|

|

||||||

|

|

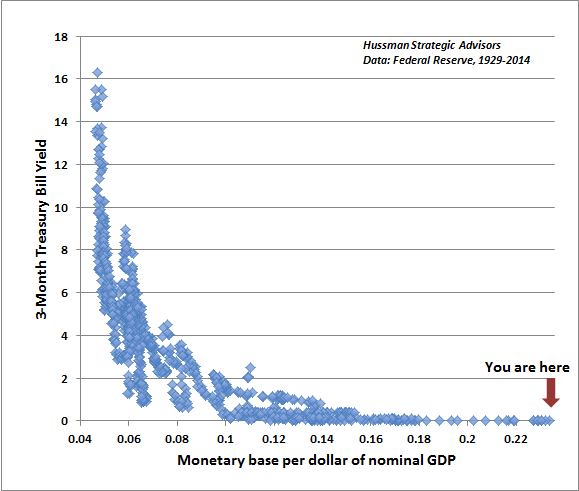

December 15, 2014 A Sensible Proposal and a New Adjective A week ago, FOMC member Richard Fisher observed “It strikes me as timely for the Fed to consider implementing one of the possible options under the ‘normalization principles’ the FOMC articulated in September: allowing our security holdings to run off as the bonds in our massive portfolio mature... Mind you, the above proposition does not imply any rush to raise the fed funds rate or its equivalents, such as the rate on excess reserves.” As the FOMC considers the way forward, Fisher’s proposal makes a great deal of sense. Some additional evidence in support of that direction may be helpful. 1) Liquidity preference: The Federal Reserve could presently roll more than one-third of its current asset holdings off of its balance sheet without producing any departure of the Federal Funds rate or Treasury bill yields from zero. Nearly a century of Federal Reserve data demonstrates very clearly that short-term interest rates are a well-behaved function of the size of the monetary base (currency and bank reserves) relative to nominal GDP. The chart below shows this relationship – our empirical version of what economists know as the “liquidity preference curve.” Put simply, when the economy is flooded with base money that earns zero, or nearly-zero interest, the first response of individuals is to seek near-alternatives to cash. The closest default-free, liquid alternatives are Treasury bills. Those alternatives are bid up in price, and down in yield, until individuals are indifferent between holding base money and holding Treasury bills. Today, the yield that produces indifference is exactly zero. More importantly, that indifference-yield would still be zero if the monetary base was reduced by more than one-third.

Notice that as Treasury bill yields are driven to compressed levels, investors and speculators respond by reaching beyond default-free assets, toward securities that carry greater risk. A decade ago, that Fed-induced reach-for-yield was largely directed toward mortgage securities, which until then had been reasonably default-free. The yield-seeking demand of investors and speculators for securities promising a “pickup” over suppressed Treasury bill yields naturally resulted in a response by Wall Street to create more “product” by creating new mortgage securities – eventually with little or no regard for the creditworthiness of those who obtained the mortgages. These were packaged through tortuous slicing-and-dicing by financial engineers (to boost their credit ratings) and sold to investors. Hedge funds and other speculators went further, borrowing at depressed short-term interest rates and using that leverage to buy riskier and higher-yielding mortgage securities in an effort to “leverage the carry” - all ultimately feeding a housing bubble whose inevitable collapse provoked the deepest economic crisis since the Great Depression. Policy makers learned little from that episode. In recent years, a similar reach-for-yield has driven equity valuations to levels that are now about double their historical norms, based on historically reliable measures that are about 90% correlated with actual subsequent 10-year market returns. Suppressed interest rates do not “justify” this elevation. Any standard discounting approach can be used to demonstrate that if “normal” valuations are associated with short-term interest rates averaging say 4%, the promise of even 3-4 years of zero short-term interest rates should result in longer-term risk assets being priced only 12-16% above their respective valuation norms. Likewise, current or year-ahead earnings projections do not “justify” present equity valuations, unless one ignores a century of evidence that major peaks in the equity market are always associated with cyclically elevated earnings well above their long-term trend, which in turn always understates observed price/earnings multiples at major peaks. A century of historical evidence can also easily be brought to bear to demonstrate that valuation measures having limited sensitivity to cyclical swings in profit margins have a dramatically stronger correlation with actual subsequent equity market returns. Once again, investors and speculators have also reached for yield in low-quality debt, producing a boom in junk bond issuance and leveraged loans (loans to already indebted borrowers), with the majority of those new loans having “covenant-lite” features that reduce the protection of the lender in the event of bankruptcy. Moreover, much of the trillion dollars of outstanding leveraged loans are held by major U.S. banks in the form of “participating shares,” an indirect form of ownership that has been repudiated by the FDIC. As KBRA bond rating agency recently observed, “Today, many leveraged loans continue to be participated to banks, insurers, and bond funds in a manner that raises similarly questionable rights in the event that the lead bank or non-bank sponsor fails. The intense competition for assets among institutional investors caused by low interest rate policies has, it appears, caused a deterioration in both the perception and the terms of structural protections that we believe could create future risks for investors and the global financial system. The lesson of finance and financial law is that protection which ends at the doorstep of a trustee or receiver is no protection whatsoever.” 3) Risk of capital loss: Unless 10-year bond yields normalize by less than 1% over the coming three-year period, a policy of reinvesting proceeds as existing Federal Reserve securities mature is likely to produce a net loss for the Federal Reserve. That loss would represent a subtle form of fiscal policy – effectively allocating public funds to finance the payment of interest to banks for the questionable economic service of holding idle reserve balances. As holdings on the Federal Reserve balance sheet roll off at expiration, the decision to reinvest the proceeds by purchasing new bonds is, in effect, an investment decision by the FOMC. The potential loss of that investment can be specified by a profile of “breakeven” yields over time. For example, consider the decision to purchase a 10-year, 2% coupon bond at a yield of 2.1%. If the 10-year yield is anything greater than 2.36% a year from today, 2.68% two years from now, or 3.10% three years from now, the return of that bond (including interest) over that holding period will be negative. Since the Federal Reserve already pays 0.25% to banks as interest on idle reserves, the breakeven rates after that expense are actually a bit lower, at 2.33% and 2.61% and 2.98% respectively. Those breakeven rates will move lower still in the event the FOMC raises the rate of interest on reserves. Notice that there are essentially two ways by which a normalization of short-term yields toward say, 4% could be achieved in the years ahead. The conventional approach would involve reducing the Fed’s balance sheet to 8 cents of monetary base per dollar of nominal GDP (see the liquidity preference curve above). This could be done either by reducing the monetary base by two-thirds, or theoretically through a tripling of nominal GDP (assuming inflation expectations could be held in check, since most of that adjustment would have to represent inflation). Alternatively, the Fed could achieve higher rates through the payment of interest on reserves. But would reinvesting principal as it matures and holding those bonds to maturity be useful in that process? Not at all. Notice that at the current 10-year Treasury yield of 2.1%, a diagonal normalization of short-term rates from 0% to 4% would exhaust the cumulative total return of the bond if the 4% target was achieved much sooner than a decade from now. As such, the only way to avoid a net loss on the newly reinvested principal would be on the expectation of an extremely low future 10-year trajectory for Fed policy rates. For all of these reasons, the FOMC is well-served by Richard Fisher’s proposal to consider terminating the current policy of reinvesting proceeds from Fed balance sheet holdings as those securities mature. Again, that shift implies no rush to raise the federal funds rate or otherwise normalize policy rates. Finally, with respect to policy language surrounding the timeline of policy normalization, the Fed could certainly reflect continuing economic uncertainties by changing the phrasing in its guidance from “considerable time” to “appreciable time.” Considerable (adj): notably large in size, amount, or extent. Appreciable (adj): large or important enough to be noticed. Market behavior: distinctions matter Last week’s market action, like the decline we observed in October, was a fairly standard reflection of the kind of abrupt “air pocket” that we normally see across history following points of extreme overvalued, overbought, overbullish conditions. Those events are usually characterized by what I’ve called “unpleasant skew” – a persistent series of slight marginal new highs, followed by an abrupt decline that wipes out weeks or months of upside progress in a handful of sessions. Last week’s decline was too shallow to materially change our classification of the market return/risk profile, so equities appear vulnerable to more extended weakness for now. My impression is that the recent weakness in the equity market and the plunge in Treasury yields have not been “caused” by weakness in the energy market, but that all are joint symptoms of a synchronous downturn in global economic growth, most obvious in Japan and Europe, and increasingly developing in England, China, and elsewhere. It's a reasonable concern that this softening may include the U.S. economy. In U.S. data, we don’t observe much evidence of recession risks at present, but that evidence can emerge fairly rapidly. A large-scale credit event would obviously heighten our immediate economic concerns. We’re particularly attentive to clear upward pressure on credit spreads and risk premiums here. Having fully addressed the two challenges we openly wrestled with in the half cycle since 2009 (see Hard Won Lessons and the Bird in the Hand), I remain convinced that we can finally put a box around this period as a completed transition from our effective pre-2009 methods to our present methods (which we’ve validated in market cycles across history, notably including Depression-era data, the recent cycle, and even the period since 2009). Undoubtedly, the word “transition” will be paired with unseemly adjectives and expletives until we demonstrate outcomes that match or exceed those we enjoyed before my unfortunately-timed insistence in 2009 on stress-testing our methods against Depression-era outcomes. In the meantime, it’s clear that periods classified with negative return/risk profiles under our present classification methods have had quite severe implications, on average – even in periods of easing Federal Reserve policy. See A Most Important Distinction for a chart of the cumulative performance of the S&P 500 under the market return/risk profile we currently identify. In recent years, there is one legitimate way that “this time” has been “different” as a result of yield-seeking speculation induced by quantitative easing. Historically, extremely overvalued, overbought, overbullish conditions were followed by corrective plunges in relatively short order, yet the consequences of those same syndromes have been persistently deferred in recent years. If one wishes to share what we’ve learned from our struggle with this episode, without dispensing with the benefit of a discipline that ultimately made us look like evil geniuses in prior cycles, it will help to learn the right lesson. As I’ve noted frequently in recent months, and detailed in Air Pockets, Free-Falls and Crashes: “Neither our stress-testing against Depression-era data, nor the adaptations we’ve made in response extreme yield-seeking speculation, do anything to diminish our conviction that historically reliable valuation measures are of immense importance to investors. Rather, the lessons to be drawn have to do with the criteria that distinguish periods where valuations have little near-term impact from periods where they suddenly matter with a vengeance. “The effect of valuations on subsequent market returns is conditional. While depressed valuations are a good indication of strong prospective long-term returns, depressed valuations don’t prevent further – sometimes massive – losses in the near-term. A retreat in valuation becomes reliably favorable mainly when it is joined with an early improvement in market internals. All of history (not just the Depression-era and the 2008-2009 collapse) imposes demanding requirements; not least that internals aren’t collapsing and credit spreads aren’t shooting higher, as they are today. Conversely, overvalued, overbought, overbullish extremes are associated with total market returns below risk-free interest rates, on average, but that average features an unpleasant skew: most of the week-to-week returns are actually positive, but the average is harmed by large, abrupt losses. Such extremes become reliably dangerous when they are joined by deterioration in market internals.” The speculative advance of recent years has not made the lessons of history irrelevant, but has only clarified that essential distinction: creating a mountain of default-free, zero-interest money can evidently defer the negative implications of overvalued, overbought, overbullish conditions, but only provided that credit spreads and the uniformity of market internals indicate a persistent willingness of investors to accept risk. Uniformly favorable market internals (where a broad range of individual stocks, industries, sectors, small caps, large caps, defensive stocks, speculative stocks, junk debt, and safe debt are advancing with little dispersion) are indicative of a general willingness of investors to accept risk – often completely regardless of the level of valuation, and in recent years, even regardless of the severity of overbought and overbullish conditions. Essentially, uniform market action and tame credit spreads are an indication that safe, low-interest liquidity is viewed as an inferior asset. In that environment, creating more liquidity provokes persistent yield-seeking speculation. In contrast – and to ignore this hard-won lesson may be begging for trouble – if credit spreads are widening and internal uniformity is deteriorating, one can infer that investors are shifting toward risk aversion. In that environment, safe, low-interest liquidity is no longer an inferior asset but a desirable one, and creating more of the stuff is not reliably supportive to risky asset prices. This is borne out across a century of history, including the 2000-2002 and 2007-2009 declines, and can be observed even in several episodes since 2009. The effect of quantitative easing is to extend and defer the consequences of reckless speculation, provided that low-risk liquidity is viewed as an inferior asset. Quantitative easing doesn’t eliminate the consequences of speculation and overvaluation, and in our judgment only promises to make the fallout more severe. But we should generally expect the worst consequences to emerge at those points when speculative, overvalued, overbought, overbullish conditions are joined by increased risk-aversion, as evidenced by widening credit spreads or subtle deterioration in the uniformity of market internals. Those shifts are clearly evident here, and our immediate concerns could hardly be more acute. An improvement in the behavior of credit spreads and market internals would significantly reduce the immediacy of our downside concerns, though it would not ease our longer-term concerns about valuation. Presently, market internals and credit spreads imply a measurable shift toward investor risk aversion – one that is likely, for now, to leave further monetary accommodation relatively ineffective in provoking fresh speculation aside from short-lived announcement effects – not that renewed easing would be a good idea in any event. This outlook will change only as valuations, credit spreads, and market internals shift.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |