|

|

||||||

|

|

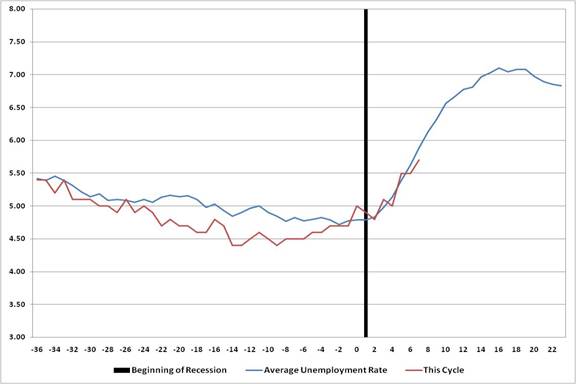

September 8, 2008 Deja Vu (Again) A few weeks ago, I observed that the stock market was again overbought in an unfavorable Market Climate, which is one of the few conditions when I ever have near-term expectations for the market (the other being oversold conditions in favorable Market Climates). The stock market's tumble last week was consistent with the type of abrupt weakness we typically observe from such conditions. Meanwhile, the weak labor report was in line with what we've seen recently in the elevated weekly jobless claims figures, and the surge in the unemployment rate to 6.1% is also consistent with what we would expect on the assumption that a U.S. recession began about January of this year. The chart below is from Bill Hester's recent piece - The Beginning of the Middle - the blue line being the "average" behavior of the unemployment rate centered around the beginning of recessions, and the red line being the unemployment rate in this cycle. Suffice it to say that we can expect the unemployment rate to move substantially higher over the coming 6-8 months.

Last week, the Mortgage Bankers Association reported a fresh surge in delinquencies and foreclosures during the second quarter, indicating that deterioration in the housing market is ongoing. A record 9.16% of U.S. mortgages were in delinquency (6.41%) or foreclosure (2.75%) as of June 30. This figure will likely be even worse in the third quarter report. The bright side, for what it's worth, is that I expect that we are currently in the heaviest period of this deterioration, and while that means a continued high foreclosure rate and mounting losses for financials over the next quarter or two, it also means that the the rate of change in this deterioration is presently near its peak. In short, we'll continue to see additional mortgage-related losses well into 2009 and even 2010, but I don't expect the rate of new foreclosures to continue accelerating beyond a few more months. To see why, I've reprinted the chart I presented in the April 14, 2008 comment - Which "Inning" of the Mortgage Crisis Are We In? Notice that the period from July through November represents the maximum slope of the cumulative reset curve (which I lagged by 180 days to get a profile of the likely foreclosure profile). After that inflection point later this year, losses may continue to mount, but the rate of losses and deterioration can be expected to flatten out significantly. Deja Vu (Again) Didn't we just "save the global financial system" a few months ago with the Bear Stearns transaction? Over the weekend, the Treasury announced that Fannie Mae and Freddie Mac will go into the conservatorship of the U.S. government. Unlike the Bear Stearns transaction, I don't have visceral objections to this transaction, because Fannie and Freddie's mortgage securities always had at least the implicit backing of the Federal government. But I'll tell you one thing - unless Congress mandates that mortgage originators will be partially on the hook in the event that future mortgages purchased by the government go into foreclosure, we're going to have a "moral hazard" problem of epic proportions. Without that provision, mortgage originators will be able to write bad mortgages and put U.S. taxpayers on the hook. In any event, you can be certain that this bailout will cost dramatically more than the "tens of billions" that press reports suggest. As I noted in July "it is reasonable to expect that at least 4% of the mortgages held or guaranteed by Fannie Mae and Freddie Mac will ultimately fail by 2009 (when the open-ended commitment of the government sunsets). Assuming a 50% recovery rate, which is about what banks are running on foreclosure recoveries lately, the losses on the retained mortgages and the guaranty books of Fannie and Freddie would already exceed $100 billion." Unfortunately, that $100 billion loss projection was based on the premise that the government's commitment would extend only until January 2009, so I only included in that 4% the mortgages already in foreclosure and just a portion of the delinquent ones. With that January 2009 "sunset" provision now gone, I expect that U.S. taxpayers will be on the hook for about $250 billion in losses. Look - 9.16% of U.S. mortgages are already delinquent or in foreclosure, with the likelihood of further delinquencies and foreclosures in the coming quarters. On a $5.2 trillion book of mortgage loans between Fannie and Freddie, and a prevailing recovery rate of 50% on foreclosed properties, an overall loss of about 5% of this book, or about $250 billion, is a fairly conservative expectation. It's likely that the market will take some initial comfort from this transaction, on the notion that the government has provided a "safety net" under the U.S. financial system. The problem with that interpretation, however, is that Fannie and Freddie always had the implicit backing of the government, and the government is now being forced to save these institutions because private investors have increasingly refused to provide additional capital. Unfortunately, what is true of Fannie and Freddie is most likely also true of other financial institutions that do not enjoy the implicit backing of the government. The prospect of a government bailout of those other institutions isn't at all clear. So by essentially capitulating that Fannie and Freddie have to be taken over, the government is also sending a signal that other financial institutions (particularly investment banks with high gross leverage multiples) may be vulnerable to failure. For that reason, any "knee jerk" enthusiasm about this transaction will probably be misplaced. With regard to the broader stock market, my impression is that investors still have not fully accepted or discounted what I view as the fact of recession. Unfortunately, credit spreads continue to widen, suggesting growing default risk beyond just the financial sector (the Moody's Baa/Aaa credit spread surged to a 25-year high last week), and job losses are increasingly spread broadly across industries. The level of economic discomfort certainly increased with Thursday's jump in jobless claims and Friday's weak employment report, but it was very noticeable that the selloff in the S&P 500 quickly halted at the same level as the closing low of the July decline. Investors appeared to believe (at least temporarily) that the prior closing low represented a good buying point. For my part, I'm neither compelled nor unduly distressed by current valuation levels. Though valuations (particularly on the basis of normalized earnings) are still richer than we typically observe at bear market lows, they are gradually improving. For that reason, if we can get some distance below the recent trading range on legitimate recession, profit and credit concerns, we may have the opportunity to establish some amount of market exposure at those lower levels, with a reasonable expectation of recovering toward current levels on a subsequent recovery. In other words, we aren't inclined to accept market exposure at present, because the outlook for a sustained advance from this starting point isn't particularly strong. But we would be inclined to gradually increase our market exposure some distance below these levels, because a recovery back to this area (say, in a bear market rally or eventual bull market) might then be reasonable or even likely. Even with unfavorable economic and credit conditions, we will remain alert to potential opportunities to establish a constructive investment stance as this market downturn runs its course, particularly once we are provided a sufficient margin of safety from valuations (or at least constructive market internals). Ideally, the present bear market decline will end at a much better valuation trough than the 2000-2002 bear market established. One of the reasons that the initial portion of a bull market produces such powerful returns is that new bull markets have historically taken the normalized price/earnings ratio on the S&P 500 from deeply depressed levels back toward "known values." Bear markets have regularly troughed below 11 times prior peak earnings, with an average closer to 9 times prior peak earnings, and sometimes below a P/E of 7, as we saw in 1974 and 1982. By contrast, the 2002 bear market low was established at a much higher multiple (about 15), which is why the most recent bull market produced only one annual gain exceeding 20% for the S&P 500, with relatively tepid returns over the complete cycle (the 5-year total return on the S&P 500 is currently just under 6% annually). Currently, the S&P 500 is trading at about 15 times prior peak earnings, but that multiple is somewhat misleading because those prior peak earnings reflected extremely elevated profit margins on a historical basis. On normalized profit margins, the market's current valuation remains well above the level established at any prior bear market low, including 2002 (in fact, it is closer to levels established at most historical bull market peaks). Based on our standard methodology, the S&P 500 Index is priced to deliver expected total returns over the coming decade in the range of 4-6% annually, with an expected annual total return as high as 9% if the decade ends with valuations near their historical extremes, and as low as 0% if the decade ends with valuations near their historical troughs. As always, no forecasts are required, and we'll take our evidence as it arrives. Either a strong reversal in market internals, or a move to more favorable valuations, would provide a basis for accepting some amount of market risk. For now, we remain defensive and well-hedged. Market Climate As of last week, the Market Climate for stocks remained characterized by unfavorable valuations and unfavorable market action, holding the Strategic Growth Fund to a fully hedged investment stance. The recent selloff has certainly compressed short-term technical conditions enough to allow for a "fast, furious, prone-to -failure" rally, but again, there is nothing in the government's takeover of Fannie Mae and Freddie Mac that changes the fundamental state of the economy. If anything, it is a negative signal about solvency problems, which - if credit spreads are any indication - will shortly begin emerging in other financials with high gross leverage ratios (high multiples of total assets to shareholder equity). In bonds, the Market Climate was characterized last week by modestly unfavorable yield levels and relatively neutral yield pressures. The Strategic Total Return Fund continues to have a duration of about 2.5 years, primarily in Treasury securities, with just under 20% of assets in foreign currencies. In response to the recent weakness in utility stocks, we have started "nibbling" on shares, placing about 5% of assets in this sector. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |