|

|

||||||

|

|

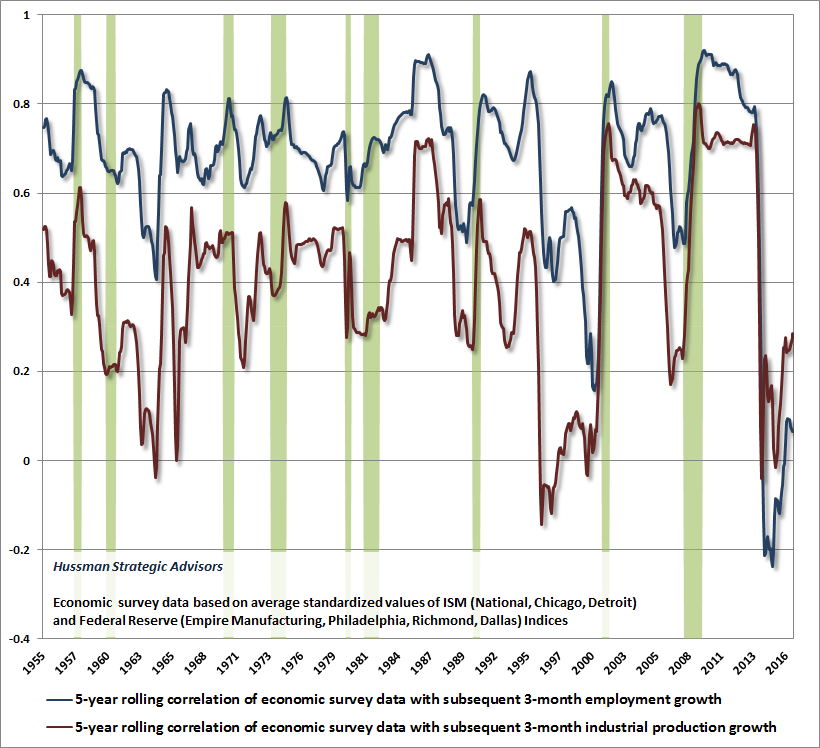

April 10, 2017 Echo Chamber In recent months, the consensus of survey-based economic measures has turned higher, including a variety of surveys of purchasing managers, as well as indices compiled by regional Federal Reserve banks. At the same time, economic measures based on actual activity such real GDP, real sales, consumption, and employment haven’t been nearly as robust, and in some cases have turned lower. This disparity between “hard” activity-based and “soft” survey-based measures has been particularly wide relative to historical norms. Soft data Soft survey-based measures tend to be most informative when they uniformly surge coming out of recessions. In contrast, during late-stage economic expansions, positive disparities in soft measures tend to be false signals that are resolved in favor of harder measures. Sharp downturns in "soft data" can contribute to recession warnings, but they should be confirmed by measures such as slowing growth in employment, real personal income, and consumption. That has been particularly true in recent years, when historically reliable survey-based signals were regularly distorted by swings in expectations about quantitative easing. The current positive divergence is particularly likely to be misleading. The charts of survey-based measures below demonstrate why. What’s striking about survey-based economic measures is that their 5-year rolling correlation with actual subsequent economic outcomes has plunged to zero in recent years (and periodically less than zero), meaning that these measures have been nearly useless or even contrary indicators of subsequent economic outcomes. The first chart shows the correlation between these survey measures and subsequent 3-month growth in employment and industrial production. Note that a correlation of 1.0 is perfect correlation, a correlation of -1.0 is a perfect inverse correlation, and a correlation of zero implies no relationship at all.

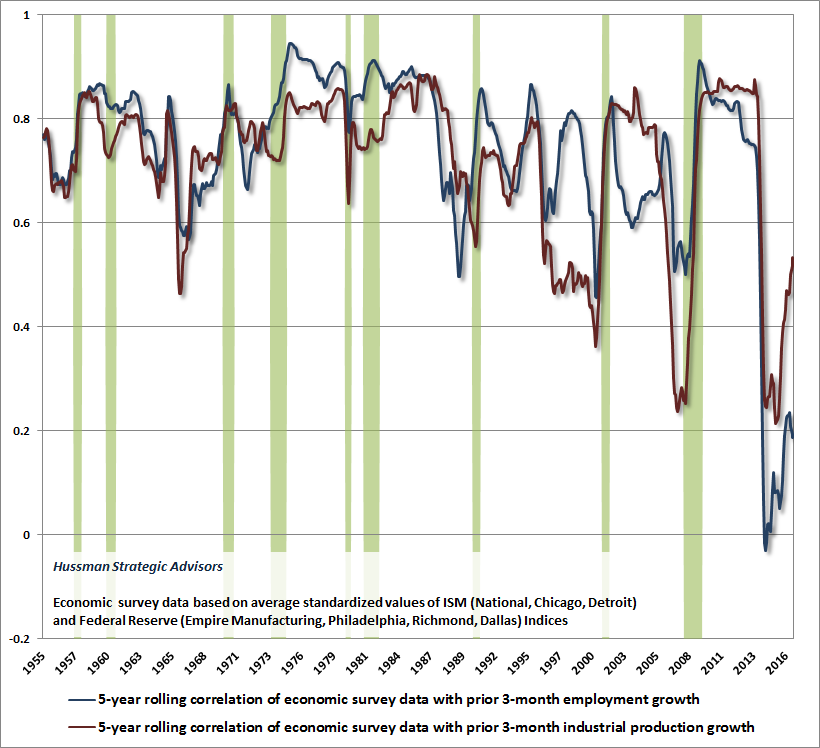

In the chart above, the green bars show U.S. economic recessions. The blue employment line shows the steepest collapse in the reliability of survey-based data in post-war history. While it’s not always the case, one can also see a tendency for these measures to be least reliable (having the lowest correlation with subsequent economic outcomes) just before U.S. recessions. What’s also interesting is that in recent years, these survey-based measures have also become less correlated with prior changes in economic activity. So at least in recent years, these measures have lost their correlation with both past and subsequent economic activity. These surveys may be measuring something, but whatever it is, it’s weakly related to actual economic fluctuations.

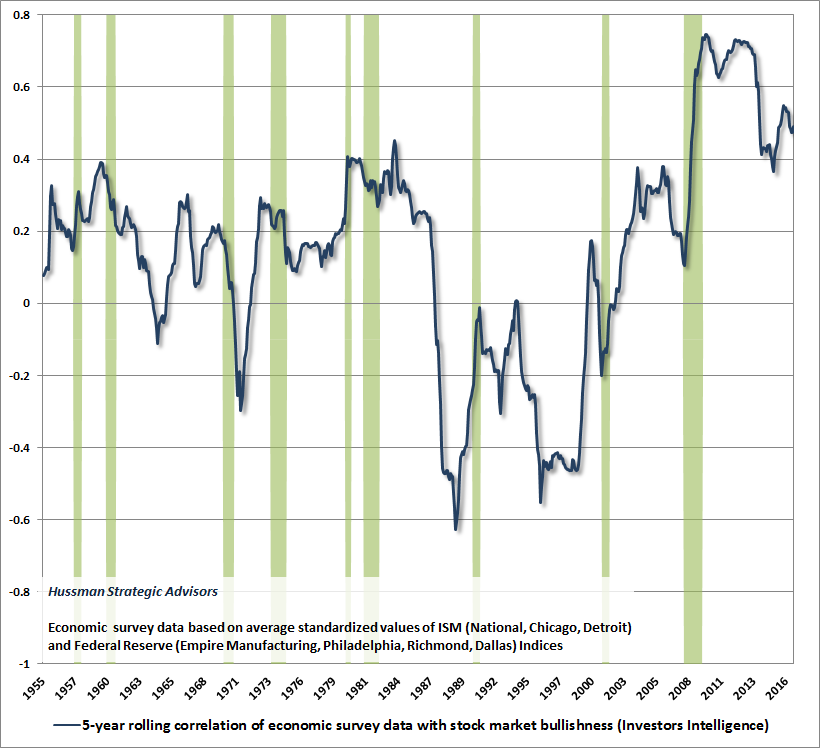

The chart below presents our best guess as to the “something” that these surveys are actually capturing: financial market sentiment. In particular, in recent cycles, these survey-based economic measures have become increasingly correlated with measures of bullish investor sentiment.

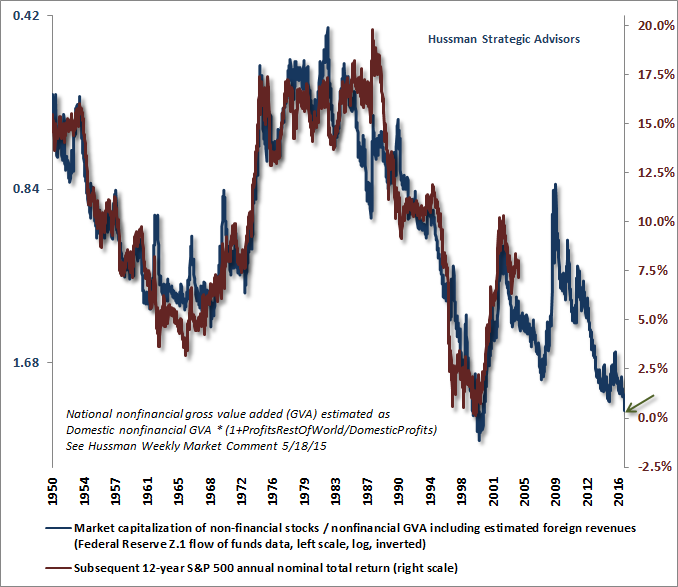

Of course, these optimistic economic surveys are helping to feed optimism among investors of a coming economic renaissance, which we view as wholly inconsistent with the arithmetic of likely GDP growth in the coming years (see in particular Stalling Engines: The Outlook for Economic Growth). That inconsistency is likely to play out over time, but in the short-run, bullish investor sentiment is driving economic sentiment, which is helping to drive bullish investor sentiment. Discussing this feedback loop with Bill Hester, he remarked, “We’re living in a huge echo chamber.” The link between valuations and subsequent market returns has strengthened As a side note, the trailing correlation between soft economic measures and subsequent market returns has also dropped to zero. In contrast, the relationship between valuations and subsequent market returns has actually strengthened in recent years. I’ve periodically noted the correlation of -0.93 between our favored valuation measure, nonfinancial market capitalization to corporate gross value-added, including estimated foreign revenues, and actual subsequent 12-year S&P 500 total returns (technically, we use the log of MarketCap/GVA, for reasons I’ve detailed previously). On shorter horizons, the correlations between this measure and subsequent S&P 500 total returns, in data since 1950, are -0.80 for 7-year returns, -0.54 for 3-year returns, and -0.41 for 18-month returns. If we examine rolling correlations, we find that the correlation between valuations and subsequent market returns has actually strengthened in recent years. A rolling correlation works like this: the most recently available 5-year rolling correlation between log(MarketCap/GVA) and 12-year S&P 500 returns would relate market valuations at every point between 2000-2005 with the 12-year market returns following those dates (that is, the most recent 12-year return period would end in 2017). Notably, the 20-year rolling correlation between log(MarketCap/GVA) and subsequent returns is currently -0.92 for 12-year returns, -0.86 for 7-year returns, -0.80 for 3-year returns, and -0.60 for 18-month returns. Similarly, the 5-year rolling correlations are currently -0.97 for 12-year returns, -0.86 for 7-year returns, -0.66 for 3-year returns, and -0.68 for 18-month returns. Put simply, there’s no evidence whatsoever that the link between reliable valuation measures and subsequent market returns has deteriorated in recent market cycles. I’ve regularly discussed the challenges that emerged in the recent half-cycle as a result of my 2009 insistence on stress-testing our market return/risk classification methods against Depression-era data (see Portfolio Strategy and the Iron Laws for a detailed narrative). Investors are placing themselves in significant danger by incorrectly assuming that our difficulty in this half-cycle was due to some failure in our measures of valuation. It emphatically was not, which should be obvious by reviewing the actual course of those measures over time (chart). It is a mistake to dismiss today’s obscene levels of valuation. I’ve spoken my truth often enough on this matter, but many investors will choose to learn these distinctions the hard way. My sense is that we may be emerging from our own inadvertent journey through purgatory, exiting from the same door that investors are now trampling over each other to enter, as they did in 2000 and 2007. Hard economic data With the U.S. unemployment rate now at 4.5%, the U4 “unemployed and discouraged workers” rate down to 4.8% (just 0.8% from its historic low of 4% in October 2000), and even the U6 “unemployed, plus marginally attached, plus employed part-time for economic reasons” rate within 2.1% of its own historic low, the labor market is already tight enough to prompt the Federal Reserve to further normalize interest rates. Understand that any move in the Federal Funds rate from current levels to at least 2% should be considered a “normalization” of extraordinarily aggressive and unconventionally easy monetary policy, rather than a so-called “tightening.” Indeed, the Taylor Rule presently prescribes a rate closer to 4% as appropriate. Civilian employment now stands at 153.0 million workers. Based on demographic projections by the U.S. Bureau of Labor Statistics, the civilian labor force will reach 163.8 million workers in 2024. Even if we assume that the unemployment rate will remain at 4.5% at that date, the resulting level of civilian employment would be (1-.045)*163.8 = 156.4 million workers. Let that figure sink in. Even assuming a permanently low unemployment rate of 4.5%, cumulative U.S. job creation over the coming 7 years is likely to amount to 3.4 million workers, averaging about 40,000 new jobs per month. That's dramatically fewer than investors seem to be expecting. Worse, if the unemployment rate was to climb to 6.6% by 2024, the number of jobs created over the intervening 7-year period would be zero. The hard economic data tell a much different story than soft survey-based measures, and there is a risk that investors may be setting themselves up for considerable disappointment. The GDPNow projection from the Atlanta Fed for first-quarter 2017 GDP growth has dropped a projected annualized growth rate of just 0.6%.

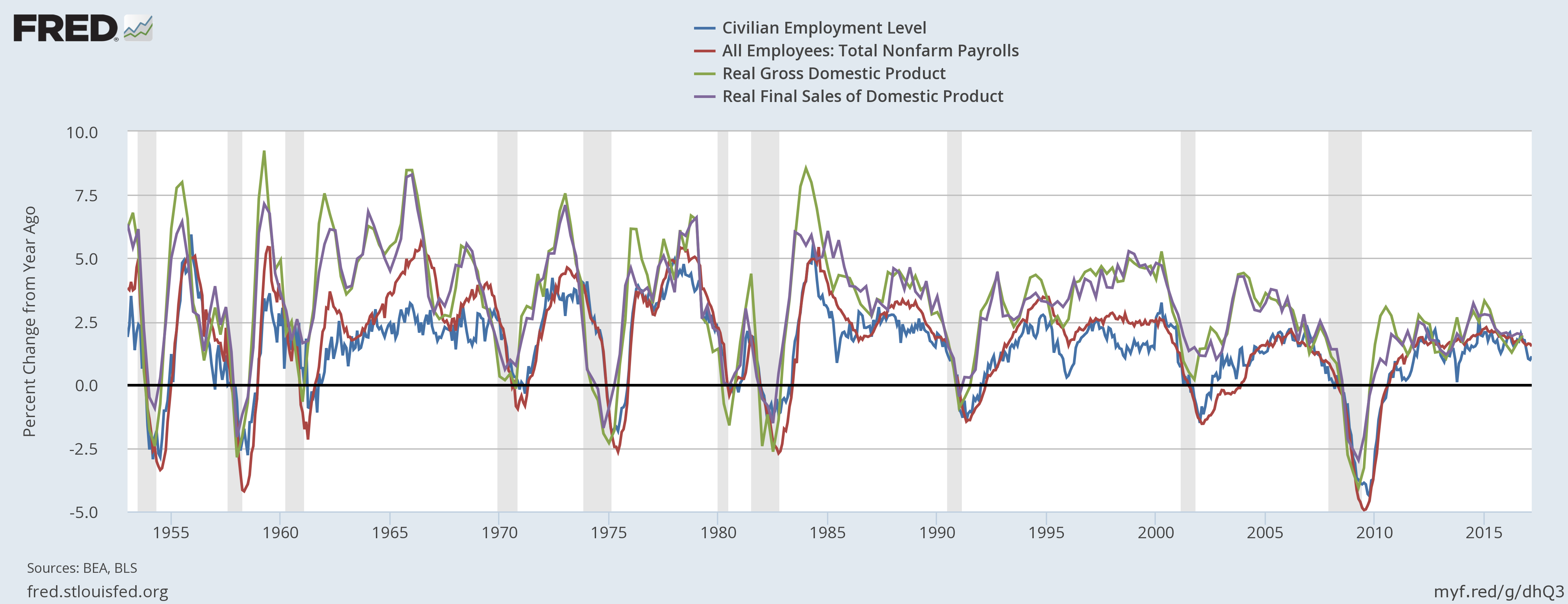

Meanwhile the growth rates of real output and even employment are gradually rolling over, consistent with a late-stage economic expansion, and not very far from levels that have previously attended the start of U.S. recessions. Notice that the difference between growth in the output measures and the employment measures is essentially productivity growth, which has also flattened (click the chart to enlarge). As I’ve previously noted, I do expect a moderate pickup in productivity growth in the coming years, relative to the recent past. The extent to which faster productivity can offset slowing labor force growth and the risk of weak gross domestic investment (particularly in the event of trade tensions) is unclear. As I detailed last week, investors shouldn’t be particularly surprised if real GDP growth amounts to just a fraction of a percent annually over the coming 4-year period.

The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |

{kind=link}