|

|

||||||

|

|

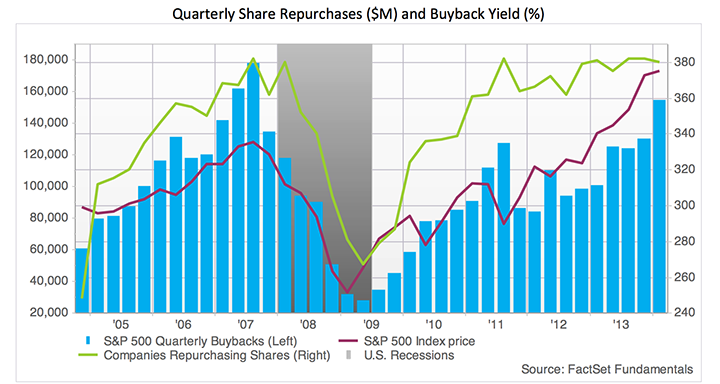

September 22, 2014 The Ponzi Economy In the decade and a half since the late-1990’s, the U.S. economy has undergone a fundamental shift. The signs of this shift can be observed at the foundation of our standard of living, as both accumulation of productive capital and participation in the labor force have buckled. What obscures this fundamental deterioration is that activity at the surface still appears quite stable. It’s important to understand why this is so. The standard of living of a country is measured by the amount of output that individuals are able to consume as a result of their work. The productivity of a country is measured by the amount that individuals are able to produce as a result of their work. Over time, growth in the standard of living is chained to and limited by growth in productivity. Productivity, in turn, rests on two factors: a productive capital base, and an active pool of productive domestic labor. The accumulation of productive factors is what drives long-term growth. When the most persistent, most aggressive, and most sizeable actions of policymakers are those that discourage saving, promote debt-financed consumption, and encourage the diversion of scarce savings to yield-seeking financial speculation rather than productive investment, the backbone that supports a rising standard of living is broken. With respect to the U.S. capital base, real gross domestic investment has crawled at an annual growth rate of just 1.4% since 1999, compared to 4.9% real annual growth in the preceding half-century. During that same 15-year period, the U.S. labor force participation rate has collapsed from a record high to the lowest level since the 1970’s, wages and salaries have plunged to a record low share of GDP, and real median household income has contracted by a cumulative 9%. But there are wrinkles in this story, which make present conditions feel better than this deterioration would suggest. A country can insulate itself from its own deteriorating productivity, for a time, if continued consumption is financed by the accumulation of debt (and its partner, the printing of money). The U.S. has gone from the largest creditor nation in the world to its largest debtor by shifting from accumulation to dissaving. Statistics reflecting modest 2.1% growth in output per hour since 1999 also make us feel somewhat better about declining labor force participation, but as I detailed more than a decade ago in The U.S. Productivity Miracle (Made in China), our measures of productivity growth are heavily influenced by U.S. imports and foreign labor outsourcing. We import intermediate goods we would have produced at home, but at cheaper prices, meaning that the deduction from GDP on account of imports is proportionally smaller than the corresponding loss in U.S. employment. As Fabrizio Galimberti noted in the Economist, foreign outsourcing has the effect of artificially raising productivity figures because subtracting imports from GDP does not adequately correct for their impact on final output, yet foreign labor is not counted in the denominator, so measured output per U.S. worker increases. Meanwhile, financial repression by the Federal Reserve has held interest rates at zero, discouraging savings while encouraging and enabling households to go more deeply into debt. Various forms of deficit-financed government assistance and unemployment compensation have also been used to make up the shortfall, allowing consumption, and by extension, corporate revenues and profits, to be sustained. As long-term economic prospects have deteriorated, the illusion of prosperity has been maintained through soaring indebtedness, coupled with yield-seeking speculation in risky assets that has repeatedly (albeit not always immediately) been followed by crashes throughout history. Distribution, diversity, and winner-take-all markets That’s not to say that this apparent prosperity must be, or has been, evenly distributed. As I observed in Broken Links: Fed Policy and the Growing Gap Between Wall Street and Main Street, the misallocation of scarce savings from productive purposes to speculative ones; the thinning of the domestic capital base; the weakening of local linkages between lenders, borrowers, producers and consumers; the “massive macro” focus of policymakers, the sausage-factory securitization of locally originated loans by remote Wall Street institutions; the expansion of information technology; and our broadening foreign trade with low-wage countries that lack many of the human rights protections that we take for granted, have all contributed to the emergence of “winner-take-all” features in the U.S. economy. Local interactions, local recycling of economic resources, and economic multiplier effects have progressively weakened as the economy moves toward a system that favors remote interactions that channel resources out of local economies and up the food chain toward a few dominant players. The largest initial public offering of stock in history, Friday’s IPO of a Chinese business-to-business e-commerce site, is an example of such winner-take-all dynamics. This process can also be observed in the form of too-big-to-fail banks, an “all eyes on the Fed” financial system, an enormous widening in the distribution of income, and a hollowing out of the U.S. middle class. There are additional risks in “winner-take-all” and “too-big-to-fail” monocultures. From the study of complex adaptive systems, we know that local and diverse relationships contribute to stability, while remote and overspecialized relationships invite greater disruption as a result of crises or single points of failure. The reason that species go extinct is that they overspecialize in ways that are highly adaptive in one particular state of the world but prove to be insufficiently flexible when the environment changes. As we discovered in the most recent economic cycle, the notion that “all real estate is local” was turned on its head as Fed-induced yield seeking, pooling of mortgages in complex securities, and excessive reliance on too-big-to-fail banks all collaborated to create a single point of failure that propagated through the global economy as the deepest collapse since the Great Depression. One would be naïve to imagine that the Fed-enabled entrenchment of enormous financial institutions and the “massive macro” focus of economic policy have done anything to enhance our long-term resilience. Alongside the deterioration in the U.S. capital base and labor market has been an increasing and perpetual reliance on various forms of “stimulus” through government deficit spending and monetary intervention. What’s essential to understand is that these forms of “stimulus” are not just additional symptoms of this economic shift. They have become the causes and the guardians of it. Suppressed interest rates have encouraged a continuous diversion of scarce savings toward what is effectively debt-financed gambling. Meanwhile, cheaply financed deficit spending anesthetizes the consequences of deteriorating productive factors, allowing the U.S., for a time, to feast on the geese that could lay its golden eggs. To be clear, deficit spending and monetary stimulus can be appropriate as a sort of short-run “kindling” to ease constraints on the economy that would otherwise be binding. But it is important to measure the impact of these policies not simply on the basis of subsequent economic activity, but also on the basis of observed capital formation. The accumulation of debt cannot ultimately be repaid without accumulating the productive means to do so. Instead, since the late-1990’s, we’ve moved to an economy where stimulus is sought at every turn, and a blind eye is cast toward issues of speculation and financial stability, in the belief that stimulus itself can be the wood that sustains the fire and can be applied perpetually without consequence. The Ponzi Economy The central point is this. The U.S. economy has shifted course from one of productive capital accumulation to a reliance on continuous expansion of debt in excess of the economic ability to repay it. Call this the Ponzi Economy. The U.S. Ponzi Economy is one where domestic workers are underemployed and consume beyond their means; household and government debt make up the shortfall; corporate profits expand to a record share of GDP as revenues are sustained by household and government deficits; local employment is replaced by outsourced goods and labor; companies refrain from productive investment, accumulate the debt of other companies and issue new debt of their own, primarily to repurchase their own shares at escalating valuations; our trading partners (particularly China and Japan) become our largest creditors and accumulate trillions of dollars of claims that can effectively be traded for U.S. property and future output; Fed policy encourages the yield-seeking diversion of scarce savings toward speculation in risky securities; and as with every Ponzi scheme, everyone is happy as long as nobody seeks to be repaid. If you wonder why the economy feels “fine” despite the persistent thinning of the U.S. capital base and the hollowing out of its middle class, it’s because we are covering the shortfall at every turn with the endless issuance of cheap debt that needs to be rolled forward forever. Of course, not all debt should be treated equally. From my perspective, until we observe inflationary pressures, U.S. Treasury debt will remain a safe-haven that is likely to be more in demand than not at points of crisis. Over the longer-term, we may very well observe inflationary outcomes (or the need for inflationary outcomes) that reduce the real value of this debt, but I continue to believe that any significant inflationary cycle is much more likely to follow the next cyclical economic downturn than it is to precede it. While debt accumulation often leads to default in countries that cannot print their own currencies, and can produce currency crises in countries with fixed exchange rates, U.S. government debt is likely to result – probably late in this decade – in a more conventional inflationary cycle that reduces its real value. In contrast, we view corporate and junk yields as insufficient to justify their additional credit risk at present levels, and we are particularly concerned at the increasing issuance of corporate debt to obtain what amounts to leveraged exposure to equities at historically extreme valuations (either through share buybacks or acquisitions). Buybacks are not a return of capital to shareholders – they are partly a leveraged speculation on shareholder’s behalf, partly a strategy to enhance per-share earnings by reducing share count, and partly a way to reduce the dilution from stock-based compensation to corporate insiders. Moreover, repurchases move in tandem with corporate debt issuance, which is another way of saying that the history of stock buybacks is one of companies using debt to buy their stock at overvalued prices. Keep in mind also that corporate share repurchases have no tendency to concentrate at points of depressed valuation, and but have instead been disproportionately aggressive at points that have historically represented severe overvaluation. The chart below (h/t Thad Beversdorf) illustrates this regularity. See The Two Pillars of Full-Cycle Investing for additional data.

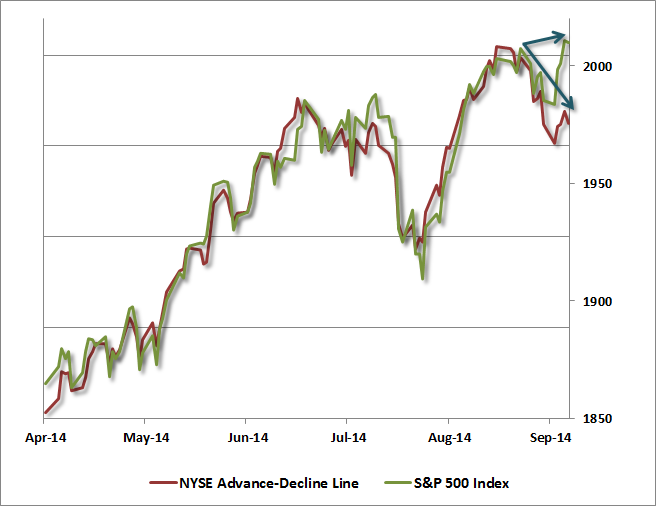

Given that the majority of corporate debt issuance is shorter than 8 years, and we estimate nominal S&P 500 total returns to be negative at that and shorter horizons (with our estimates rising to just 1.5% annually on a 10-year horizon), my view is that issuing corporate debt to repurchase equity presently represents value destruction, and also weakens corporate balance sheets. Credit spreads are widening already, and the history of credit spreads (as with equity risk premiums) is that they normalize in abrupt spikes. We don’t expect a massive wave of defaults, but we do believe that junk yields in particular are lower than the default rates that investors are likely to observe on those securities in the coming years. The next decision Though a certain amount of disruption resulting from overvalued financial markets, compressed risk premiums, and excessive debt issuance is baked-in-the-cake, there is also a ray of hope. Regardless of the point the U.S. economy has arrived to, there is room to improve matters by making each next decision well. Those next decisions should include policies that increase bank capital requirements (particularly through the use of convertible debt that would automatically convert to equity if existing capital becomes insufficient); investment tax credits, job training credits, and other incentives to deepen the domestic base of productive capital and labor; an abandonment of financial repression by the Federal Reserve and a gradual normalization of interest rates that would increase savings, discourage speculative yield-seeking, and allow the markets to signal supply and scarcity without distortion; the enhancement of local enterprise zones; and policies that discourage the endless expansion of too-big-to-fail institutions and massive leveraged transactions in favor of traditional, local banking institutions and greater availability of capital to small businesses that create two-thirds of all U.S. jobs. Despite the short-term enjoyment that comes from living within an ever-growing Ponzi scheme, our long-term economic future relies on ending it. Market internals continue to deteriorate An important note on the equity markets: we’re observing a continued deterioration in market internals at extremely elevated valuations, much as we observed in July 2007 (see Market Internals Go Negative). Credit spreads have widened in recent weeks, breadth has deteriorated (resulting in weakness among the average stock despite marginal new highs in several major indices), and downside leadership is also increasing. As a small example that illustrates the larger point, despite the marginal new high in the S&P 500 last week, the NYSE showed more declines than advances, and nearly as many new 52-week lows as new 52-week highs. About half of all equities traded on the Nasdaq are already down 20% from their 52-week highs and below their 200-day averages. Small cap stocks have also weakened considerably relative to the S&P 500. Indeed, though it’s not a signal that factors into our own measures of market internals (and we also wouldn’t put much weight on it in the absence of deterioration in our own measures), it’s interesting that Friday also produced a “Hindenburg” signal as a result of that lack of internal uniformity: both new highs and new lows exceeded 2.5% of issues traded, the S&P 500 was above its 10-week average, and breadth as measured by advance-decline line is deteriorating. One can certainly wait for greater internal divergence before raising concerns, but my impression is that this confirmation is likely to emerge in the form of a steep, abrupt initial decline (which we call an “air pocket”). That isn’t a forecast, but an observation based on prior instances of deteriorating uniformity following extended overvalued, overbought, overbullish periods. This time may be different. Needless to say, we aren’t counting on that. The chart below shows the cumulative NYSE advance-decline line (red) versus the S&P 500. While the divergence is not profound, similar and broader divergences are appearing across a wide range of asset classes and security types, and it’s the uniformity of those divergences – not simply the extent – that contains information that suggests that investor risk preferences are subtly shifting toward risk aversion.

The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Only comments in the Fund Notes section relate specifically to the Hussman Funds and the investment positions of the Funds. Fund Notes The Hussman Funds remain defensive toward equities, with a moderately constructive stance toward Treasury securities and precious metals shares. The most important feature we observe at present is the deterioration of market internals in the past several weeks. We observe this in weakening breadth (advances versus declines), leadership (new highs versus new lows), small capitalization stocks, and credit spreads (junk yields and BAA yields versus Treasury and AAA credit) among other internals. Over the short-run, this has the side-effect that broadly diversified portfolios that are not capitalization-weighted may not track the major indices well. For example, the Russell 2000 Index of smaller capitalization stocks was down more than 1% on Friday, versus a nearly unchanged S&P 500 Index. While my expectation is that the major indices are likely to fall in line with market internals rather abruptly, to the extent that they do not (as has been the case in the past few weeks), we’ll tend to observe some day-to-day fluctuations in our hedged portfolios on days when our broadly diversified stock holdings don’t closely track the indices we use to hedge. Since our primary hedge in Strategic Growth (and Strategic Dividend Value) is in the S&P 500, much of that day-to-day fluctuation can be understood by quickly comparing how much dispersion there was between the S&P 500 Index and broader indices on a given day. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |