard back, so even while the car continues down the road at 20 miles an hour, the skateboard actually loses ground for a while. Over the long-term, the car and the skateboard move ahead at the same speed, but the speed of the skateboard over shorter horizons depends on its position relative to the underlying trend. The same proposition applies to the trajectory of numerous economic and financial variables. We have to be attentive to at least two things: 1) the central tendency of growth in underlying fundamentals, and 2) our current position, relative to that central tendency. The difference between the two is what separates longer-term growth from cyclical fluctuations. I’ve detailed this dynamic extensively in the financial markets. Given present valuation extremes, the skateboard is so far ahead of the car that we expect S&P 500 annual nominal total returns to average just 0.6% over the coming 12-year period, even if underlying economic growth accelerates to historically normal rates. Combine that with depressed interest rates, where poor 10-12 year total returns are baked-in-the-cake, and our estimate of the prospective total return on a conventional portfolio mix of 60% stocks, 30% bonds, and 10% T-bills has never been lower. The chart below presents our estimates for these returns, along with the subsequent total returns (red line) that investors actually realized over the following 12-year period. Given that typical pension fund return assumptions are vastly above our current estimates, it follows that we expect a rather severe pension funding crisis in the coming years. If the resolution of the present valuation extremes is anything like what has followed other speculative peaks like 2000 and 2007, investors will likely face a substantially different (and better) menu of investment opportunities within a small number of years. Dry powder has considerable option value.

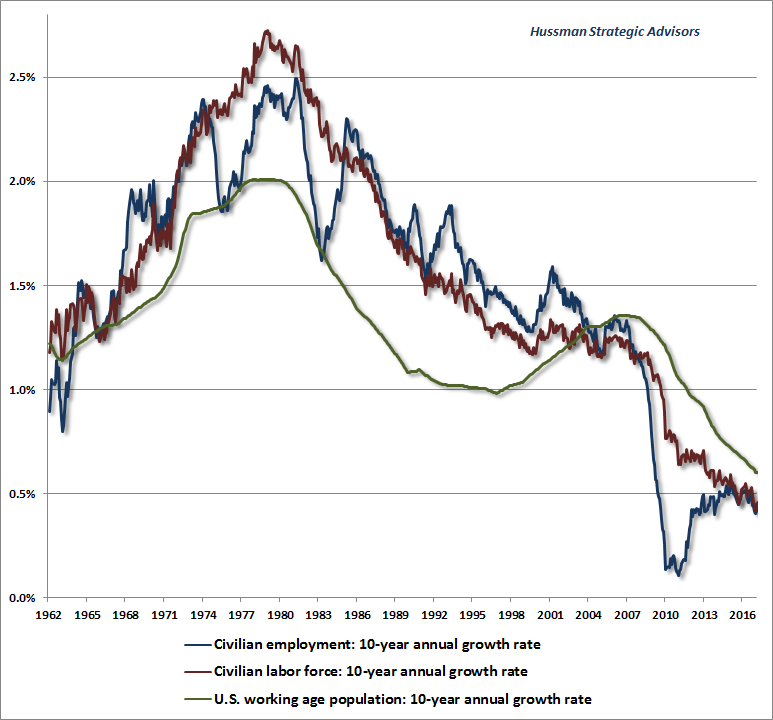

Moving beyond the financial markets, we turn to the prospects for growth in the U.S. economy itself. We’ll begin first with the 7-10 year horizon, and then focus our attention on cyclical risks. The two engines of economic growth Real U.S. GDP growth is driven by two engines: the growth rate of the labor force, plus the growth rate of output per worker (productivity). On the labor side, the U.S Bureau of Labor Statistics (BLS) projects that the U.S. labor force - the number of people working or looking for work - will reach 163.8 million in 2024. As of February 2017, the U.S. labor force stood at 160.1 million. Accordingly, the growth rate of the U.S. labor force is projected to average just 0.3% annually over the coming 7 years. To illustrate what’s going on, the chart below shows the 10-year growth rates of the U.S. working age population, the civilian labor force, and civilian employment since the 1960’s. It’s clear from this chart that the central tendency of the “labor force” contribution to U.S. GDP growth has been steadily declining, having peaked in the 1970s and early 1980s. As the BLS explains, “During the 1970s and 1980s, the labor force grew vigorously as women’s labor force participation rates surged and the baby-boom generation entered the labor market. However, the dynamic demographic, economic, and social forces that once spurred the level, growth, and composition of the labor force have changed and are now damping labor force growth. The labor force participation rate of women, which peaked in 1999, has been on a declining trend. In addition, instead of entering the labor force, baby boomers are retiring in large numbers and exiting the workforce. Once again, the baby-boom generation has become a generator of change, this time in its retirement.”

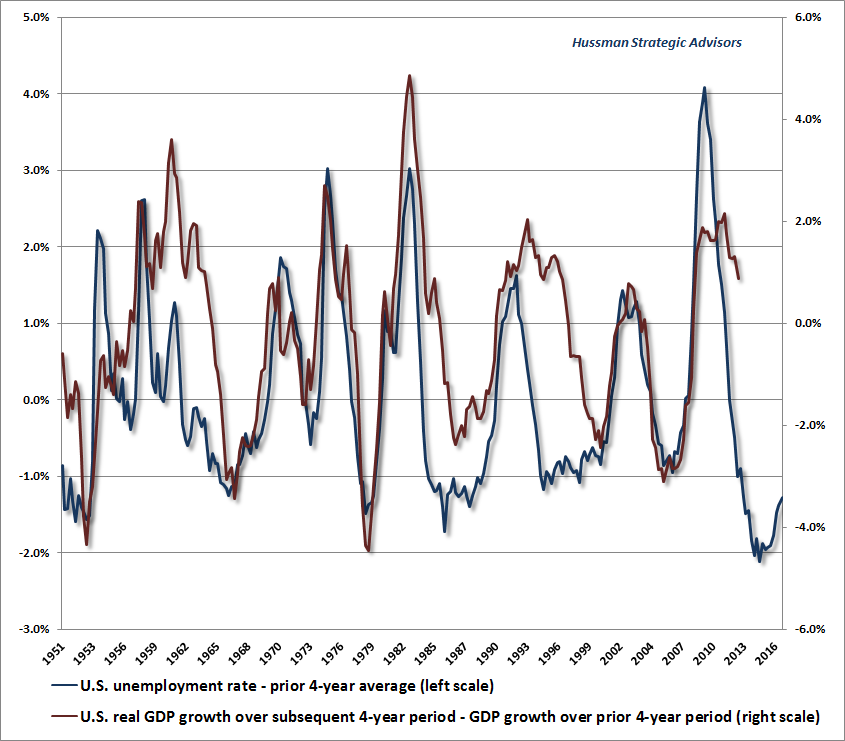

On the productivity front, as I noted in Economic Fancies and Basic Arithmetic, “Over the past decade, productivity growth has declined from a post-war average of 2% to a growth rate of just 1% annually, with growth of just 0.5% annually over the past 5 years. The gap between dismal productivity and the most productive economic environment in U.S. history is only about 2.5% annually.” Presently, the Federal Reserve estimates the central tendency of long-run real GDP growth to average just 1.85% annually. Understand that even a 1.85% average economic growth rate in the coming years already builds in some optimistic assumptions. See, even if U.S labor force growth grows at the projected rate of 0.3% annually, this growth will transfer to a similar rate of employment growth only if the unemployment rate remains constant at the current 4.7% level. Meanwhile, with labor productivity growing at only about 0.5% annually, well below the post-war average of 2%, the baseline expectation for U.S. GDP growth, given no change in the present trajectory, is actually just 0.3% + 0.5% = 0.8%. So a 1.85% growth trajectory for real GDP assumes that some combination of labor force growth and productivity growth will accelerate from the current baseline. Stalling engines While I share the optimism that the central tendency of U.S. real GDP growth will average close to 2% annually over the coming decade (largely based on expectations for somewhat faster productivity growth), it’s important to distinguish this average trend from the cyclical growth rates that we’re likely to observe over shorter horizons. On that front, my expectation is that the U.S. is facing the prospect of sustained slowing or outright contraction of economic activity over the next several years. There is certainly great hope across Wall Street that the policy changes being proposed by 45 will improve the economic outlook. Unfortunately, this hope overlooks the challenging arithmetic that is already baked-in-the-cake here. Moreover, as detailed below, the policies being discussed - particularly as they affect immigration and trade - are likely to materially worsen this arithmetic. Recall the car and the skateboard. When the skateboard lags way behind, there is a great deal of room available to pull ahead, allowing a temporary acceleration where a great deal of forward progress can be made over a short period of time. Conversely, once the skateboard has moved ahead for a sustained period of time, the likelihood of continued forward progress becomes smaller, and even a slight backward tug can erase all momentum and send the skateboard backwards. 1) Labor force growth Periods of rapid and sustained economic growth invariably begin from points of steep unemployment, because that’s the point from which the economy can enjoy a great deal of growth in the “labor force” contribution to growth. We hear a lot of hope that corporate tax cuts will prompt the kind of growth the U.S. enjoyed following the tax reforms of the 1950’s and the 1980’s. What’s often lost in this conversation is that the principal engines of economic expansion were already loaded with fuel at those points, mainly in the form of rapid underlying labor force growth and slack labor market capacity. That is not at all true today. The chart below shows the unemployment rate relative to its trailing 4-year average, along with subsequent 4-year growth in real GDP in excess of its trailing 4-year average. Note that significant accelerations in real GDP growth, not surprisingly, originate at points where unemployment has surged relative to previous years. That was true even coming out of the global financial crisis. But even the relatively tepid economic growth of recent years has taken up that slack capacity, because it has been sustained longer than most prior expansions. Combine the low underlying growth of the labor force with limited amount of remaining slack, and it’s clear that one of the two engines of economic growth is set to sputter for a while. As a side note, the combination of slowing economic growth and tightening labor market constraints is likely to widen the wage share of GDP, while narrowing corporate profit margins by a greater amount than tax cuts are likely to relieve.

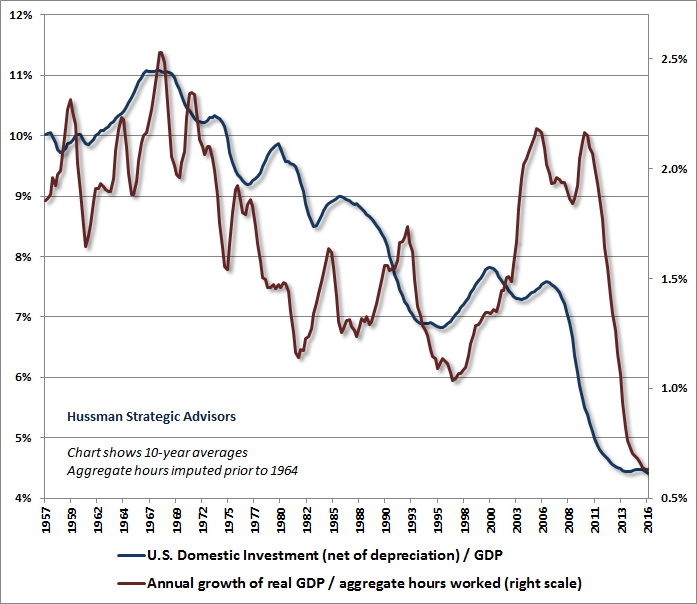

Employment, population, and unemployment figures relate to each other like this: the current labor force represents 63% of the U.S. working age population. That participation rate is below the record high of 67% at the peak of the 2000 economic cycle, but several percent above the post-war norm prior to 1980. Civilian employment currently stands at 152.5 million, representing 95.3% of the labor force. The unemployment rate captures the remaining 4.7% of the labor force. Even the “U6” unemployment rate is within 2.6% of its lowest level in history. Most of the difference between the U6 and the traditional unemployment rate represents workers who are “employed part-time for economic reasons.” That is, they already have a job, but they would prefer to have full-time rather than part-time work. Doing so would increase aggregate hours worked, but it wouldn’t raise total employment. So let’s be clear about the prospects for U.S. employment growth. Suppose that contrary to demographic projections, U.S. labor force participation was to surge back to the highest level in history, coupled with a continued drop in the unemployment rate to just 4% by 2024. Even in this wildly best-case scenario, the growth rate of U.S. employment would average just 1.3% over the coming 7-year period, a rate that would still be below the post-war average of 1.7% prior to 2000. 2) Productivity Since 1950, the central tendency of U.S. productivity growth has averaged slightly more than 2% annually, falling to half that rate over the past decade, and close to 0.5% in recent years. Over the long-term, the growth of U.S. productivity is largely driven by the growth of U.S. domestic investment, particularly net of depreciation. As technology increases the speed of obsolescence, depreciation rates have progressively increased in recent decades, so a given amount of gross domestic investment does progressively less to expand the U.S. capital stock. The chart below shows the 10-year averages of U.S. domestic investment (net of depreciation) as a share of GDP, along with the growth rate of real output per labor hour.

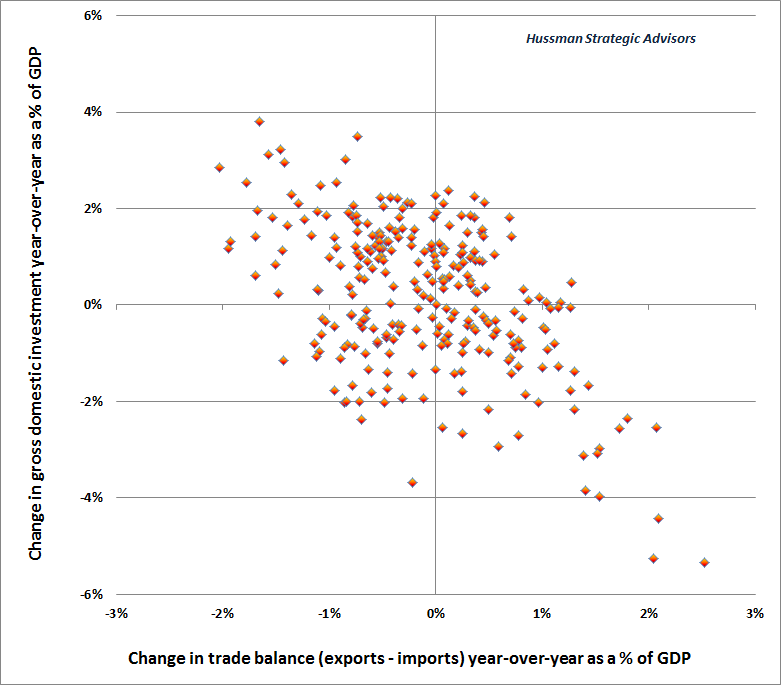

One of the most significant dangers our economy faces here is that 45’s dogmatic approach to trade deficits is inadvertently courting a recessionary collapse in gross domestic investment. See, the fact is that rapid growth in U.S. domestic investment is also typically associated with rapid deterioration in the U.S. trade deficit (an implication of the savings-investment identity, as explained below). For that reason, we observe a very strong regularity across history: the quickest way to “improve” the U.S. trade balance is to torpedo gross domestic investment, and the quickest way to “worsen” the U.S. trade balance is to enjoy a boom in gross domestic investment. The chart below illustrates this regularity in post-war data.

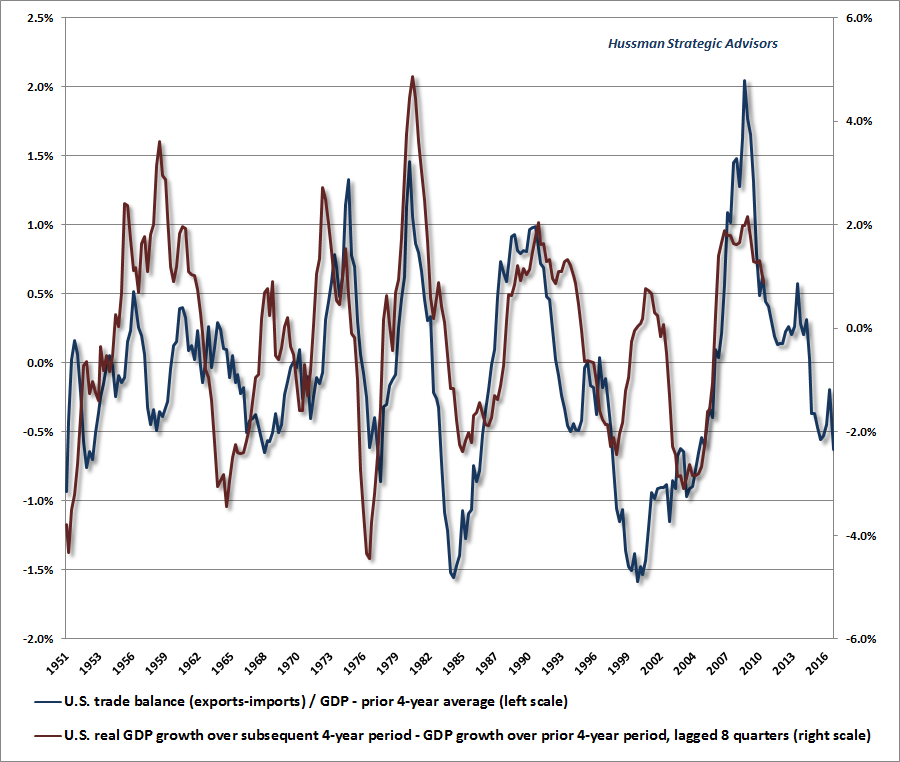

Why are changes in U.S. gross domestic investment related to opposite changes in the trade balance? Well, recall that it’s not just a theory, but an accounting identity, that gross domestic investment must be funded by an identical amount of saving, of which there are three sources: U.S. private saving, U.S. government saving, and foreign saving. Every time we import $1 of “stuff” from foreign countries, we pay for it by exporting $1 of “stuff” in return. That “stuff” can be either goods and services, or securities. By definition, if the U.S. is importing more goods and services from foreign countries than it exports, it must also be true that the U.S. is exporting more securities to foreign countries than it imports. So a “trade deficit” is equivalent to a “net export of securities,” which is equivalent to an inflow of foreign savings. The bottom line is simple: when U.S. gross domestic investment enjoys a boom (particularly when the U.S. government is already running a deficit and U.S. private saving is weak) the U.S. trade deficit typically widens considerably. This, by the way, is also the reason the U.S. becomes more vulnerable to running large trade deficits when the government is running a large budget deficit. From a cyclical perspective, the problem is that once the trade balance is already at a significant deficit, there is little remaining slack for rapid expansion in either gross domestic investment or, by extension, U.S. productivity growth. Periods of rapid economic growth typically emerge from points of high unemployment - not when unemployment is already quite low. Likewise, periods of rapid economic growth typically emerge from points where the trade balance (exports - imports) is elevated as a share of GDP - not when it is already at a steep deficit. Because of these dynamics, U.S. economic growth tends to mirror (with a lag of about 8 quarters) the profile of the U.S. trade balance. The chart below illustrates this regularity. The blue line shows the U.S. trade balance as a share of GDP, relative to its prior 4-year average. The red line shows subsequent growth in U.S. GDP over the subsequent 4-year period, relative to the prior 4-year average.

The upshot is this. Over the coming 7-10 years, the central tendency of U.S. GDP growth is likely to average only about 2%, a result that is largely baked-in-the-cake because of the underlying drivers already in place. On a cyclical horizon focused on the coming 4-year period, the diminished slack in core economic drivers is consistent with a material slowing of economic growth relative to its average in recent years. Given that real U.S. GDP growth has averaged just 2.2% over the past 4 years, and that the current starting positions of labor force growth, unemployment, and the trade balance suggest a deceleration even from that average, we shouldn’t be surprised if real U.S. GDP growth amounts to just a fraction of a percent annually over the coming 4-year period. See my November 2003 comment, The U.S. Productivity Miracle (Made in China) for more on the relationship between trade and productivity. Informed Policy The policy menu currently under discussion threatens to materially worsen the arithmetic of U.S. economic growth. Limiting immigration, for example, will further constrain the component of labor force growth. Attempts to forcibly narrow the trade balance will torpedo gross domestic investment. Appeals to the economic impact of tax reforms in the 1950’s and 1980’s conflate the effect of tax reductions with the impact of factors, already in place at those points, that have regularly created the conditions for rapid economic growth. Though a great deal of hope is being placed on corporate tax reform, the effective tax rate of U.S. corporations (taxes actually paid as a fraction of pre-tax profits) is already lower than at any point in the post-war era prior to the 2008-2009 economic collapse. Even cutting the statutory rate in half from here would result in a likely bump to corporate profits of less than 10%. As for repatriation of cash held overseas, a similar tax holiday in 2004 resulted primarily in bonuses and stock repurchases, while the corporations that benefited most actually cut employment and decreased research spending. Meanwhile, foreign cash holdings pose virtually zero funding constraints. As I've noted before, major corporations already have ample access to funding for any project they could reasonably consider. Even if cash is held overseas, it’s rather easy for corporations to effect interest-rate swap transactions that effectively make the funds available domestically. There are many actions we can take as a nation to improve our capacity for long-term economic growth, including an emphasis on productive, sustainable and non-duplicative infrastructure; greater investments in education and workforce training; increased immigration of high-skilled workers (who have a multiplier effect on both national income and employment); a substantial increase in the number of H1B visas; expansion of training, incentives and even immigration of workers in fields such as home and community health (where an aging population is likely to pose substantial demands); increased incentives for research and development; and substantially enhanced funding of scientific research through the NIH, NSF and other agencies. It also should not be overlooked that domestic workers are frequently unwilling to take many agricultural, food service and custodial jobs that immigrants accept with dignity. With regard to low-skilled domestic workers, the fact is that the incomes of low-skilled workers are typically highest in areas where high-skilled workers are most plentiful. Productive investment is essential, and misguided efforts at protection will actually have the effect of cratering gross domestic investment. Meanwhile, tax cuts don’t “trickle down” or “spill over” a fraction as much as knowledge, skills, and education can. We are doing exactly the opposite of what an informed nation with a comparative advantage in innovation should do, and the ignorance inherent in the current policy direction will produce only more of itself.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |