|

|

||||||

|

|

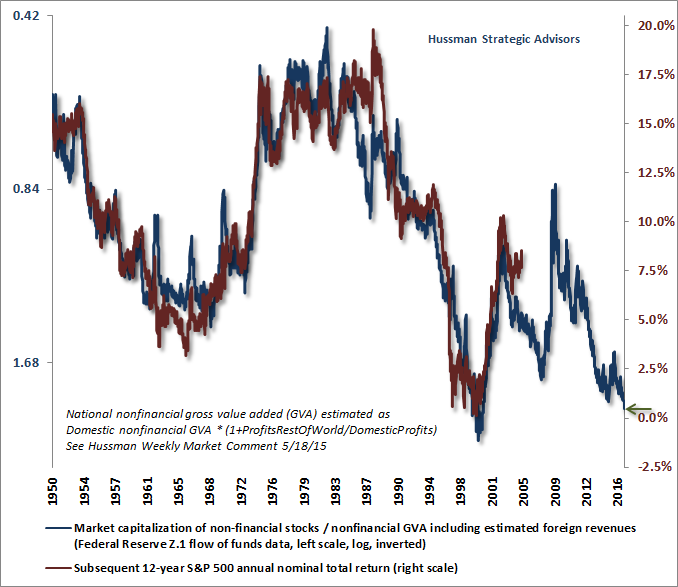

April 24, 2017 Valuation Breakevens Let’s begin by distinguishing the short-run from the full-cycle and the long-run. While we presently observe wicked valuations from a historical perspective, the fact is that valuations often have very little effect on short-term market behavior. The primary factor that drives market fluctuations over short horizons is the preference or aversion of investors toward risk, and the best measure of that is the uniformity or divergence of market internals across a broad range of individual stocks, industries, sectors and security types (when investors are inclined to speculate, they tend to be indiscriminate about it). While the classification methods we’ve found most reliable in complete market cycles across history remain negative, we follow a broad range of measures, and a few of the less-reliable but still-useful measures are mixed. As a result, our immediate view is currently a bit more neutral than negative. Our overall outlook is defensive either way, so that may seem like a distinction without a difference, but it's mainly a statement about the magnitude of our near-term concerns. Currently, we’d look for more uniform deterioration in market internals before pounding the table about an immediate market collapse. From a full-cycle perspective, my expectation remains that the S&P 500 is likely to lose between 40-60% of its value over the completion of the current cycle (a market cycle combines a bull market and a bear market, and a full cycle is appropriately measured peak-to-peak or trough-to-trough). On a longer-term perspective, we presently estimate 12-year S&P 500 nominal total returns averaging just 0.6% annually. Indeed, as noted below, unless one believes that the entire structure of the U.S. financial markets has changed since as recently as 2012, investors should allow for the market to lose at least one-third of its value over the completion of the current cycle, with the S&P 500 underperforming even the depressed yields on Treasury bonds over the coming decade. To get a sense of why these expectations are so pointed, I’ll begin with a familiar chart, which shows the ratio of nonfinancial market capitalization to corporate gross value-added (including estimated foreign revenues). I originated this measure to create a true apples-to-apples metric that also takes foreign revenues into account. Perhaps not surprisingly, we find this measure better correlated with actual subsequent market returns than any other measure we’ve studied, including forward operating P/Es, the Shiller CAPE, price/cash flow, price/dividend, Tobin’s Q, the Fed Model, and market capitalization/GDP, among others. On a 12-year horizon (the point where the autocorrelation profile of valuations typically hits zero, and the most reliable horizon over which mean-reversion can be expected), MarketCap/GVA has a correlation of -0.93 with actual subsequent S&P 500 total returns (negative because higher valuations imply lower subsequent returns). The chart below presents MarketCap/GVA on an inverted log scale (blue line, left), along with the actual subsequent 12-year nominal annual total return of the S&P 500 Index (red line, right scale).

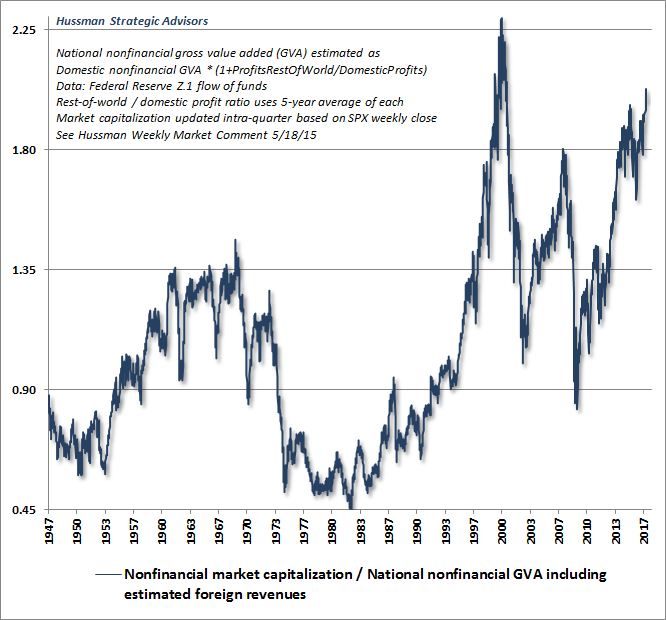

I occasionally receive questions asking why our valuation measures are supposedly “not working.” Wait. Hold on and look carefully at the chart above. It should be rather obvious that valuations have continued to “work” even in recent complete market cycles, and throughout the recent series of bubbles and crashes, correctly identifying stocks as wickedly overvalued in 2000, today, and to a lesser extent, 2007, while identifying stocks as undervalued in 2009, and reasonably valued at the 2002 low. Even the “overshoot” of actual returns from expected returns in the past few years is something that regularly occurs at valuation extremes, particularly when the completion of an extreme cycle occurs a bit sooner or later than usual. Note, for example, the 1988 overshoot of actual market returns for the 12-year horizon that ended with the 2000 peak. The reverse tendency is often seen at major lows. Note, for example, the 1997 undershoot of actual market returns for the 12-year horizon that ended with the 2009 low. I’m going to say this yet again: our challenges in the recent half-cycle had nothing to do with valuation measures, but was instead the result of my own insistence in 2009 on stress-testing our methods of classifying market return/risk profiles against Depression-era data. The inadvertent result of that decision was to create an Achilles Heel in the face of zero interest rate policy and extreme yield-seeking speculation. That took us much of the recent half-cycle to fully address. See Portfolio Strategy and the Iron Laws for further discussion. What investors imagine to be a “different” market is merely a market near the mature end of an as-yet uncorrected episode of reckless speculation, just as it was in 2000. If you’re an investor and you want to do yourself a favor, do this: distinguish my own inadvertent stumble in the recent half-cycle, which I’ve regularly, openly and exhaustively discussed, from objective evidence on valuations. What you see at present is not valuations “failing to work.” We already know valuations don’t govern short-run market outcomes - that’s why market action and related measures are useful over shorter segments of the market cycle. What you see is a speculative bubble that is doing its best to draw you in like Sirens singing to Ulysses, across a graveyard of ship hulls smashed against the rocks. The chart below presents MarketCap/GVA on a regular scale in post-war data. What investors should note is that no market cycle in history, including the most recent ones, has failed to take valuations down to half of today's level (or below) over the completion of the cycle. So whatever change investors think has occurred to make valuations useless had better be something permanent that’s occurred in the past few years. And even if investors do believe that the level of valuations has shifted forever higher (meaning that the level of normal stock market returns has also shifted forever lower), they are encouraged to recognize that there are no permanent plateaus in the chart. Instead, one observes repeated extremes and troughs. The current level of MarketCap/GVA is above 2.0. Investors who refuse to allow for a retreat even to a level of 1.35 over the completion of this cycle (which would be a market loss of one-third) had better be able to explain what has permanently changed since 2012, because we saw 1.35 even well into the current speculative run. Zero interest rates, by the way, are not adequate to dismiss valuations here. Changing the level of interest rates alters the laws of finance no more than changing the value of x alters the laws of arithmetic. You don’t suddenly decide that math itself is no longer useful. The maximum “justified” effect of interest rates on valuations is quantifiable (see The Value of Dry Powder). The fact is that current valuations would not be “justified” even the Fed brought rates back down to zero and held them there for decades.

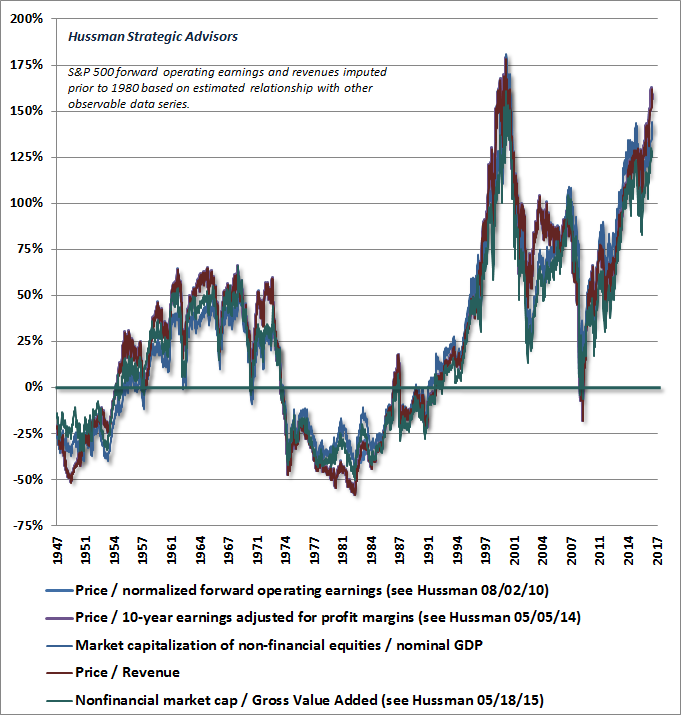

The chart below broadens the picture to the measures we’ve found most tightly correlated with actual subsequent S&P 500 total returns in market cycles across history. These measures are presently well beyond double their historical norms, ranging from 125% to 160% over those norms.

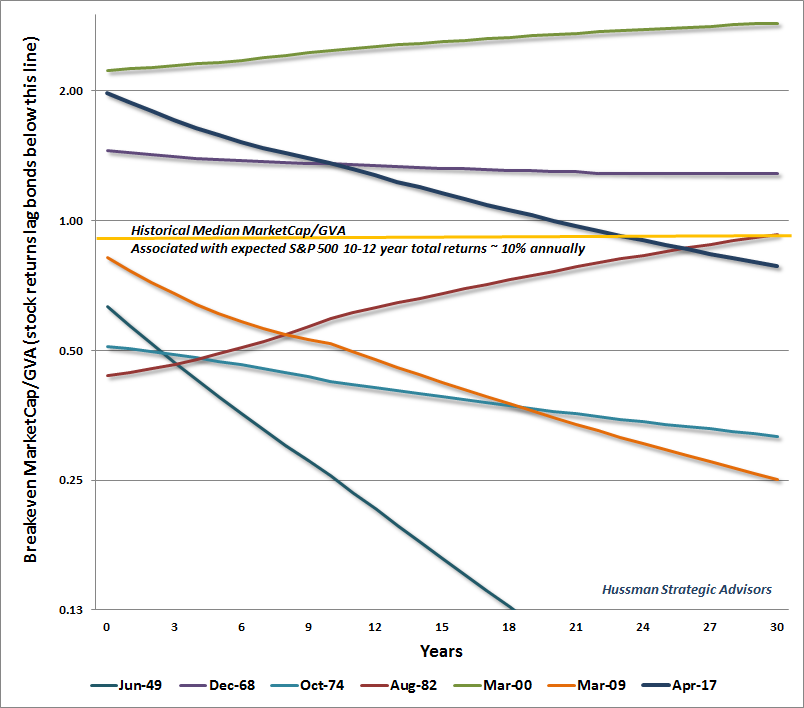

It’s not unheard-of for a peaceful Zen teacher to give a student a little whack over the head with a bamboo stick in order to wake them up, as an act of compassion. So I’m going to be blunt. Stop arguing that the market has permanently changed over the last several decades when you’re really trying to argue that the market has permanently changed over the past 5 years. Don’t get me wrong. It’s essential to ask questions, obtain data, and test every possibility. What’s offensive is Wall Street’s endless reliance on verbal argument in place of evidence, and the eagerness of investors to buy into verbal fictions to the point where they second-guess actual data. If you can’t demonstrate your arguments with evidence, you’re fooling yourself. You’re mistaking the delay of consequences with the absence of consequences. You see the advancing half of a mature speculative episode and you’re looking for any excuse at all to escape into a fantasy world where stock prices never go down. Worse, you may even be using a stumble I’ve already admitted and addressed in the first half of this cycle as an excuse to make your own in the second half. Again, on the question of near-term outcomes, we’ll take our evidence as it arrives, particularly from market internals. In any event, however, I expect any near-term market returns to be quickly wiped out quite early into the completion of this cycle. Investors who ignore valuations are going to get hurt. Valuation Breakevens In prior comments, I’ve demonstrated that the relationship between valuation measures such as MarketCap/GVA and subsequent S&P 500 total returns is not affected by the level of interest rates. That’s not to say that interest rates don’t affect valuations - though the historical evidence is far more mixed on that question than investors seem to assume. Rather, the point is for any given level of valuations, we can estimate prospective market returns without appealing further to interest rates. That’s because, given any set of expected future cash flows along with the current market price, one already has all the information required to estimate the future return on the asset. Of course, that estimated rate of return can then be compared with the prevailing level of interest rates to evaluate the relative merits of the two choices (See The Most Broadly Overvalued Moment in Market History for more on this point). Lower interest rates may encourage investors to accept higher valuations (which imply correspondingly low future stock returns), but as a historical matter, investors don’t reliably behave this way. In fact, prospective stock returns and interest rates have actually been negatively correlated through most of the past century, outside of the inflation-deflation cycle from the early 1970’s until about 1998. In fact, the correlation between the two has been negative even over the past 20 years. Still, the following is an approach I constructed to use information on stock valuations and interest rates in a systematic way, by estimating the break-even level of valuation that would have to exist at given points in the future, in order for stocks to outperform or underperform bonds over various horizons. The chart below shows these breakeven estimates for several market extremes across history: June 1949, December 1968, October 1974, August 1982, March 2000, March 2009, and April 2017. Each line begins at the prevailing market valuation at each date (so the starting point gives a quick indication of how rich or cheap the market was relative to historical norms at each date). As one moves into the future, the lines show the valuation level below which stocks would lag bonds, and above which stocks would outperform bonds, over each horizon. Below, those horizons extend from 1 to 30 years. Everywhere below the breakeven profile, the return on stocks purchased at today's levels would be expected to lag what you could expect from bonds over the same horizon. Put simply, low breakeven profiles are better for stocks, since their returns over any given horizon (measured from today to various future dates) would only be expected to lag bonds at points where future valuations fall below the breakeven line. A breakeven profile that begins at a low level (regardless of its slope) also means that investors are bargaining for a strong overall return in stocks either way. Conversely, a breakeven profile that begins at a high level means that investors are bargaining for a poor overall return in stocks either way. A breakeven profile that slopes downward means that bonds have little long-run advantage, so beating them becomes progressively easier over time. A breakeven profile that slopes upward means that interest rates are so attractive that market valuations must rise over time in order for stocks to keep pace. Today's high, downward sloping breakeven line is essentially the worst of both worlds for both asset classes. The high level means that prospective stock returns are weak, while the downward slope means that prospective bond returns aren't very attractive either. This menu will change over the full course of the market cycle. For example, in June 1949, MarketCap/GVA stood at 0.64, a level we associate with expected 12-year returns of more than 15% annually. The dividend yield on the S&P 500 stood at 7.4% at a time when Treasury bond yields were just 2.4%. That’s why the breakeven line plunges so steeply. Given those relative prospective returns, stock valuation multiples could have declined progressively, yet stocks would still have been expected to outperform bonds (indeed, the S&P 500 averaged total returns of close to 19% annually in the 12 years following the June 1949 low).

By contrast, in March 2000 (green line), MarketCap/GVA reached 2.29, a level that we associate with 12-year expected S&P 500 total returns of zero. At the same time, the dividend yield on the S&P 500 was just 1%, while Treasury bond yields were at 6.2%. The combination produced a situation where even very high future valuations could be expected to result in stocks underperforming bonds over the same horizon. Indeed, today, even 17 years later, and even after one of the most offensive speculative episodes in history, the total return of the S&P 500 has averaged only 4.5% annually since that 2000 peak, easily lagging bonds over this horizon, with violent interim losses of 50% and 55% respectively, and another likely on the way. Notice the orange breakeven corresponding to the March 2009 low. The ratio of MarketCap/GVA dropped to about 0.8, a level that we associate with 12-year prospective annual returns about 12% annually (as I observed in real time - recall that our challenges in the half cycle that followed were due to my insistence on stress testing our methods against Depression era data, not to any change in the reliability of our valuation methods). Meanwhile the S&P 500 dividend yield was at 3.6%, while Treasury yields were at 2.9%. As a result, the breakeven line slopes down, implying that only progressively lower valuations would cause stocks to underperform bonds in subsequent years. The December 1968 valuation peak (purple) was associated with a MarketCap/GVA ratio of 1.5, which we associate with expected S&P 500 12-year total returns of about 5%. At the time, however, Treasury bond yields were above 6%, requiring elevated valuations to be sustained for quite some time in order for stocks to outperform bonds. As it happened, the S&P 500 enjoyed average annual total returns of 6% over the following 12-year period, falling slightly short of the return on bonds over the same horizon. The October 1974 low, less than 6 years later (light blue) was associated with a MarketCap/GVA ratio of just 0.5, resulting from intervening growth in fundamentals coupled with a 50% market loss. We associate that valuation level with expected S&P 500 12-year total returns of 17.9%. At the time, Treasury bond yields stood just over 8%. As it happened, the total return of the S&P 500 averaged 17.0% over the following 12-year period, even though valuations would establish a deeper secular low in 1982. The August 1982 secular low (red) was a bit unusual, because the breakeven line slopes higher. At that secular low, the ratio of MarketCap/GVA fell to just 0.4, a level that we associate with expected S&P 500 12-year returns averaging over 19% annually. The actual 12-year total return came in at 17.2%, with the tech bubble extending that return to 20% annually over the nearly 18-year span ending with the March 2000 market peak (hold that thought until the next paragraph). The S&P 500 dividend yield rose above 6.6% at the 1982 low, but note that the breakeven line still slopes up, meaning that valuations still needed to rise over time in order for stocks to outperform bonds. The reason for this is that the yield on Treasury bonds in August 1982 was more than 13%. Based on the estimated 1982 breakeven line, stocks would not outperform bonds over the following 30 years unless valuations moved above their historical norms by August 2012. In hindsight, we know that the tech bubble didn't last. In fact, MarketCap/GVA stood slightly below 1.0 by August 2012, and as a result, the S&P 500 actually slightly underperformed bonds as measured from the August 1982 low, with an annual total return averaging 11.9%. That's a useful reminder that the glorious market returns one measures at the peak of a bubble aren't actually retained over the completion of the cycle. Think carefully about that. The gains of recent years are just as unlikely to be retained. This is a very, very bad time to finally become "convinced" about the merits of passive investing. The dark blue line shows the current breakeven profile as of last week. MarketCap/GVA recently pushed above 2.0, driving our 12-year estimate of S&P 500 total returns to just 0.6% annually. The dividend yield of the S&P 500 is now just 2.0%, but with the 10-year Treasury bill yield at just 2.2%, investors face a dismal menu of expected returns regardless of their choice. Indeed, in order for expected S&P 500 total returns to outperform even the lowly return on Treasury bonds in the years ahead, investors now require market valuations to remain above historical norms for the next 22 years. The good news is that this menu is likely to improve substantially over the completion of the current market cycle. The problem is that current valuation extremes present a hostile combination of weak prospective return and steep risk. Even a retreat in MarketCap/GVA from the current level of 2.0 to a still-elevated level of 1.35 over the next decade will likely result in S&P 500 total returns below the 2.3% available on Treasury bonds. To see why, assume that real economic growth averages 2% in the coming decade (see Stalling Engines to see why this is quite a likely expectation), while inflation averages 2% annually. Couple 4% annual growth in corporate gross value added (matching the growth rate of GVA over the past two decades, and close to the growth rate of earnings over the same period) with a 2% dividend yield and a modest reduction in the valuation multiple, and you get S&P 500 annual returns of roughly: (1.04)*(1.35/2.0)^(1/10)+.02-1 = 2% annually, with the S&P 500 Index itself no higher 10 years from now than it is today.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |