|

|

||||||

|

|

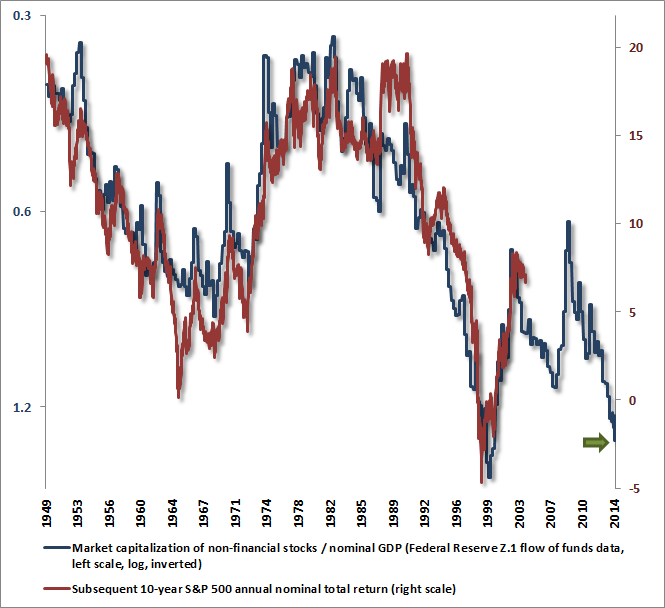

July 7, 2014 Quotes on a Screen and Blotches of Ink With the fresh high in the S&P 500 Index last week, our estimates of prospective 10-year S&P 500 nominal total returns have fallen below 1.8% annually. At shorter horizons and on historically reliable measures, our estimates of S&P 500 total returns are now negative at every horizon shorter than 8 years. Investors who feel that zero interest rate policy offers them “no choice” but to hold stocks are likely choosing to experience negative returns instead of zero. While millions of investors appear to have the same expectation that they will be able to sell before everyone else, the question “sell to whom?” will probably remain unanswered until it is too late. Meanwhile, we should recognize that each additional year where short-term interest rates are held at zero (rather than a more normal level of about 4%) is actually worth only an increase in market valuation of that same 4%. This is basic arithmetic. To see this, suppose that 30-year zero-coupon bonds normally yield 3% more than risk-free Treasury bills. In a world of 4% Treasury bill yields, the riskier bonds would yield 7%, with a price of $13.14 assuming a face value of $100. If short-term yields were expected to be zero for two years, normalizing thereafter, investors would price the 30-year bonds to return just 3% for the first two years, then 7% thereafter. The price that would be consistent with that result is $14.18 (= 100/{(1.07)^28 * (1.03)^2}). Not surprisingly, that’s about 8% higher than the bond would be valued in the absence of two years of zero interest rate policy. Now assume 5 years of zero interest rate policy. The associated impact would be to raise the bond price to $15.89, which is not surprisingly just over 20% higher than the bond would be valued at in a constant 4% world. The same arithmetic applies for equities, and can be demonstrated using any discounted cash flow approach. In this context, the fact that historically reliable valuation methods imply negative total returns at every horizon shorter than 8 years does not simply reflect the expectation of 8 years of zero interest rate policy, but 8 years of zero interest rate policy combined with zero compensation for the substantial additional risk of holding equities. Assuming that a modest risk premium is appropriate for an asset class that has proven itself quite capable of repeatedly losing half of its value, current equity valuations are reasonable only if one assumes more than two decades of zero interest rate policy. Even in that case, “reasonable” would still imply commensurately low equity returns in the mid-single digits over the next two decades. At a time when we should be pounding the table about risk, we are quietly stating our case. At this point even that is something of a lightning rod for disdain. As we observed after the 2000-2002 and 2007-2009 plunges, our concerns have a tendency to hold weight only after the fact (see Setting the Record Straight and This Time is Different, Yet With the Same Ending to understand our experience in the half-cycle since 2009). There’s certainly no point in urging anyone to sell – doing so only means that some other poor investor would have to hold the bag over the completion of this cycle. It’s an unfortunate situation, but much of what investors view as “wealth” here is little but transitory quotes on a screen and blotches of ink on pieces of paper that have today’s date on them. Investors seem to have forgotten how that works. Few are likely to realize that apparent wealth by selling, and those that do will essentially be redistributing it from the investors who buy. Meanwhile, don’t confuse time to sell with opportunity to sell. Trading volume remains quite tepid, and the majority of that volume represents existing owners exchanging what they hold rather than outright entry and exit. The investors who successfully leave the equity market at current valuations will exit through a needle’s eye. Implied volatility in S&P 500 index options fell to just 10.3% last week, indicating enormous complacency about potential risk. I’ve noted before that extreme overvalued, overbought, overbullish conditions tend to feature “unpleasant skew”: the raw probability of an advance is typically greater than the probability of a decline, so the market tends to achieve a series of successive but fairly marginal new highs, which can feel excruciating for investors in a defensive position. The “skew” part is that while the raw probability favors an advance, the remaining probability often features vertical drops that can wipe out weeks or months of market gains in a handful of trading days. We’ve certainly seen an unusual persistence of overvalued, overbought, overbullish conditions without consequence in recent quarters, but it is notable that the implied skew in S&P 500 index options has soared. Indeed, the ratio of implied skew to implied volatility spiked to the highest level in history on Friday. Again, we’ll quietly state our case here, with an understanding that there is little use in waving our arms about. Again, on a broad range of historically reliable measures, our estimate of 10-year S&P 500 nominal total returns is now less than 1.8% annually. That said, the most reliable measures actually project negative returns, but then, the most reliable measures are those that adjust most fully for cyclical variations in profit margins, and we are continually reminded that this time is different. The ratio of market capitalization to GDP, which Warren Buffett (correctly) observed in a 2001 Fortune interview is “probably the single best measure of where valuations stand at any given moment” is now about 150% (not just 50%) above its pre-bubble norm, even imputing a rebound in Q2 GDP growth. Of course, Buffett also wrote "A group of lemmings looks like a pack of individualists compared with Wall Street when it gets a concept in its teeth" - which may explain why Wall Street seems so entranced with the concept of QE instead of actually doing the math. The ratio of market capitalization to GDP is beyond every point in history except for the final quarter of 1999 and the first two quarters of 2000. The chart below illustrates the (log) ratio of nonfinancial market capitalization to GDP in blue, on an inverted scale at left. The red line is the actual subsequent 10-year nominal annual total return of the S&P 500 (right scale). While there's no assurance that the relationship between valuations and subsequent market returns will continue (and no concern about that prospect among many speculators anyway), the green arrow shows where the ratio stands at present.

A warning from the Bank for International Settlements Last week, the Bank for International Settlements, which acts as the central bank to central banks, issued its annual report. It is about the most insightful warning that one is likely to see from the central banking system, even if the Federal Reserve, ECB and other individual central banks are the ones being warned. “Financial markets have been exuberant over the past year, at least in advanced economies, dancing mainly to the tune of central bank decisions. Volatility in equity, fixed income and foreign exchange markets has sagged to historical lows. Obviously, market participants are pricing in hardly any risks. In advanced economies, a powerful and pervasive search for yield has gathered pace and credit spreads have narrowed. The euro area periphery has been no exception. Equity markets have pushed higher. To be sure, in emerging market economies the ride has been much rougher. At the first hint in May last year that the Federal Reserve might normalize its policy, emerging markets reeled, as did their exchange rates and asset prices. Similar tensions resurfaced in January, this time driven more by a change in sentiment about conditions in emerging market economies themselves. But market sentiment has since improved in response to decisive policy measures and a renewed search for yield. Overall, it is hard to avoid the sense of a puzzling disconnect between the markets’ buoyancy and underlying economic developments globally. “In the countries that have been experiencing outsize financial booms, the risk is that these will turn to bust and possibly inflict financial distress. Based on leading indicators that have proved useful in the past, such as the behaviour of credit and property prices, the signs are worrying. “Term and risk premia can only be compressed up to a point, and in recent years they have already reached or approached historical lows. The risk is that, over time, monetary policy loses traction while its side effects proliferate. These side effects are well known (see previous Annual Reports). Policy may help postpone balance sheet adjustments, by encouraging the evergreening of bad debts, for instance. It may actually damage the profitability and financial strength of institutions, by compressing interest margins. It may favour the wrong forms of risk-taking. And it can generate unwelcome spillovers to other economies, particularly when financial cycles are out of synch. Tellingly, growth has disappointed even as financial markets have roared: the transmission chain seems to be badly impaired. The failure to boost investment despite extremely accommodative financial conditions is a case in point. “Good policy is less a question of seeking to pump up growth at all costs than of removing the obstacles that hold it back. When policy responses fail to take a long-term perspective, they run the risk of addressing the immediate problem at the cost of creating a bigger one down the road. Debt accumulation over successive business and financial cycles becomes the decisive factor. “In contrast to what is often argued, central banks need to pay special attention to the risks of exiting too late and too gradually. This reflects the economic considerations just outlined: the balance of benefits and costs deteriorates as exceptionally accommodative conditions stay in place. And political economy concerns also play a key role. As past experience indicates, huge financial and political economy pressures will be pushing to delay and stretch out the exit. “The current weakness of aggregate demand may suggest the need for further monetary stimulus or for easing the pace of fiscal consolidation. However, these policies are likely to be either ineffective in current circumstances or unsustainable: taking a long-term perspective, they may simply succeed in bringing forward spending from the future rather than increasing its overall amount over the long run, while leading to a further rise in public and private debt. Instead, the only way to boost demand in a sustainable manner is to raise the production capacity of the economy by removing barriers to productive investment and the reallocation of resources. This is even more important in the face of declining productivity growth. “The benefits of unusually easy monetary policies may appear quite tangible, especially if judged by the response of financial markets; the costs, unfortunately, will become apparent only over time and with hindsight. This has happened often enough in the past. And regardless of central banks’ communication efforts, the exit is unlikely to be smooth. Seeking to prepare markets by being clear about intentions may inadvertently result in participants taking more assurance than the central bank wishes to convey. This can encourage further risk-taking, sowing the seeds of an even sharper reaction. Moreover, even if the central bank becomes aware of the forces at work, it may be boxed in, for fear of precipitating exactly the sharp adjustment it is seeking to avoid. A vicious circle can develop. In the end, it may be markets that react first, if participants start to see central banks as being behind the curve. This, too, suggests that special attention needs to be paid to the risks of delaying the exit. Market jitters should be no reason to slow down the process. “The temptation to postpone adjustment can prove irresistible, especially when times are good and financial booms sprinkle the fairy dust of illusory riches. The consequence is a growth model that relies too much on debt, both private and public, and which over time sows the seeds of its own demise. More generally, asymmetrical policies over successive business and financial cycles can impart a serious bias over time and run the risk of entrenching instability in the economy. Policy does not lean against the booms but eases aggressively and persistently during busts. This induces a downward bias in interest rates and an upward bias in debt levels, which in turn makes it hard to raise rates without damaging the economy – a debt trap. Systemic financial crises do not become less frequent or intense, private and public debts continue to grow, the economy fails to climb onto a stronger sustainable path, and monetary and fiscal policies run out of ammunition. Over time, policies lose their effectiveness and may end up fostering the very conditions they seek to prevent. In this context, economists speak of ‘time inconsistency’: taken in isolation, policy steps may look compelling but, as a sequence, they lead policymakers astray. “The risks of failing to act should not be underestimated.” The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Only comments in the Fund Notes section relate specifically to the Hussman Funds and the investment positions of the Funds. Fund Notes We’ve increasingly taken the view that there may be a benefit in refraining from telegraphing changes in our investment position, except where comments may help shareholders to interpret various day-to-day movements in the Funds. Broadly speaking, the Hussman Funds remain defensive toward equities and Treasury securities, with a constructive stance toward precious metals shares. While our estimates of prospective market return/risk have been unusually negative, we’ve been relatively slow to raise the strike prices of the index put option side of our hedges in Strategic Growth Fund, which has helped somewhat in reducing the discomfort of aligning our investment position with historically hostile market conditions. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |