|

|

||||||

|

|

February 13, 2017 Time-Stamp of Speculative Euphoria If there’s any point in U.S. stock market history, next to the market peaks of 1929 and 2000, that has deserved a time-stamp of speculative euphoria that will be bewildering in hindsight, now is that moment. Perhaps there’s room for this burning wick to shorten further, but across every effective, value-conscious, historically-informed classification method we use, the estimated downside risk of the market overwhelms its upside potential. The chart below shows monthly candlesticks for the S&P 500 Index since 1996, including the tech bubble and collapse, the Fed-induced mortgage bubble and collapse, and the speculative first half of the current, wholly uncompleted cycle. I believe the equity market now faces the likelihood of deeper losses over the completion of this cycle than any other in history, save for the collapse that followed the 1929 peak.

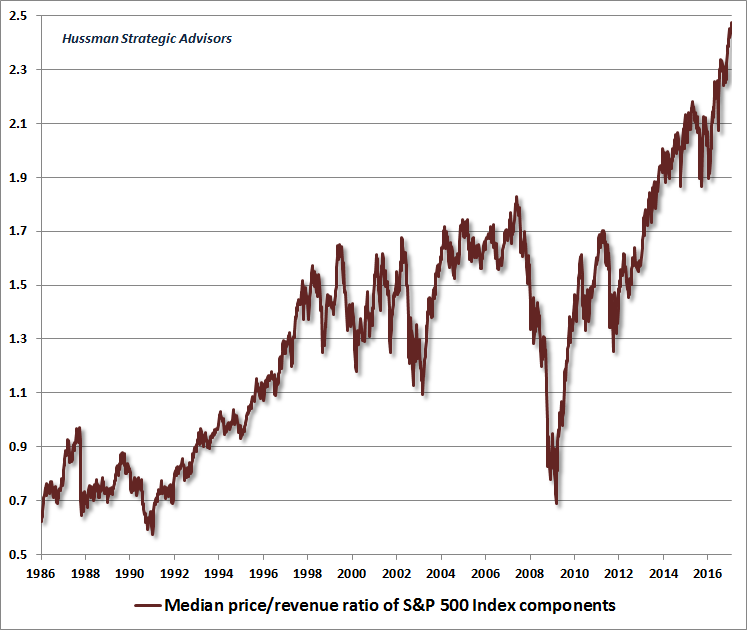

The post-election advance has taken the S&P 500 Index nearly 9% above its May 2015 high, yet internal divergences have persisted, particularly among interest sensitive sectors and security-types, along with other features such as deteriorating price/volume characteristics, leadership, and participation on new highs. I continue to view the recent advance as more consistent with a transient speculative blowoff than a durable breakout in market action. Even before the election, steep market losses over the completion of this cycle were already likely, as a consequence of obscene overvaluation baked in the cake by years of yield-seeking speculation. The election outcome only added a caboose to the back of a freight train already headed toward that cliff. The difference between value-conscious investors and speculators is that when they encounter a sign that says “Warning! Dynamite” and see a lit wick at their feet, every inch the wick shortens is a signal for the value investor to step further away. The speculator instead moves closer, taking the delayed consequences as evidence that it’s different this time, and the sign is wrong. There have certainly been longer and shorter wicks, but ultimately, the consequences have always arrived. On valuations, earnings, and taxes We can’t be certain that current extremes won’t be eclipsed, as higher valuations were observed for nearly three months approaching the March 2000 market peak (based on measures that have the strongest correlation with actual subsequent returns in market cycles across history). Still, we don’t encourage relying on that as a target. The 2000 bubble peak was dominated by a subset of large-capitalization technology stocks that were breathtakingly overvalued, while median valuations across all components of the S&P 500 were less extreme. See Sizing Up the Bubble for a reminder of those skewed valuations. Last week, one of the self-fashioned carnival barkers of financial television compared the 5 stocks with the largest market capitalizations at the height of the tech bubble with the 5 largest stocks today, “to prove once and for all” that the market is not overvalued. This conflates an argument about valuation skew with an argument about valuation levels. The fact is that the present speculative episode features what are already the most extreme median stock valuations in history. Indeed, even the richest two deciles of the S&P 500 are more extreme than those same two deciles were outside of any point in history other than the year 2000 itself. The chart below begins in 1986, when market valuations were fairly close to the pre-bubble norm of 0.8 for the S&P 500 price/revenue ratio. Even if market valuations never fall below historical norms again, the current speculative episode is likely to end badly.

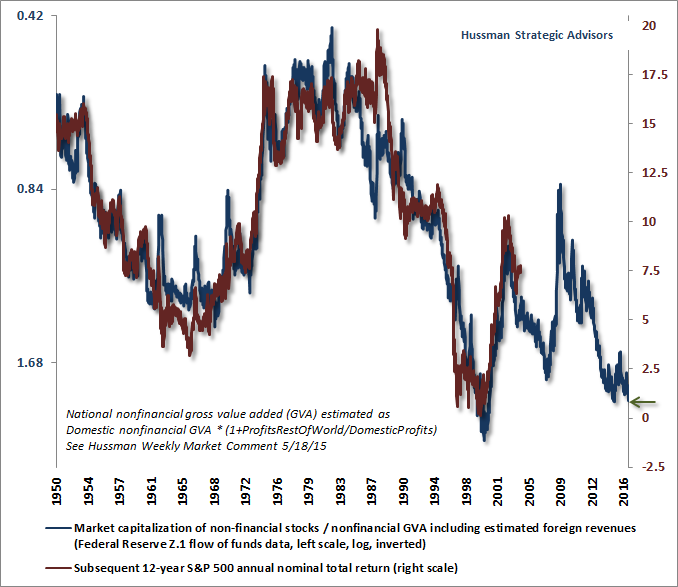

The late-1990’s bubble focused the greatest distortion on technology and internet stocks, and was followed by a -50% loss in the S&P 500 and an -83% collapse in the tech-heavy Nasdaq 100. The next bubble into 2007 was broader, but was still dominated by financial and mortgage-related speculation. That bubble was followed by a 55% loss in the S&P 500 during the global financial crisis. The current bubble has been driven by years of Fed-induced yield-seeking speculation, and has infected risk assets from global debt, to junk bonds, to every corner of the equity market. My friend Jesse Felder of The Felder Report appropriately calls this the “everything bubble.” The chart below shows the ratio of nonfinancial market capitalization to corporate gross value-added (MarketCap/GVA), which we find to be better correlated with actual subsequent market returns across history (and even in recent market cycles) than numerous popular measures including price/earnings, price/forward operating earnings, the Fed Model, Tobin’s Q, the Shiller cyclically-adjusted P/E, and even Warren Buffett’s old favorite, market capitalization/GDP. MarketCap/GVA is shown on an inverted log scale (blue line, left scale) along with the actual subsequent S&P 500 average annual nominal total return over the following 12-year period (red line, right scale). At present, our estimate based on this and other reliable measures is that the S&P 500 is likely to scratch out a barely positive total return between now and 2029, with all of that gain coming from dividends, leaving the S&P 500 Index itself lower at that date than it is today. That shouldn’t be a terribly surprising statement. The S&P 500 didn’t durably break its March 24, 2000 high of 1527.46 until March 5, 2013. I expect the completion of the current cycle will not only revisit that level on the S&P 500, but that it will also wipe out the entire total return of the S&P 500 since 2000. Those are the long-term consequences of extreme overvaluation, and they have been throughout history.

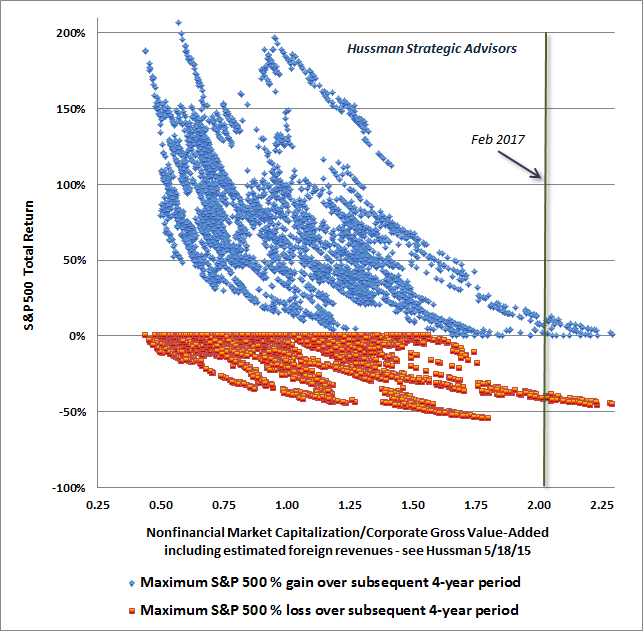

Remember that the S&P 500 registered negative total returns for a buy-and-hold strategy for the nearly 12-year period from March 2000 all the way to November 2011. I expect that’s about what we’ll observe from current extremes. While investors seem eager to lock themselves into passive strategies that have performed well in the rear-view mirror of this climb to obscene valuations, I expect the greatest asset to investors in the coming decade will be adherence to a flexible approach that reduces risk in response to extreme valuation and divergent market action, and embraces risk in response to material retreats in valuation that are coupled with early improvements in the uniformity of market action. As I noted last week, my view is that passive, value-insensitive investment strategies are at the beginning of another long winter, while value-conscious, risk-managed, full-cycle investment disciplines are approaching the first day of spring. It’s notable that Wall Street continues to rely on earnings-based measures that have demonstrably poor correlations with subsequent market returns, relative to other readily available measures. As I’ve detailed previously in data across history, every earnings-based measure must be considered hand-in-hand with the profit margin embedded in those earnings (see Margins, Multiples, and the Iron Law of Valuation). Though earnings are certainly necessary to generate long-term cash flows that can be delivered to investors over time, year-to-year earnings figures are very poor “sufficient statistics” for that long-term stream of cash flows, because of fluctuations in profit margins over the economic cycle, and competition in the markets for output and labor, which has the effect of normalizing after-tax profit margins over longer horizons. These historical relationships between valuations, earnings, margins, and investment returns have several implications. First, Robert Shiller’s “cyclically adjusted P/E” or “CAPE” (S&P 500 divided by the 10-year average of inflation-adjusted earnings) was at 43.5 at the March 2000 peak. By contrast, the current CAPE of 27.4, though higher than the multiple seen at any pre-bubble market peak except 1929, still seems much less extreme. The problem with that simple comparison is that in 2000, the embedded profit margin (the denominator of the CAPE divided by S&P 500 revenues) was just 5.1%, below the historical norm of 5.4%. Presently, the embedded profit margin is 7.4%. Put another way, on the basis of normalized profit margins, the CAPE in 2000 would have peaked at 41.1, which is less than 10% from the adjusted level of 37.7 that would prevail today on normalized margins. As I showed in my May 5, 2014 comment, adjusting the CAPE based on the embedded profit margin improves its historical reliability (as measured by its correlation with actual subsequent market returns). Prior to the late-1990’s bubble, the highest raw CAPE ever observed was about 31.0 at the 1929 top. That’s slightly above the current raw multiple of 27.4, but below the current normalized CAPE of 37.5. I expect that the 1929 multiple would likely have been higher on the basis of normalized profit margins. We don’t have revenue data to estimate the embedded margin at the time, but a variety of alternative, historically reliable measures place current valuations at roughly the same levels as the 1929 peak. Changes in tax policy are unlikely to alter matters much. Investors should recognize that effective corporate tax rates (actual taxes paid/pre-tax income) have already declined from 50% in the 1950’s to less than half that level at present. Even if the effective corporate tax rate was suddenly and permanently cut in half, the incremental long-term boost to the level of corporate profits, from here, would be hardly 10%. Our view is that the U.S. equity market currently prices in all of the potential benefit, and none of the prospective instability, that the current administration is likely to introduce. In the face of what I view as legitimate concern about the disquietingly incivil, disruptive, and autocratic mode of leadership adopted by the new administration (see On Governance for my views on this subject), Wall Street has shown little concern for social or economic risks, focusing only on whatever gains might be available from shifting the costs and externalities of corporate behavior onto the public and the environment through deregulation, and tax reforms that thus far appear more fixed on lowering corporate rates than on creating meaningful incentives for productive investment. I’m reminded of a story that Art Cashin shared at dinner a few years ago. There was a presentation on Wall Street focused on a growing trend of heroin addiction. Summarizing the attitude of the audience, one of the traders shouted out, “Who makes the needles?” As for sentiment, the S&P 500 has advanced by less than 2% since mid-December, but since even the most incremental gains represent fresh highs, the advance feels almost unshakeable and relentless. Bullish sentiment among investment advisors surged last week to 62.7%, while bears plunged to just 16.7% (Investors Intelligence). The resulting bull-bear spread is among the widest 4% in history. That said, I’ve often noted that sentiment, in and of itself, isn’t a particularly reliable indicator, since it can also become lopsided relatively early into steep market advances and declines outside of major turning points. For that reason, we typically use sentiment only as part of broader syndromes of extreme conditions. In recent weeks, I’ve noted that we’ve observed the most extreme syndromes of overvalued, overbought, overbullish conditions that we define. Outside of a single set of instances between late-2013 and early-2014, at the height of zero-interest rate enthusiasm about the Fed’s zero-interest rate policy, every other prior instance has been associated with a major market peak, including 1929, 1972, 1987, 2000, 2007. We also observe a rare set of event-related “signatures” that capture broad market conditions that have typically preceded near-vertical market losses on a variety of horizons. For the record, the current level of 62.7% bulls, 16.7% bears compares to other major market peaks in recent decades as follows: October 2007: 60.2% bulls, 21.5% bears; March 2000: 55.7% bulls, 26.4% bears; August 1987: 60.8% bulls, 19.2% bears. Arc of the Pendulum One of the central lessons of history is that while investors may be distracted by optimistic themes and shiny objects over shorter segments of the market cycle, valuations are the principal driver of longer-term investment returns over horizons of 10-12 years, and are the key determinant of the extent of downside losses over the completion of any given market cycle. Imagine a pendulum that swings between one extreme on the left and another on the right. At any point along the arc of the pendulum, we can measure two distances. We’ll call the “potential gain” the distance from the current position all the way to the right extreme. We’ll call the “potential loss” the distance from the current position all the way to the left extreme. If the pendulum has swung all the way to the left, there is initially a huge potential gain, which gradually drops to zero as it swings to the right extreme. Similarly, the potential loss starts at zero when the pendulum is all the way to the left, and becomes extremely negative once the pendulum reaches the right extreme. So, if we were to draw a chart of both potential gain and potential loss, the two curves would swoop downward as the pendulum moves from left to right. If the pendulum could trace out the exact same path each time, we’d just get two curves. But if there was some amount of variation from swing to swing, we’d trace out a whole set of arcs, packed close to one another but not perfectly overlapping. As it happens, our pendulum is a reasonable analogy for how valuations and potential gains and losses are related in the financial markets. Last week, I constructed the following chart in response to a question about the relationship between valuations and drawdowns (h/t Aaron Brask). On the horizontal axis I’ve plotted the ratio of MarketCap/GVA in weekly data since 1948. On the vertical axis, there are two series. The blue dots (weekly) show the maximum total return experienced by the S&P 500 over the subsequent 4-year period, measured from the prevailing level of the S&P 500 at the time (regardless of whether the maximum gain was recorded say, 1 year later, or 3 years later, or at the very end of the 4-year period). Likewise, the red dots show the maximum loss experienced by the S&P 500 at any point over the subsequent 4-year period, measured from the prevailing level of the S&P 500 at the time.

You can think of those sweeping dots as tracing out different market cycles; different arcs of the pendulum. The most extreme swing ended in March 2000, at a MarketCap/GVA multiple of 2.3. The present level of 2.0 is shown by the green bar. I could show a similar chart using MarketCap/GDP going back to the Great Depression, but the overall plot looks the same, and it would just be well, greatly depressing, because in that case, valuations similar to the present were followed by a maximum loss in the Dow Jones Industrial Average of -89% by mid-1932. Suffice it to say that we expect current valuation extremes to represent one of the most extreme arcs of the pendulum in U.S. history, and we associate this extreme with extraordinarily weak prospects for further returns (and even weaker prospects still for durable returns). As for prospective losses, we continue to expect a collapse in the S&P 500 in the range of 50-60% over the completion of the current market cycle, which would actually only bring the most reliable measures of valuation to historically run-of-the-mill norms. My sense is that these estimates of prospective loss seem as preposterous as those I correctly projected at the 2000 and 2007 peaks. Even for those familiar with our record in complete market cycles prior to 2009, it’s tempting to discard my concerns in this half-cycle because of the inadvertent challenges that followed my 2009 insistence on stress-testing our methods against Depression-era data, after a collapse we fully anticipated (see Portfolio Strategy and the Iron Laws for that narrative). I’ve openly detailed the Achilles Heel that resulted, and how we adapted in response, but those adaptations don’t remove our defensiveness in what are essentially the same conditions that allowed us to anticipate the 2000-2002 and 2007-2009 collapses. Despite the “permabear” label, the fact is that I’ve also encouraged a constructive or even leveraged market outlook after every bear market decline in more than three decades as a professional investor (though our late-October 2008 shift, following an expected collapse of more than -40% in the S&P 500, was truncated by that 2009 stress-testing decision). Still, I have no intention of convincing investors of anything that they prefer to reject. Since every share of stock outstanding will have to be held by someone over the completion of this cycle, it’s impossible for investors to reduce their risk in aggregate anyway. In any event, I’ll have the comfort of knowing that I’ve shared my truth. We know how this works, because we’ve seen it in real-time before. When the market begins to lose several percent of its value by the day (and I believe it will), I suspect that investors will wonder why they were so profoundly eager to chase potential gains that had little chance of being durable or worth the risk, and why they were so profoundly averse to accepting the risk of small losses in defensive positions that could have ultimately prevented or reversed their misfortune. For our part, we’ll continue to align our outlook with new evidence that arrives at each point in time, particularly relating to valuations and market action. On that front, even recent highs have not reversed the dispersion we observe across market internals, the most obvious being among interest-sensitive sectors. Here and now, our estimated return/risk classifications remain sharply negative, and we observe a preponderance of risk signatures that we associate with steep losses or sharp interim drawdowns on nearly every horizon beyond a few weeks.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |