|

|

||||||

|

|

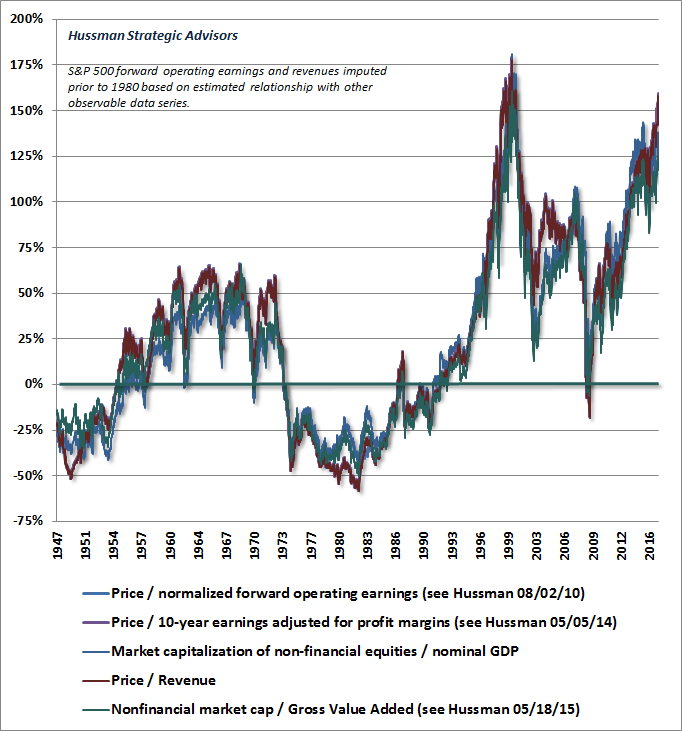

February 20, 2017 When Speculators Prosper Through Ignorance “No Congress of the United States ever assembled, on surveying the State of the Union, has met with a more pleasant prospect than that which appears at the present time.” “There can be little argument that the American economy as it stands at the beginning of a new century has never exhibited so remarkable a prosperity for at least the majority of Americans.” “We believe the effect of the troubles in the subprime sector on the broader housing market will be limited and we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system.” “Investors haven’t been this optimistic on the global economy since 2011... A full 23 percent of investors expect an outright ‘boom,’ according to a survey released Tuesday by Bank of America Merrill Lynch... ‘The U.S. economy is not only humming on all cylinders, but in our view the optimism associated with a clean sweep by the Republicans in Washington is likely to create a self-fulfilling period of strong markets and at least the potential for strong growth.’ The optimism comes amid forecasts global growth will pick up and as Donald Trump promises to cut taxes, boost fiscal spending and loosen regulations in moves that could boost corporate earnings. ‘Macro optimism is surging,’ wrote the team.” The relationship between the economy and the stock market is a study in contradiction. It’s precisely when economic optimism is strongest, when caution is seen as misguided, and when bullish enthusiasm is most exuberant, that the stock market reaches its speculative apex and becomes most vulnerable to collapse. It’s precisely when economic pessimism is most dismal, when hope is set aside, and when bearish consensus is most dire, that market plumbs its deepest lows and carries the greatest potential for future returns. If you think about the market as an equilibrium where every purchase has to be matched with a corresponding sale, this apparent contradiction vanishes. See, it’s precisely the untethered bullish enthusiasm of buyers, and the corresponding reluctance of sellers to part with their shares, that generates extreme overvaluation. Offensive valuation extremes could emerge no other way. Likewise, it’s precisely the wide-eyed fear of sellers, and the corresponding reluctance of buyers to absorb new shares, that generates extreme undervaluation. Understanding this, it’s essential to resist the popular but misinformed impulse to believe that economic optimism itself is a useful or valid basis on which to invest in securities. What’s required instead is an insistence on recognizing that the long-term total returns that investors actually achieve from their investments are tightly linked to the valuations that they pay. As we’ve detailed in scores of prior commentaries, the most reliable market valuation measures we’ve identified have correlations of 90-94% with subsequent S&P 500 10-12 year total returns. The chart below updates several of these measures as of last week. We continue to view recent market action as the likely final blowoff of one of the most extreme speculative episodes in U.S. history. The valuation measures we identify as most tightly correlated with actual subsequent S&P 500 total returns in market cycles across history range about 160% above (2.6 times) their historical norms, and more than 5 times the levels observed at points of secular undervaluation such as 1949 and 1982. This implies that a rather run-of-the-mill retreat to historical norms would now be associated with an expected market loss of about -60%, while a retreat even to a level still 25% above historical norms would be associated with a market loss exceeding -50%. That range of prospective market losses between -50% and -60% is in fact our expectation over the completion of the current market cycle, and neither would take reliable equity valuations below their long-term historical norms.

Of course, several popular and unreliable valuation measures are less extreme, but those measures also have generally weak correlations with subsequent market returns, invariably because they ignore the tendency of profit margins to fluctuate over the economic cycle. Investors should be particularly attentive to the fact that the median component of the S&P 500 is now far more overvalued than in 2000, 2007, or indeed in any prior point in history, and unlike 2000, small-capitalization indices are also breathtakingly overextended. As Benjamin Graham warned, “Observation over many years has taught us that the chief losses to investors come from the purchase of low-quality securities at times of good business conditions. The purchasers view the good current earnings as equivalent to ‘earning power’ and assume that prosperity is equivalent to safety.” Presently, we estimate that the nominal total returns of the S&P 500 Index are likely to average less than 1% annually over the coming 12-year horizon. Since that estimated return is positive only because of expected dividend income, we project that the S&P 500 Index itself is likely to be 10-20% lower than its present level 10-12 years from today. That outcome would be quite similar to what we accurately anticipated, and observed, following the valuation extremes in 2000. From a valuation standpoint, a 12-year total return estimate of less than 1% annually implies that it would take a further advance of less than 12% in the S&P 500 (over and above nominal economic growth of about 4% at an annual rate) to drive the our estimate of prospective 12-year total returns to zero, with any further market advance driving 12-year prospects into negative territory. Such an advance would bring the most reliable measures we identify to the same hypervaluation we observed at the 2000 extreme (we presently estimate that valuations have already eclipsed the 1929 extreme). We can’t rule that out, but we would expect any further gains to be wiped out as quickly as they were in the 2000 instance. As Benjamin Graham observed decades ago, "Speculators often prosper through ignorance; it is a cliche that in a roaring bull market, knowledge is superfluous and experience is a handicap. But the typical experience of the speculator is one of temporary profit and ultimate loss." I’ve often emphasized that valuation in itself is a rather poor measure of near-term return prospects. Instead, the primary driver of market returns over shorter segments of the market cycle is the preference of investors toward risk-seeking or risk-aversion. The best measure we’ve found of investor risk-preferences is the uniformity or divergence of market action across a wide range of individual stocks, industries, sectors, and security types. When investors are strongly inclined to speculate, they tend to be indiscriminate about it. Our inferences aren’t based on a single measure like the advance-decline line or some moving average or another, but instead on a much broader signal extraction which remains unfavorable here. As a side note, investors who are willing to dismiss our valuation concerns based on our own challenges in the recent advancing half-cycle are leaving themselves terribly vulnerable. Those same valuation methods properly identified stocks as undervalued in 2009. The real issue was that my 2009 insistence on stress-testing our market return/risk classification methods against Depression-era data, following a collapse we fully anticipated, inadvertently created an Achilles Heel in the face of zero interest rate policy. Despite our admirable record in previous complete market cycles, that stress-testing led us to overemphasize “overvalued, overbought, overbullish” features of market action and to inadequately prioritize market internals. We introduced adaptations to address this in mid-2014. See Portfolio Strategy and the Iron Laws for a further discussion. Presently, interest-sensitive sectors exhibit the clearest divergences, but we also observe divergences across numerous measures of breadth, leadership, and participation that remain more consistent with a speculative blowoff than a period of robust sponsorship or risk-seeking among investors. That may change, but given current overvalued, overbought, overbullish extremes and Fed policy that has moved off the zero bound, the likely consequence of improved market internals would be a shift to a neutral outlook from our current hard-negative outlook. A more constructive outlook would require an abatement of overvalued, overbought, overbullish extremes coupled with constructive market internals. I have no question we’ll see strong opportunities on that basis over time. But the impatience for bullish opportunity, when none presents itself, will be responsible for a great deal of disappointment over the completion of this cycle. On alternative investment strategies Finally, two brief comments about what we view as the current top formation of this speculative market cycle. Since about mid-2014, many value-conscious stock-selection approaches we track, including those we’ve found most effective over time, have moderately lagged the capitalization-weighted indices. This broad tendency for active portfolios to lag the major indices has encouraged a clear shift among investors toward passive investment strategies. This pattern has also been challenging for hedge funds and hedged-equity strategies, which hedge diversified long portfolios with short positions in the major indices. We saw the same thing during the 2000 top formation, and approaching the 2007 peak, when I observed that the performance of value-conscious stock selection strategies is typically the least impressive just when the market itself is approaching a long period of dull and often negative returns. In general, active strategies compare poorly with their passive peers when the passive indices themselves are at bull market highs. The pattern then tends to reverse in declining markets. Suffice it to repeat that we view the recent shift of investors toward passive, price-insensitive investment strategies as a form of late-stage performance chasing. While that has uncomfortable short-term effects for value-conscious investors, particularly across hedged strategies, that behavior has historically set up the very opportunities that disciplined long-term investors rely on. Second, while our own discipline doesn’t contemplate pure short sales in the equity market, I should observe that across all investment strategies we monitor, we presently expect short positions in the major U.S. equity indices to be associated with stronger prospective returns over the coming 2-year period than virtually any other investment class. Again, pure short sales are outside of our own discipline, but it’s still a point worth noting. It’s often argued that a short sale is associated with a maximum gain of 100% yet faces unlimited risk. In fact, however, this assumes a wholly static investment position, rather than one that rebalances as the market fluctuates. Now, I certainly can’t imagine how any investor could contemplate a short sale of a single stock, because the risk of abrupt, discontinuous, and devastating price jumps is significant. But as a short portfolio becomes more diversified, it also becomes better behaved. If the short position is rebalanced as the underlying security fluctuates, the return/risk profile changes substantially. See, in a randomly fluctuating market (without enormous price leaps) where the short position is continuously rebalanced to the value of the account itself, the cumulative value of a short position will, to a close approximation, track the reciprocal of the cumulative value of a long position in the market. That is, if the market falls in half, a regularly rebalanced short position will tend to double in value (particularly when one takes account of interest on the short sale proceeds). Conversely, if the market doubles, the short position will tend to lose half of its value. Mathematically, if X is the cumulative value of the index position (e.g. starting at 1.0 and increasing or decreasing proportionally with the index total return), a regularly rebalanced short position with N times leverage will evolve as (1/X)^N, but that evolution becomes unstable at very high multiples of leverage, because of the potential for a series of large, adverse moves to disrupt or wipe out the position entirely. You can demonstrate this to yourself with historical or simulated data. Indeed, a regularly rebalanced short position on the S&P 500 would have roughly doubled during both the 2000-2002 and 2007-2009 declines, and would have outperformed a long position in the S&P 500 itself from the March 2000 peak all the way out to January 2012. Once market valuations become extreme, short index positions represent a perfectly valid alternative asset class for investors who take a full-cycle perspective toward investing. The reason they are underused, even in hypervalued markets, is because of a herd-following anomaly of temperament among investors, which allows them to tolerate losses that occur when other investors are also losing, but to practically burst a vein if those losses occur in periods when other investors are gaining. Those investors often abandon their positions at the worst possible point in the market cycle, and it may be best for them to avoid alternative investments entirely. The main objective can then be simply to align their exposure to various long investments according to their risk-tolerance and investment horizon. My own view is that diversified short portfolios or short index positions are best used to hedge diversified long portfolios in periods of historically unfavorable market conditions, and to establish limited inverse exposures during extremely hostile conditions. I certainly think that long-short strategies are better suited to the present market environment than those that indiscriminately accept exposure to market risk; particularly at valuations that now closely rival the most offensive in history, in the presence of the most extreme overvalued, overbought, overbullish syndromes we identify, and with continued dispersion in our key measures of market action. Market conditions aside, I am also dismayed by the increasingly mean-spirited, divisive, weakly-informed, and nearly pathological mode of governance that is unfolding before us. For now, Wall Street seems to love every bit of it. Then again, we should repeatedly have learned that once blinded by speculation, Wall Street has never had the capacity to recognize a massive toxic liability until it implodes and rains havoc on the entire country. Given historically offensive overvaluation, extended by a post-election blowoff (see Time Stamp of Speculative Euphoria), an economic environment lacking the precursors for sustained growth (see Economic Fancies and Basic Arithmetic), and a mode of governance that practically courts disruption (see On Governance), I expect that the next few years will not go well for risk-seeking strategies, except those explicitly constructed to benefit from market weakness and volatility. The word “risk” has taken on a purely theoretical connotation in recent years, to the extent that it is now seen as equivalent to “return.” Investors are likely to rediscover that its actual meaning is quite distinct, and devastatingly real.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |