|

|

||||||

|

|

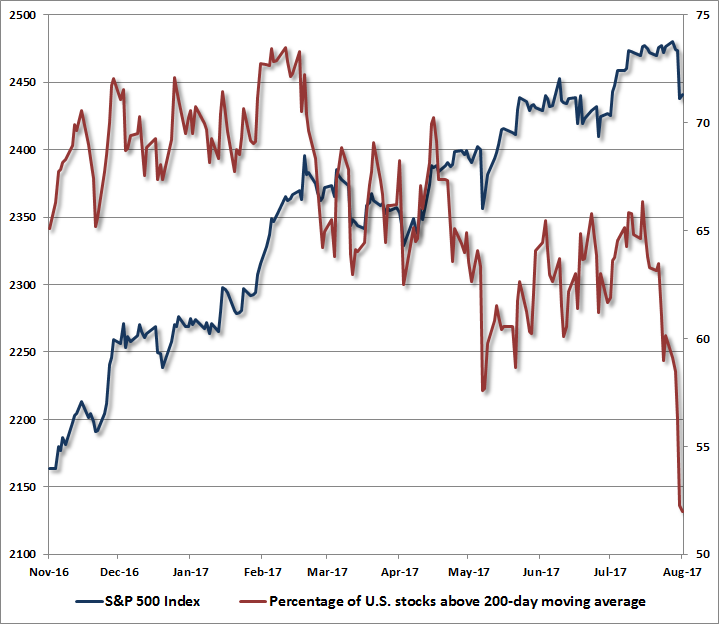

August 14, 2017 Broadening Internal Dispersion Nothing in history leads me to expect that current extremes will end in something other than profound disappointment for investors. In my view, the S&P 500 will likely complete the current cycle at an index level that has only 3-digits. Indeed, a market decline of -63% would presently be required to take the most historically reliable valuation measures we identify to the same norms that they have revisited or breached during the completion of nearly every market cycle in history. The notion that elevated valuations are “justified” by low interest rates requires the assumption that future cash flows and growth rates are held constant. But any investor familiar with discounted cash flow valuation should recognize that if interest rates are lower because expected growth is also lower, the prospective return on the investment falls without any need for a valuation premium. This is not just a theoretical matter. Across history, the impact of variations in interest rates and growth rates systematically wash each other out, which is why long-term returns are so tightly linked to starting valuations (see Rarefied Air: Valuations and Subsequent Market Returns for a full exposition). With regard to future economic growth prospects, the fact is that demographic factors constrain likely U.S. labor force growth to just 0.3% annually in the coming years, while U.S. productivity growth has declined from 2% annually in the post-war period, to 1% annually over the past decade, and just 0.6% annually over the past 5 years. Add 0.3% and 0.6%, and the baseline expectation for U.S. economic growth in the coming years is just 0.9% annually, assuming that the unemployment rate does not rise at all from the current level of 4.3%. As I detailed in Stalling Engines: The Outlook for U.S. Economic Growth, even a future 1.85% trajectory for U.S. real GDP growth requires that some combination of labor force growth and productivity growth will accelerate from the current baseline. Given that real U.S. GDP growth has averaged just 2.2% over the past 4 years, and that the current starting positions of labor force growth, unemployment, and the trade balance suggest a deceleration even from that average, we shouldn’t be surprised if real U.S. GDP growth amounts to just a fraction of a percent annually over the coming 4-year period. Valuations, market action, and overextended syndromes It’s important to observe that if short-term interest rates were still at zero and market internals were favorable, even the most extreme overvalued, overbought, overbullish syndromes we identify would not be enough to push us to a hard-negative market outlook. That, in a nutshell, is the central lesson from quantitative easing, and is one that could alone have dramatically altered our own challenging experience in the recent speculative half-cycle. At present, however, we observe not only the most obscene level of valuation in history aside from the single week of the March 24, 2000 market peak; not only the most extreme median valuations across individual S&P 500 component stocks in history; not only the most extreme overvalued, overbought, overbullish syndromes we define; but also interest rates that are off the zero-bound, and a key feature that has historically been the hinge between overvalued markets that continue higher and overvalued markets that collapse: widening divergences in internal market action across a broad range of stocks and security types, signaling growing risk-aversion among investors, at valuation levels that provide no cushion against severe losses. We extract signals about the preferences of investors toward speculation or risk-aversion based on the joint and sometimes subtle behavior of numerous markets and securities, so our inferences don't map to any short list of indicators. Still, internal dispersion is becoming apparent in measures that are increasingly obvious. For example, a growing proportion of individual stocks falling below their respective 200-day moving averages; widening divergences in leadership (as measured by the proportion of individual issues setting both new highs and new lows); widening dispersion across industry groups and sectors, for example, transportation versus industrial stocks, small-cap stocks versus large-cap stocks; and fresh divergences in the behavior of credit-sensitive junk debt versus debt securities of higher quality. All of this dispersion suggests that risk-aversion is rising, no longer subtly. Across history, this sort of shift in investor preferences, coupled with extreme overvalued, overbought, overbullish conditions, has been the hallmark of major peaks and subsequent market collapses. Again, the principal lesson of the recent half-cycle was that in the face of zero interest rates, even the most extreme “overvalued, overbought, overbullish” syndromes were not enough to anticipate steep market losses (as they typically were in prior market cycles). Instead, investors were driven to believe that they had no other alternative but to continue their yield-seeking speculation. In the face of zero interest rates, one had to wait for market internals to deteriorate before adopting a hard negative market outlook. At present, we observe neither zero interest rates, nor uniformly favorable market internals. In the current environment, we expect that obscene valuations and severe "overvalued, overbought, overbullish" syndromes are likely to be followed by the same outcomes that have attended similar conditions across history. A few graphs will update the present situation. The chart below shows the percentage of U.S. stocks above their respective 200-day moving averages, along with the S&P 500 Index. The deterioration and widening dispersion in market internals is no longer subtle.

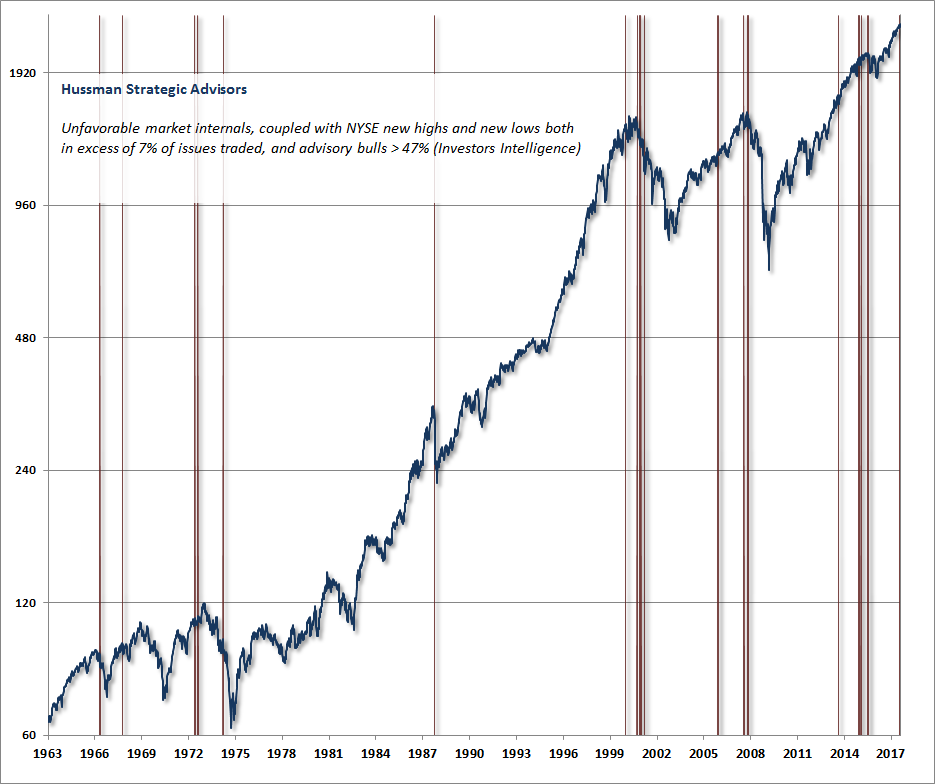

Last week, both new highs and new lows on the NYSE exceeded 7% of total issues traded. Over the past three decades, I’ve periodically described this kind of internal dispersion as a negative consideration for the market (h/t Norm Fosback), particularly when it is joined by lopsided bullish sentiment and negative market internals across our own measures. While we don’t view this divergent leadership as necessary or sufficient for either a market peak or severe subsequent losses, it’s notable that the same set of features also emerged near the 1973, 1987, 2000 and 2007 peaks.

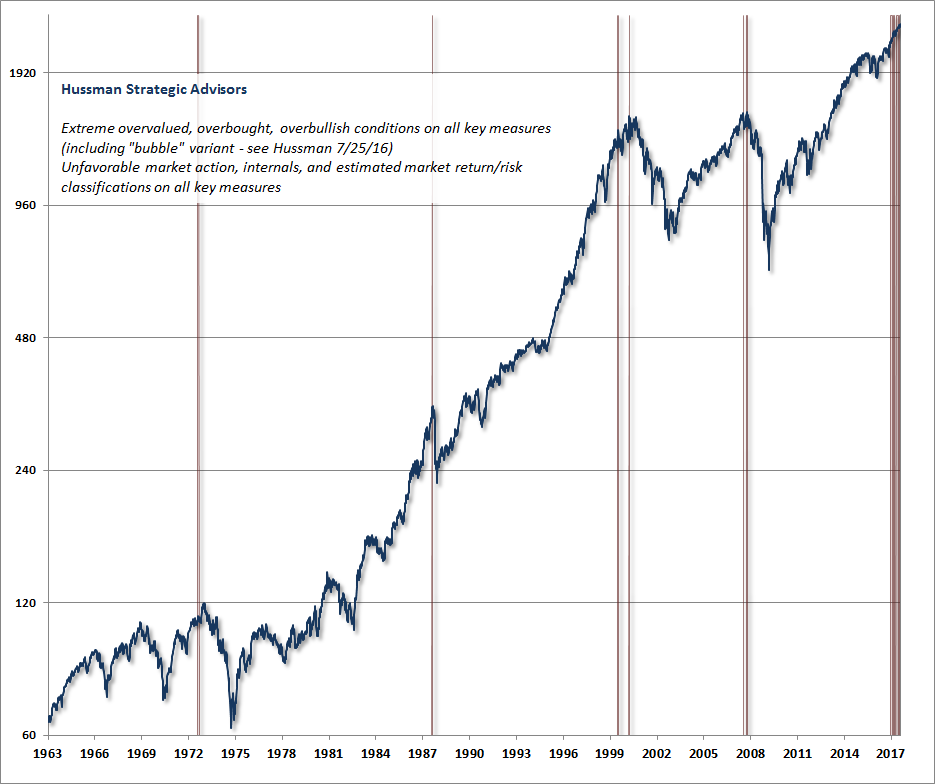

The final chart includes more proprietary factors, but they largely reflect measures and syndromes that I’ve detailed in prior commentaries over time. The key point to emphasize is that investors presently face the broadest and most obscene valuations and “overvalued, overbought, overbullish” syndromes we define, and that unlike the bulk of the recent speculative half-cycle, these extremes are joined by clear deterioration and dispersion across market internals. In my view, rich valuations are not at all “justified” by low interest rates. Rather, to the extent that low interest rates persist, it is likely to be because of failing U.S. economic growth. If one understands how assets are priced, that is a combination that justifies no valuation premium at all. Yet even if economic growth was to accelerate to historically-normal levels, and interest rates were held 3% below their own historical norms for a full decade, only a premium of 30% (10 years x 3%) could be justified. Instead, the most reliable valuation measures we identify are about 170% above (2.70 times) their historical norms. Frankly, I don’t expect to observe any material premium by the completion of this cycle. Market internals suggest that risk-aversion is now accelerating. The most extreme variants of “overvalued, overbought, overbullish” conditions we identify are already in place. A market loss of [1/2.70-1 =] -63% over the completion of this cycle would be a rather run-of-the-mill outcome from these valuations. All of our key measures of expected market return/risk prospects are unfavorable here. Market conditions will change, and as they do, the prospective market return/risk profile will change as well. Examine all of your investment exposures, and ensure that they are consistent with your actual investment horizon and tolerance for risk. The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |