|

|

||||||

|

|

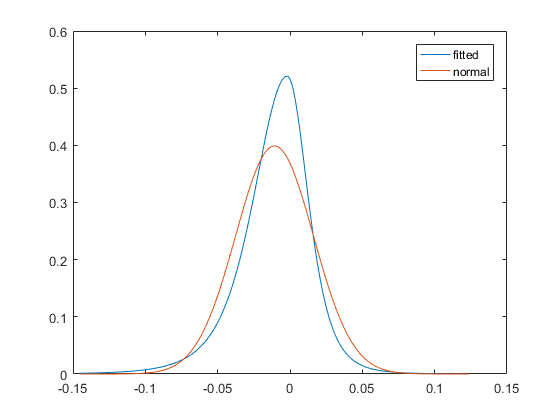

December 5, 2016 Complacency and the Fat Left Tail The present combination of overvalued, overbought, overbullish conditions, coupled with rising interest rates and broad dispersion among market internals, is one that most closely resembles only three other points in the post-war period; the first in early-October 1987 (though at less extreme valuations), the second in January 2000, and the most recent in July 2015 (the S&P 500 lost -12% over the next 6 weeks). Relaxing the set to include the nearly 10% of post-war periods that share the more general market return/risk classification we presently identify, the overall expected return distribution is associated with severely negative market outcomes, on average, capturing a cumulative loss in the S&P 500 exceeding -90%. We currently view a hard-defensive stock market outlook as appropriate. Even in bonds and precious metals, present market conditions are consistent with only modest return expectations. While a near-term rebound in these markets would be consistent with short-term oversold conditions, our main inclination in response to the recent spike in yields is not so much to embrace Treasury debt but to avoid corporate debt, where credit spreads are compressed to the point where rapid adjustments (and steep price losses) appear likely. I have very weak expectations about direction of long-term interest rates here, but much stronger views about the likelihood of widening credit spreads. Notably, the implied bell curve of expected stock market returns features what I’ve often called “unpleasant skew.” The chart below shows the fitted probability distribution of weekly market returns under the market return/risk classification we presently identify (blue), compared to a symmetrical distribution centered at the same mean return (red). Notice that in any given week, the single most likely market outcome is actually a small gain, even though the average outcome is negative (near -40% at an annual rate). Notice also that the right tail of the blue curve is narrow, implying a much smaller-than-average probability of a significant market gain, while the left tail is fat, implying a larger-than-average probability of a vertical market loss.

Simply put, don’t be lulled into complacency by thinking that severely hostile market conditions have to resolve into immediate market losses. That’s not the way these environments work, and they never have. Rather, the “unpleasant skew” of present conditions actually means that investors should expect a greater tendency toward small market gains than market conditions might otherwise lead them to expect, punctuated - with no warning at all - by wicked vertical losses that wipe out weeks or months of market gains in handful of sessions. Every market crash in history has been associated with essentially the same skewed distribution. It’s the positive “mode” that creates complacency, it’s the negative average return that drives cumulative losses, and it’s the fat left tail that strikes out of nowhere. Meanwhile, it’s best not to focus one’s investment horizon on days or weeks, but rather, on the complete market cycle and the longer horizon in the range of 10-12 years. While we’ve adopted a defensive market outlook here, and we expect a 40-55% market loss over the completion of the current market cycle, with 10-12 year S&P 500 total returns barely above zero, we’re also open to the potential for shorter-term shifts in investor risk-seeking that could modify our near-term outlook. I expect that a strong safety-net will be required until we observe a material retreat in valuations, but we’re open to changes in the evidence from week-to-week and will align ourselves accordingly. Internal dispersion widens As I regularly emphasize, valuations are the primary driver of long-term and full-cycle market returns, while outcomes over shorter segments of the complete market cycle are driven instead by the preferences of investors toward risk-seeking or risk-aversion. Since risk-seeking speculation tends to be indiscriminate, the most reliable measure of these risk-preferences we’ve found is the uniformity or divergence of market internals across a broad range of individual stocks, industries, sectors, and security types, including debt securities of varying credit quality. It’s on that front that we have to remain flexible. I’m always the first to note that my insistence on stress-testing our market return/risk classification methods against Depression-era data in 2009 bared an Achilles Heel that made the subsequent half-cycle difficult on us, largely as a result of quantitative easing. We addressed the key issue in mid-2014 (see the Box in The Next Big Short for the full narrative). Since then, the market has been locked in a sideways two-year top-formation with deteriorating internals. That’s made it challenging for risk-managed investment disciplines to get traction. Still, don’t imagine that the completion of this cycle will come with lesser vengeance than the cycle completions that have attended similar valuation extremes across history. Presently, we observe wide internal market dispersion, including weakness among interest-sensitive securities, tepid uniformity across developed markets, and an abrupt whack to technology stocks last week. The combination of a steeply overvalued, overbought, overbullish market with hostile yield trends and divergent internals is not one we take lightly. It’s that combination that has most often been associated not only with emerging bear markets but with market crashes. The nature of unpleasant skew is that while our overall market expectations are negative, we have to expect a tendency toward small net advances in any given week, while at the same time being prepared for vertical tail-risk to the downside. This may be a process of weeks, or months, or of periods where investor preferences shift intermittently between risk-seeking and risk-aversion. So we’ll align our outlook as the evidence changes. Our confidence isn’t invested in the outcome of any given week, but in the expectations we have for our investment discipline over the complete market cycle, and in the average outcomes of the market conditions we identify at each point in time. That’s important to understand, because having confidence in the average outcome of repeated instances is quite different from having confidence about the outcome of any specific instance. Even here, we’ll soften our near-term view if the overall character of market action improves. For now, our market view remains hard-negative.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |