|

|

||||||

|

|

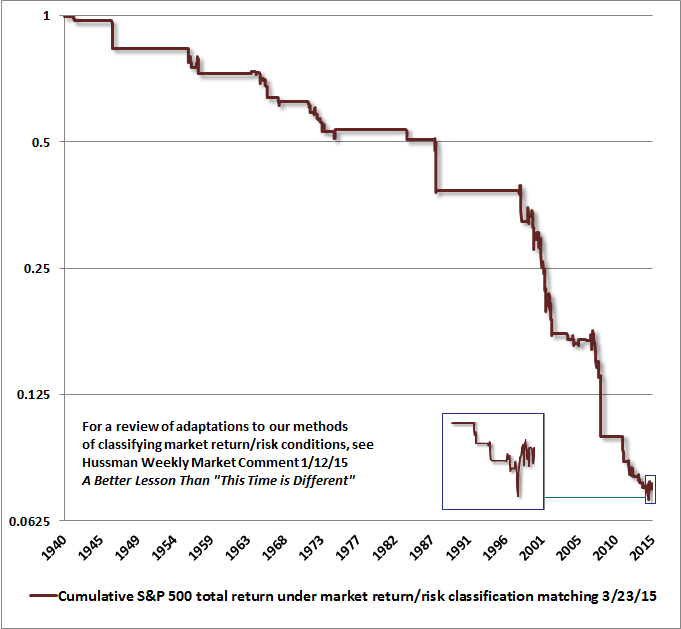

April 13, 2015 Valuation and Speculation: The Iron Laws There are two central considerations in investing that, when used in combination, have been the source of virtually every major success I’ve had in 30 years as a professional investor, and when inadvertently missed or underappreciated, have been the source of virtually every significant disappointment. The first is what I’ve often called the Iron Law of Valuation: every security is a claim on an expected stream of future cash flows, and given that expected stream of future cash flows, the current price of the security moves opposite to the expected future return on that security. The higher the price an investor pays for that expected stream of cash flows today, the lower the return that an investor should expect over the long-term. Particularly at market peaks, investors seem to believe that regardless of the extent of the preceding advance, future returns remain entirely unaffected. The repeated eagerness of investors to extrapolate returns and ignore the Iron Law of Valuation has been the source of the deepest losses in history (see Margins, Multiples, and the Iron Law of Valuation). The second consideration, however, is equally important over any horizon other than the long-term. It deserves its own name, and I’ll call it the Iron Law of Speculation: The near-term outcome of speculative, overvalued markets is conditional on investor preferences toward risk-seeking or risk-aversion, and those preferences can be largely inferred from observable market internals and credit spreads. In the long-term, investment outcomes are chiefly defined by valuations, but over the shorter-term, the difference between an overvalued market that becomes more overvalued, and an overvalued market that crashes, has little to do with the level of valuation and everything to do with investor risk preferences (see A Better Lesson than “This Time is Different”). If you have the long-term available to you, there’s nothing particularly wrong with being a value investor. Over the long-term, disciplined, historically-informed, value-conscious analysis pays off. But over shorter horizons, I promise from personal experience that it will periodically be the bane of your existence. I’ve learned that lesson twice: once during the late-1990’s valuation bubble, when I developed our methods of inferring risk preferences from market internals, credit spreads, and other risk-sensitive factors, and then again – as the inadvertent result of our awkward transition from our successful pre-2009 methods to our (hopefully equally or more successful) present methods of classifying market return/risk profiles. The simple fact is that the ensemble methods that came out of our 2009-2010 stress-testing against Depression-era data included all of those risk-sensitive measures, but not sufficiently to deal with a central bank bent on intentionally fomenting the third valuation bubble in 15 years. We ultimately imposed those bubble-tolerant considerations as an overlay to our methods in mid-2014. So if you genuinely want to learn something from our experience during the recent half-cycle, it’s not to discard the Iron Law of Valuation, but to couple your awareness of valuation with an understanding of where investor preferences toward risk are from the standpoint of the Iron Law of Speculation. I had very vocal concerns about valuation during the tech bubble and the housing bubble, well before they burst. But it was a specific combination: extreme valuation coupled with fresh deterioration in market internals – the same combination we observe presently – that provided us with timely evidence that market conditions had shifted to urgent risk at what in hindsight turned out to be the very beginning of the 2000-2002 and 2007-2009 collapses. Those collapses wiped out the entire total return of the S&P 500 - in excess of Treasury bills - all the way back to May 1996, and June 1995, respectively, despite aggressive Fed easing in both instances. Don't imagine that the current bubble will avoid a similar completion. At present, the S&P 500 is an average of 114% above the historical norms of the most reliable valuation measures we identify (and the importance of using historically reliable measures can't be overstated). Even this obscene overvaluation might not be of urgent concern, however, were it not for the fact that our measures of market internals and credit spreads also remain unfavorable at present – as they have been since late-June of last year (see Market Internals Suggest a Shift to Risk Aversion). Notably, the broad market – such as the NYSE Composite – has been in a low-volume sideways distribution pattern since then. In the absence of a jointly favorable shift in market internals and credit spreads, my impression is that the best characterization of market conditions at present is as a broad but possibly incomplete top formation, after a nearly diagonal half-cycle advance, and preceding a potentially violent retreat over the completion of this cycle. Investors may be confusing the challenges I’ve openly admitted and addressed with a license to ignore risk altogether. That’s a very, very bad idea – and draws the wrong lesson from our experience. Again, the correct lesson to draw is an appreciation of the Iron Law of Speculation: no matter how overvalued or overextended the market may be; no matter how deeply the market is likely to retrace that overvaluation over the eventual completion of the market cycle; the preferences of investors toward risk – as inferred from market internals, credit spreads and other risk-sensitive factors – can make that overvaluation largely irrelevant over shorter horizons. It may be necessary to have safety nets such as out-of-the-money put options or other defenses, but as Warren Buffett once remarked, “A group of lemmings looks like a pack of individualists compared with Wall Street when it gets a concept in its teeth.” As we observe conditions at present, market internals and credit spreads continue to suggest a subtle shift toward risk aversion. In that environment, awful outcomes occur more often than not. They may not happen immediately, but they tend to happen quickly. The late MIT economist Rudiger Dornbusch characterized the process well: “The crisis takes a much longer time coming than you think, and then it happens much faster than you would have thought.” About 8% of market history falls into the present set of market conditions (essentially characterized by extreme overvalued, overbought, overbullish conditions that are coupled with deterioration in market internals or credit spreads on our measures). Current conditions remain unchanged from a few weeks ago, so the following chart provides a good sense of our concerns here. The chart is on log scale, and the abrupt vertical drops that emerge in these conditions are often quite large in percentage terms.

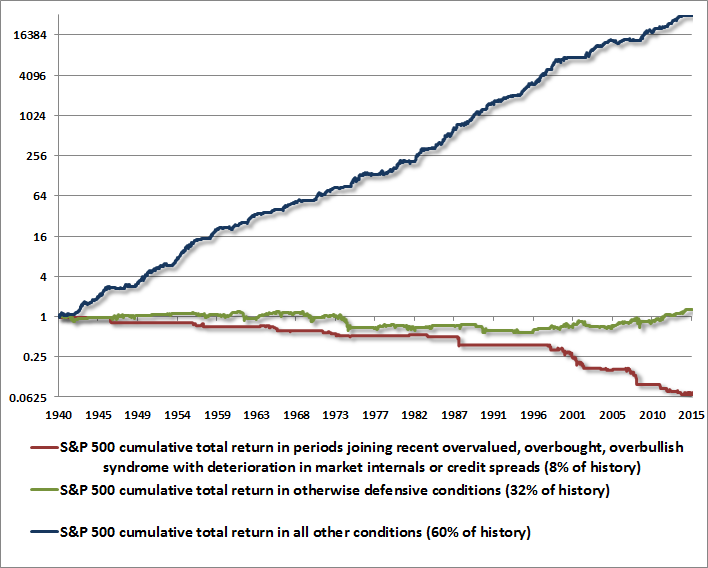

To the extent that air pockets, free-falls and crashes have reasonably identifiable commonalities, this 8% of history captures what we view as the essential features. The expanded chart below is more detailed, and also shows the cumulative total return of the S&P 500 in the 92% of market conditions outside of what we observe at present. That 92% can be (coarsely) broken down into two general bins. One set captures about 32% of historical conditions that we associate with a defensive outlook; not because of expected losses, but because of what might be called "unproductive volatility." This set features numerous bear market losses and severe drawdowns, but also periodic gains – usually in late-stage bull markets – sufficient to generate overall total returns above zero but below Treasury bill returns. The remaining 60% captures periods where our present methods would classify market conditions as constructive or even aggressively favorable.

I should note that these charts are not a depiction of an investment strategy, but simply partition market history according to observable conditions that we presently use to classify expected market return/risk profiles (primarily relating to valuations, market internals, sentiment, and other risk-sensitive measures). There’s no assurance that future market behavior will maintain this relationship with the estimated return/risk profiles that we infer. Still, if one believes that market outcomes are conditional on considerations such as valuation and investor risk preferences, we don’t know of a better set of measures to classify those conditions. Rules such as “don’t fight the Fed” are actually reliable only when one can also infer that investors are still in a risk-seeking mode (recall that the 2000-2002 and 2007-2009 plunges both occurred in an environment of persistent and aggressive Fed easing – see Following the Fed to 50% Flops). Trend-following rules can be very effective in reducing maximum drawdown, but the most popular ones – such as simple moving average strategies – also tend to sufficiently late or subject to whipsaws that incremental returns rarely survive trading costs (see The Trend is Your Fickle Friend). In any event, present conditions are not favorable (or even flat) on our measures, and despite week-to-week variation, the average outcome of present conditions has been wicked. In the event market internals and credit spreads improve, conditions will shift at minimum to those captured by the green line in the above chart. There’s no scope at these valuations for an aggressive outlook without a safety net, but the time for that sort of outlook will arrive as the present market cycle is completed. Indeed, conditions warranting a favorable market outlook have prevailed in the majority of market conditions we identify across history. Again, the lesson to be drawn from our own challenges during the recent half-cycle is not that the Iron Law of Valuation can be abandoned, but that the Iron Law of Speculation makes the near-term outcome of severe overvaluation conditional on the risk-preferences of investors (as inferred from observable market internals, credit spreads, and other risk-sensitive measures). I expect that the completion of the current market cycle will hammer that lesson home. How that completion unfolds will reflect both of the Iron Laws. At present, market conditions fall into 8% of history with the most negative return/risk profile we identify. A fresh shift to more risk-seeking investor preferences could allow for a less defensive outlook (along the lines of "constructive with a safety net"), while the strongest expected return/risk profile would result from a material improvement in valuations followed by a renewed shift toward investor risk-seeking. In our view, those more favorable conditions are worth waiting for, without abandoning the lessons of any of the Iron Laws. Updated Fund Notes and Commentary are posted this week. The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |