|

|

||||||

|

|

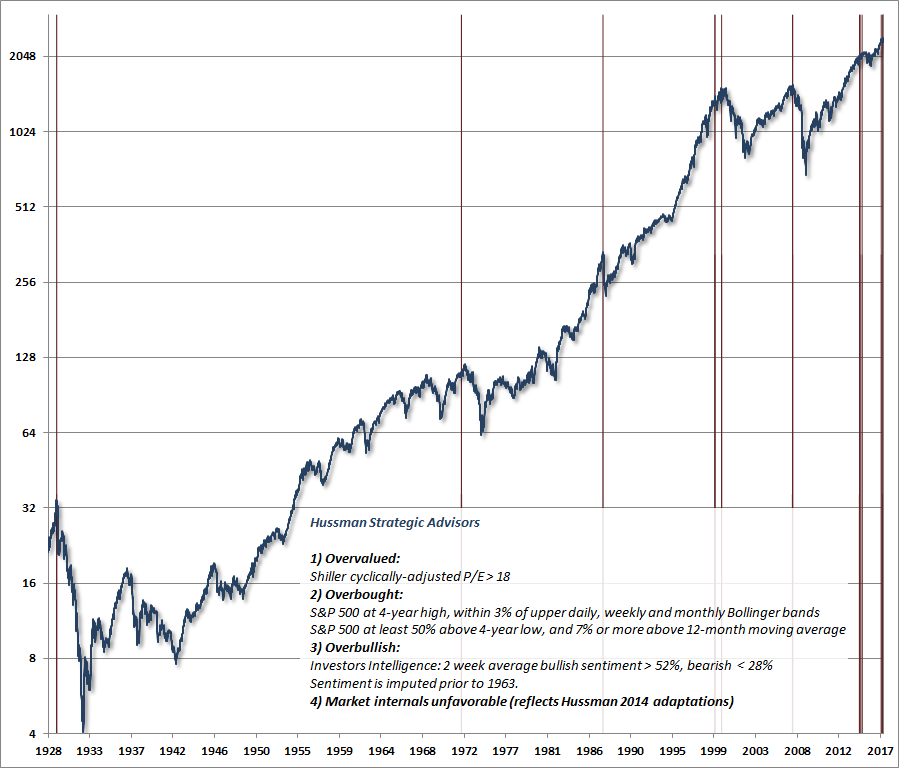

May 29, 2017 When Valuations Don't Seem to "Work" "Historically, when trend uniformity has been positive, stocks have generally ignored overvaluation, no matter how extreme. When the market loses that uniformity, valuations often matter suddenly and with a vengeance. This is a lesson best learned before a crash rather than after one." - John P. Hussman, Ph.D., October 3, 2000 "One of the best indications of the speculative willingness of investors is the 'uniformity' of positive market action across a broad range of internals. Probably the most important aspect of last week's decline was the decisive negative shift in these measures. Since early October of last year, I have at least generally been able to say in these weekly comments that “market action is favorable on the basis of price trends and other market internals.” Now, it also happens that once the market reaches overvalued, overbought and overbullish conditions, stocks have historically lagged Treasury bills, on average, even when those internals have been positive (a fact which kept us hedged). Still, the favorable market internals did tell us that investors were still willing to speculate, however abruptly that willingness might end. Evidently, it just ended, and the reversal is broad-based." - John P. Hussman, Ph.D., July 30, 2007 When one examines market cycles across history, including the most extreme speculative bubbles, one typically finds segments where valuations were clearly elevated relative to historical norms, and yet the stock market continued to advance. Still, one also finds that the market dropped like a rock over the completion of the market cycle. Likewise, one finds that virtually every point of significant overvaluation was systematically followed by below-average total market returns over a 10-12 year horizon. It’s precisely the failure of valuations to matter over shorter segments of the market cycle that regularly convinces investors that valuations don’t matter at all. This delusion is strikingly ingrained into investor behavior, and is almost inescapably revived during every speculative episode. As Graham and Dodd wrote in Security Analysis (1934), referring to the final advance that led to the 1929 market peak, the reason investors shifted their attention away from historically-reliable measures of valuation was “first, that the records of the past were proving an undependable guide to investment; and, second, that the rewards offered by the future had become irresistibly alluring.” The consequence of the delusion that “old valuation measures no longer apply” was predictably wicked, as it was after the 1969, 1972, 2000 and 2007 extremes. What’s distressing is that this delusion is actively encouraged by investment professionals who ought to know better. Valuations seem unreliable during speculative episodes because investors neglect a critical distinction. While long-term and full-cycle market outcomes are tightly determined by market valuations, the effect of valuations on outcomes over shorter segments of the market cycle depends on the psychological preference of investors toward speculation or risk aversion. When investors are inclined to speculate, they tend to be indiscriminate about it, and for that reason, we’ve found that the most reliable measure of investor psychology is the uniformity or divergence of market action across a wide range of individual stocks, industries, sectors, and security types, including debt securities of varying creditworthiness. Our own measures of market action extract a signal from the behavior of thousands of securities, and are not captured by simple indicators like 200-day moving averages or advance-decline lines. Still, as a rule-of-thumb, divergence in the behavior of a broad range of individual stocks from the behavior of the major indices tends to be a warning sign, as do widening credit spreads, or lack of uniformity in the behavior of various market sectors. Put simply, when valuation measures are steeply elevated but investors remain inclined to speculate, as evidenced by very broad uniformity of market action and the absence of internal divergences, rich valuations often have little effect on market outcomes. However, in an environment of extreme valuations, even fairly subtle deterioration in the uniformity of market internals should be taken as a signal of increasing risk-aversion among investors, and the market becomes vulnerable to steep and abrupt losses. Uniformity of market internals matters My hope is that, before the current speculative episode predictably unwinds in another catastrophe, investors will learn something from my own successes and challenges over more than 30 years as a professional investor. With regard to successes, my anticipation of the 2000-2002 and 2007-2009 market collapses was based on the combination of rich valuations and deteriorating market internals, which I discussed at the time. Conversely, my adoption of a constructive or leveraged investment stance after every bear market decline in the past three decades typically reflected the combination of a material retreat in valuations coupled with an early improvement in our measures of market action (though my early measures were rather crude). Since valuation is something I’ve never overlooked, the periodic challenges I’ve encountered in the past three decades have invariably centered on measures of market action. During the advance to the 2000 bubble peak, I became defensive too early. Still, I adapted not by abandoning valuations, but by increasing my research efforts. That research led to the recognition that uniformity across market internals could make even the most obscene levels of overvaluation temporarily irrelevant. Respecting that distinction, without disregarding overvaluation, allowed us to come out ahead over the complete market cycle, as the 2000-2002 decline wiped out the entire total return of the S&P 500, in excess of Treasury bills, all the way back to May 1996. Likewise, nearly all of our challenges during the advancing half-cycle since 2009 can be traced to my 2009 decision to stress-test our market return/risk classification methods against Depression-era data, which inadvertently led us to overemphasize “overvalued, overbought, overbullish” syndromes that had reliably warned of market losses in prior market cycles across history. The very reliability of these syndromes in prior market cycles made them a complication in the period since 2009. If quantitative easing and zero-interest rate policy made anything legitimately “different” about this half-cycle, it was to disrupt that historical reliability, and to encourage investors to continue speculating even after those extreme syndromes emerged. Most of our difficulty in the advancing half-cycle since 2009 would have been avoided by the key adaptation that we made in 2014: in the presence of zero-interest rate conditions, even the most extreme “overvalued, overbought, overbullish” syndromes were not enough. One had to wait for market internals to deteriorate explicitly before adopting a hard-negative market outlook (see Being Wrong in an Interesting Way for the full narrative). The supports have already eroded If one is talking about a complete market cycle, or 10-12 year investment prospects, valuations matter unconditionally. But if one is talking about a segment of the market cycle, valuations matter to the extent that they are aligned with the prevailing psychology of investors toward speculation or risk-aversion. Those preferences are best inferred from the uniformity or divergence of market internals. The result is that an undervalued market can continue to collapse until market internals demonstrate early improvement and positive divergences. Likewise, an overvalued market can continue to advance until market internals demonstrate early deterioration and negative divergences. Those shifts of internal market action don’t always have immediate consequences, and they have to be constantly monitored as the evidence changes. Still, a shift in market internals does immediately change the return/risk profile of the market; that is, the probability distribution that describes likely subsequent returns. An overvalued market with uniformly favorable market action has a dramatically different return/risk profile than an overvalued market with deteriorating market action. At present, we continue to identify one of the most hostile market environments we’ve observed in a century of historical data, not only because obscene valuations and extreme “overvalued, overbought, overbullish” syndromes are in place, but also because our measures of market internals remain in a deteriorating condition. That may change, in which case we will shift to a more neutral outlook. Indeed, if improvement in market internals is joined by a material retreat in valuations, we would expect to shift to a constructive or aggressive outlook (even if valuation measures were still well-above historical norms). Presently, speculators seem not to recognize how strongly the odds are stacked against them, and how steep and abrupt market losses could become. We are not inclined to “fight” further speculation by raising our safety nets on every advance, and again, our outlook would become far more neutral if market internals were to improve. Still, given the deterioration we observe in market internals here, Wall Street’s habit of dismissing and second-guessing every historically reliable valuation measure is likely to be rewarded by steep losses, as it has following every speculative extreme in history. Remember the key lesson Over the weekend, my friend Jonathan Tepper sent me a note suggesting that it might be interesting to discuss the extreme position of the S&P 500 relative to its upper Bollinger bands (two standard deviations above a 20-period moving average) at monthly, weekly, and daily resolutions. Several variants I’ve constructed to identify “overvalued, overbought, overbullish” syndromes include the use of Bollinger bands. Those who fully understand the key lesson of our 2014 adaptations will also know why Jonathan’s question made me cringe. See, prior to the advancing half-cycle that began in 2009, those “overvalued, overbought, overbullish” syndromes were regularly followed by air pockets, panics and crashes in stock prices. But in this cycle, there’s a whole block of those signals, literally for years, that were followed by further market advances, as the Federal Reserve’s deranged zero-interest rate policy encouraged continued yield-seeking speculation. One had to wait for internals to deteriorate explicitly before taking hard-defensive action in response to those signals. That single restriction (among the adaptations we introduced in 2014) is sufficient to wipe out the entire block of incorrect warnings. But the real-time challenges we experienced as a result of responding to those warnings prior to mid-2014 were ruthless to my previously lauded reputation (hence the cringe). It may take the completion of the current market cycle for investors to recognize that we’ve already adapted. Though the gain in the S&P 500 since 2014 is likely to be wiped out rather easily, the challenge for hedged equity strategies in the interim has been the extended duration of this top formation, coupled with a feverish shift of investors toward indexing, which has benefited the capitalization-weighted indices relative to a wide range of historically effective stock-selection approaches. As I noted approaching the 2007 peak, value-tilted portfolios often lag just before extended periods of weak or negative performance for the major indices. Conversely, the best time to establish a constructive or leveraged market outlook is when a material retreat in valuations is joined by an early improvement in market action. That’s the point that observers who consider me a “permabear” may become deeply confused, but again, I’ve done the same after every bear market decline in over 30 years of investing. My inadvertent branding is an artifact of my 2009 stress-testing decision (which truncated our late-2008 constructive shift), and it will understandably take a greater portion of the market cycle to shed that. Meanwhile, Jonathan is right - the S&P 500 is currently at extremely overvalued, overbought, overbullish levels. In the chart below, I’ve coupled one of our “Bollinger band” variants, limited to periods featuring explicit deterioration in our measures of market internals. Without that limitation, there would be a thick red block of false signals covering much of the recent half-cycle. That additional limitation also filters out a few useful warnings that preceded corrections in excess of -10% in 1998 and 1999, but it retains most of the signals in prior market cycles because “overvalued, overbought, overbullish” syndromes typically overlapped a shift toward risk-aversion by investors and a deterioration in our measures of market internals. To the extent that the Federal Reserve’s policies of quantitative easing and zero interest rates disrupted that overlap in the recent half-cycle, “this time” was legitimately “different.” But don’t fall prey to the delusion that this difference can't be accounted for in a systematic way.

Remember the key lesson. At the personal risk of sounding like a broken record, I also recognize the far greater risk that investors face by ignoring valuations, or assuming something has “gone wrong” with historically reliable measures. The upshot is that the psychological preference of investors toward speculation (which we infer from the behavior of market internals) can temporarily defer the consequences of extreme valuations. Respect that distinction without abandoning valuations altogether, and recognize that at least for now, the combination of obscene overvaluation, extreme overvalued, overbought, overbullish conditions, and divergent market internals creates a terribly hostile return/risk profile for investors. That profile will change as market conditions do. The extent that investors are sensitive to those changes will likely determine the extent that they weather the completion of the current cycle, and benefit from future ones. You are here Finally, we should distinguish ignoring valuation measures from systematic research to improve them. Much of my work over the past three decades has been along those lines. For example, our effort to carefully account for the impact of foreign revenues, and to create an apples-to-apples measure of general equity valuation led us to introduce MarketCap/GVA, which is better correlated with actual subsequent 10-12 year market returns than any of scores of measures we’ve studied. The problem is that we often see investors dismissing various measures of valuation, or proposing alternative measures, without any examination of the logic or historical validity of those measures whatsoever. Every valuation measure should be judged by a) whether it can be reasonably interpreted as a relationship between the current price and the very long-term stream of cash flows that stocks can be expected to deliver over the long-term, and b) the link between that valuation measure and actual subsequent total market returns, ideally over a period of 10-12 years (which is the horizon at which the autocorrelation profile of most valuation measures hits zero). I’ve previously demonstrated that the correlation of the Shiller cyclically-adjusted P/E (CAPE) with subsequent market returns is substantially strengthened by considering its embedded profit margin (the denominator of the CAPE divided by S&P 500 revenues). Indeed, adjusting for that embedded profit margin boosts the correlation with subsequent 10-12 year returns to nearly 90%. I mention this because investors seem to be playing a game of “you are here”: comparing the current unadjusted CAPE of 28 with the 2000 record high of over 43, inferring that the S&P 500 could rise by over 50% before matching that 2000 extreme. The problem is that in 2000, the CAPE was elevated because the embedded profit margin was just 5.1%, compared with a historical norm of 5.4%. In contrast, current CAPE embeds a profit margin of 7.4%, which results in a lower multiple that is only valid if we require recent record profit margins to be sustained permanently. On the basis of normalized profit margins (which improves the relationship of the CAPE with actual subsequent market returns), the margin-adjusted CAPE was 41 at the 2000 bubble peak, and is above 38 today. We observe the same thing for other historically-reliable measures such as MarketCap/GVA and the S&P 500 price/revenue ratio. Among the valuation measures having the strongest correlation with actual subsequent market returns, current levels are actually within 10% of the March 2000 extreme. There’s no question that investors have become nearly frantic in their verbal arguments about the permanence of elevated profit margins (which is something that Benjamin Graham observed at other market peaks, and warned against decades ago). We’re certainly open to systematic evidence supporting those arguments in a significant span of post-war data, ideally partitioning margins into the components that drive them. For my own analysis on this subject, see This Time is not Different, Because This Time is Always Different. Meanwhile, our best response to Wall Street’s evidence-free assertions about profit margins is to quote W. Edwards Deming: “Without data, you’re just another person with an opinion.” Again, if our measures of market internals were to improve, we would allow for the possibility that reliable measures of market valuations could surpass their 2000 extreme, and we would not place a “cap” on how high stock prices could move. As I observed approaching the 2007 peak, "As long as investors perceive valuations to be acceptable, there is no compelling reason why the actual facts should get in their way over the short-term. That allows for the possibility that the current speculative blowoff will continue further. The implications for long-term returns remain daunting, but over the short-term, perception is reality." The effect a shift back to uniformly favorable market internals would be to move us to a more neutral outlook, though we would maintain our expectation of dismal full-cycle and long-term outcomes. An early improvement in market action following a material retreat in valuations would provide latitude for a constructive or aggressive outlook. Presently however, the market environment features a combination of obscene overvaluation, extreme “overvalued, overbought, overbullish” syndromes, and deteriorating market internals. The first two features of that combination create poor long-term and full-cycle prospects for the market. The last feature of that combination is what currently opens a potential abyss. Our outlook will shift as conditions change. The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |