|

|

||||||

|

|

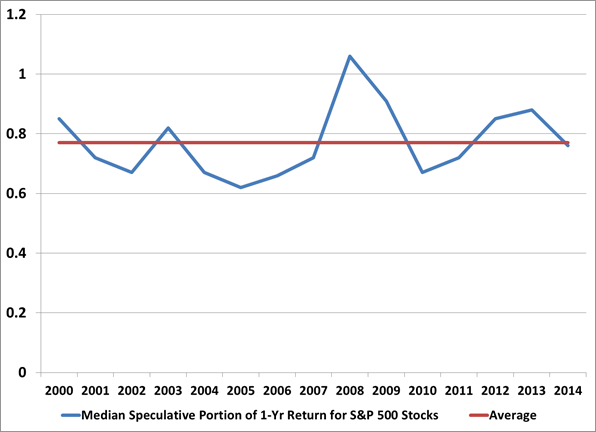

Is the Rush into European Stock Markets Warranted? Two Risks to Consider Amid the Bullishness According to a recent Bank of America Fund Manager Survey, Europe is now the top pick of managers for the coming twelve months. A record 63 percent of fund managers are allocating their assets toward Europe, up from just 18 percent earlier this year. More than 80 percent see the Euro-area economy strengthening this year, boosted by export growth tied to a 25% plunge in the euro amid fresh quantitative easing by the European Central Bank. “It is as if there is not a single bear left,” said the bank’s European strategist. He followed up with, “Bullishness towards European stocks has reached unchartered territory”. European stock markets, on the surface, certainly have the characteristics investors typically seek out, especially in this new era of staggered global monetary easing campaigns. The ECB has a new QE program in the works, just as the US is winding down its own. At a cyclically-adjusted P/E ratio of 17 for the MSCI European Index, versus 27 for the US, the region’s stock markets appear cheaper. And, especially in local currency terms, the euro-area markets have witnessed the typical post-QE announcement boost after Mario Draghi sketched out plans for a bond buying program back in January. Economic data has also been coming in stronger than economists had expected, pushing European stocks to their highest level since early 2008. There are two characteristics of these markets that investors should consider, though, before accepting the premise that European stocks are ideal candidates to overweight in a portfolio. The first is that rising valuation multiples have been the nearly singular cause for higher prices over the last few years. Second, the component of returns driven by rising valuation multiples - which have diverged so extensively from fundamental growth - is highly correlated to US stock market fluctuations. To be bullish on European stocks, one should be bullish on US stocks. This is not how a recommendation for international stock markets is usually presented. It’s typically suggested that because US stocks are expensive, then investors should consider the cheapest international stocks, which among developed countries, are in the European markets. The historical record indicates that this suggestion will likely be appropriate only if the US market continues to advance. If a bear market were to begin in US stocks, European stocks – especially the cheapest ones - would likely perform as badly as or worse than US markets. It is important to distinguish two influences on international stocks. In the long-term, valuation considerations are essential. In the intermediate term, and especially during declines in the U.S. market, foreign stocks are much more tightly linked to U.S. markets than internationally diversified investors often expect. On the valuation front, the historical evidence does support a preference for investing in countries with lower relative valuations. For example, a portfolio holding the 5 highest yielding developed countries each month since 1970 would have outpaced the MSCI World Index by 3.5 percent a year. Even so, this country rotation strategy has trailed the World Index since 2010 by a wide margin, as have most international value indices. It’s possible that underperformance could continue after the initial burst of excitement following the announcement of ECB QE. A more persistent increase in fundamental growth (to catch up with the price increases of the past few years), or a correction from recent highs, would create an environment more typical for European value stocks to do well. The Speculative Component of Short-Term Returns One way to project future expected returns, and to analyze past returns, is to separate them into a component that comes from growth in fundamentals and the component that comes from the change in the valuation multiple on those fundamentals. Jack Bogle, who has being explaining returns to investors this way for decades, calls these components the ‘fundamental’ component and the ‘speculative’ component of return. Bogle has typically used dividends as a fundamental, but sales and smoothed measures of earnings can also be used, provided that the corresponding valuation multiples are used. Take for example one of the best performing stocks in the S&P 500 last year, a food and drug retailer that rose more than 60 percent. During that period, sales per share rose about 16 percent while the price to sales multiple rose by more than 40 percent. (We’ll exclude dividends here as they typically make up a minor component of short-term performance). The speculative component of last year’s price return therefore made up about 70 percent of the total gain. Another top performer, an operator of medical facilities, had similar numbers. Its sales rose 10 percent, and its price to sales ratio rose 40 percent. So the speculative component contributed about 80 percent of its roughly 50 percent gain. Although the portion of returns originating from the speculative component in both of these cases may seem high, it’s actually what you’d expect from a large sample of stocks. In the graph below, I’ve taken a smoothed median of the speculative contribution for the largest US stocks each year, beginning in 2000. That contribution can vary, but on average, about 80 percent of the one-year price gain (or loss) is typically driven by rising (or falling) valuation multiples. The outlier in the chart is interesting too. The speculative component rose above 100 percent during the 2008-2009 bear market, when the drop in valuation multiples made up the entire loss in share value, on average.

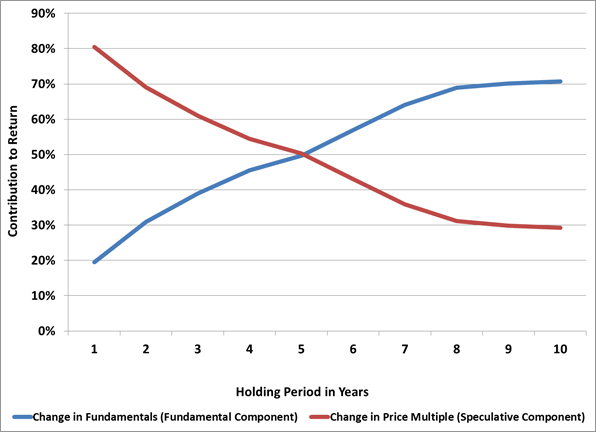

As the period of analysis lengthens, a larger contribution of a stock’s return comes from a change in the fundamentals, compared with the contribution from a change in valuation multiples. In the graph below I’ve plotted the make-up of these contributions. The data represents the 1500 largest US stocks going back 35 years. About 80 percent of first-year returns typically come from a change in valuation multiples and 20 percent from a change in fundamentals. That aligns well with the time-series analysis of 1-year returns shown in the graph above. By the third year of the holding period, about 40 percent of the return originates from a change in the fundamentals. By year five, half of the return originates from a change in the fundamentals. Over longer periods of time reaching out to ten years, the bulk of the return originates from a change in the fundamentals, reversing the importance of the components relative to year one. Considering the large span of time the data covers and the large number of companies it includes, we can assume that the particular progression shown in the graph from speculative contribution to fundamental contribution is to be what is expected, on average, from individual companies.

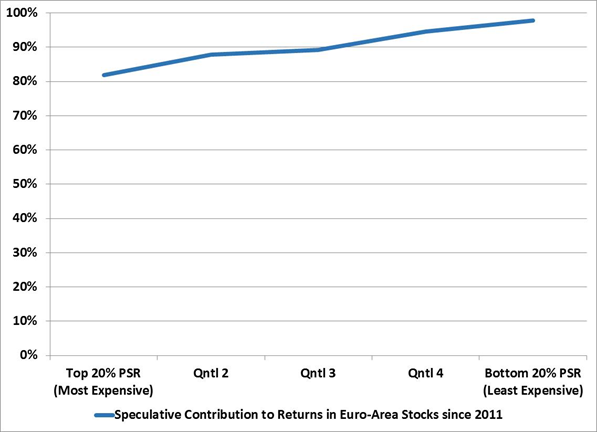

European Value Stocks Since 2010, value strategies and stocks have performed poorly on a relative basis. The country rotation strategy mentioned above is trailing the MSCI World benchmark noticeably over that time period, gaining at just 1.7 percent annually. Most of the value indices tracked by MSCI have also trailed the World benchmark (even excluding the performance of the US market). But most of this underperformance occurred in 2010 and 2011. Since Mario Draghi’s “whatever it takes” remark in July 2012, many of the regional value indexes have done as well or better than the World Index, especially European value. So, the cheapest stocks in the cheapest markets have definitely participated during this period of anticipation of ECB QE. As a number of other analysts have pointed out, there has been a growing divergence between the fundamental component and the speculative component of European stock market returns. There has been a persistent trend of rising multiples and flat or falling earnings since 2012. Using the framework for return attribution discussed above and applying it to European stocks, we can put the stark divergence between the two into better context. The graph below reflects the stocks in the Bloomberg European 500 Index and assigns them to 5 baskets based on their recent price to sales ratio. The blue line shows the median speculative contribution for each basket of stocks. The most expensive stocks begin on the left. The graph shows the stocks in the bottom 20%, ranked by price to sales ratio, have generated nearly all of their returns from the speculative component.

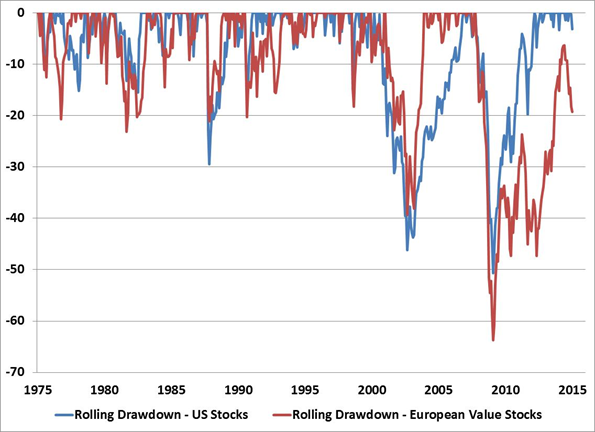

European value stocks have kept pace broadly with the other benchmarks in the past few years thanks to essentially one force alone – rising valuation multiples. We’re three years into this particular measurement period for stocks. By now, based on historical norms, about 30 to 40 percent these returns, on average, should have originated from the fundamental component of return – growing sales, earnings, and dividends. That has clearly not been the case with European stocks, especially the cheapest ones. This part of the analysis doesn’t suggest European stocks must come crashing down in value. The cyclically-adjusted PE ratio for the European Value Index is still below its long-term median, and lower than in other developed regions. It also doesn’t suggest that these investments will trail the return of the US market in the long-term. The European Value Index has a dividend yield of 4.2 percent, more than twice that of the US. On dividend income alone, the region has a head start on the US market, especially if the US market trades in a tight trading range. But it does suggest that it’s likely that the portion of return originating from rising multiples is unlikely to be as strong as it has been the last few years, and a much larger burden will rest on the growth in fundamentals. The Correlation of Speculative Returns and US Markets Euro-area stocks have a significant speculative component priced into them relative to the change in fundamentals over the last few years. The cheaper the stock, the more speculation has been priced in, on average. The risk at present is that this speculative component is highly correlated with US markets, and that correlation has been rising over the last two decades. In the event of a U.S. market correction, it is likely that European value stocks (and European stocks in general) would do as poorly, or worse, than the much more expensive US market. The graph below shows the rolling drawdowns of the MSCI US Index and the MSCI European Value Index (using monthly data, in US dollars). The fact that both markets tend to experience their deepest losses simultaneously is why it’s sometimes said that “international diversification helps except when you need it most.” What’s interesting about the graph is where the red line – the European Value Index – typically sits in relation to US stocks during bear market declines, especially in more recent data. During many of the declines, the European Value Index has either fallen about as much as the US market, or has fallen farther. And, not surprisingly, this tendency was more pronounced during the financial crisis. The Index continues to sit below the highs it set back in 2007.

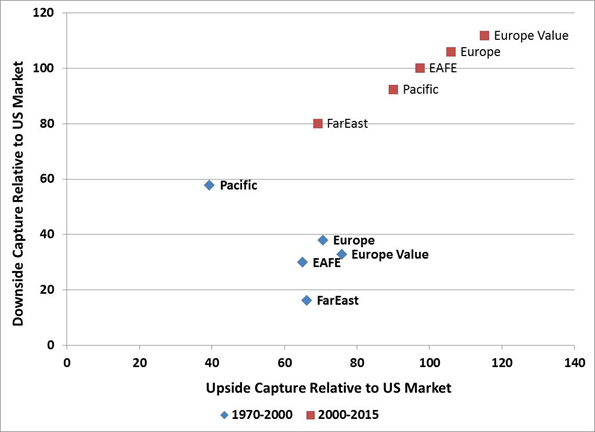

Another interesting aspect of the European Value Index is that at times it can rally faster and harder after a large decline in the US stock market (see the period following the 1987 crash and the 2000-2003 bear market). This also shows up in the data, especially over the last 15 years. Relative to the US market, the European Value Index’s downside capture – what it loses in relation to the US market when US stocks are falling - is 112%. Its upside capture is 115%. Put differently, European Value often behaves as if it were simply a more speculative and volatile subset of U.S. stocks. The graph below shows the broad MSCI regional indexes, and their upside and downside capture relative to the US during two periods. The blue markers show the variations of international indexes relative to the US from 1970 to 2000. This is the period where international stocks offered some diversification benefits – falling by a smaller amount in US bear markets, but capturing a majority of the gains of the US market when it rose. The red markers show how these international indexes have done relative to the US from 2000 until today. There has been a major increase in correlation, and reduction in the benefit of holding global markets as diversifiers in a portfolio. (For an additional discussion of these shifting correlations and their role in portfolio construction, see Fed Leaves Punchbowl, Takes Away Free Lunch (of International Diversification).

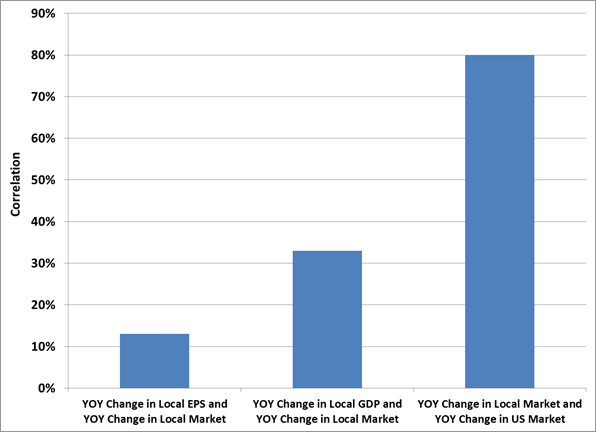

Simply put, it is best to own European value stocks when the US markets have experienced losses and the market begins to recover. The downside risks are amplified when the US market exhibits conditions that have typically led to bear markets, crashes, or steep corrections. (See John Hussman’s Plan to Exit Stocks Within the Next 8 Years? Exit Now for a discussion of current market conditions). If the high correlation between US markets and international markets persists, it may be best to consider the majority of international stocks as amplifiers to US market returns, rather than modifiers. On the topic of not fighting the central bank, Europe’s high correlations with US markets tends to trump ECB interest rate cuts. As John Hussman noted last week, the “Don’t fight the Fed” argument doesn’t fit the data once investor preferences have shifted to risk aversion (based on market internals, credit spreads, and other risk-sensitive measures). This has been particularly true during the past 15 years. The same can be said of European markets. Starting in October 2000, the Dow Jones Euro Stoxx Index fell 63 percent through March of 2003, during which time the ECB cut its rate from 4.75 percent to 2.5 percent. In July of 2008, even after European stocks already declined by nearly 25 percent in unison with US markets, the ECB raised its interest rate once. Three months later the ECB, began to lower rates aggressively, and during this period Euro-area stocks would fall another 45 percent. ECB QE would likely be ineffective at supporting Euro-area stocks during a decline in US stocks. Improving European Fundamentals There’s little doubt that European economies are showing some improvement in the last couple of months, following a steep drop in the euro and a pickup in export activity. The Citigroup Economic Surprise Index for the region reached 60 earlier this month, rare levels of altitude for this index in the last few years. Both the Eurozone manufacturing and composite PMI are above 50, and analysts are increasing their forecasts for earnings this year. It’s important to note, however, that the correlation of individual country markets with the US market swamps the correlation of individual country markets, as well as the fundamentals of these markets. All of this local fundamental data will become less compelling if the US markets turn lower. In the graph below I’ve plotted the average correlation between changes in local earnings and changes in the local country index for developed markets; the average correlation between changes in local GDP and the local country index; and the average correlation between changes in the local country index and the MSCI US index. Local fundamentals matter, but they tend to get overwhelmed by each country’s correlation to the US and the overall world markets.

--- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |