|

|

||||||

|

|

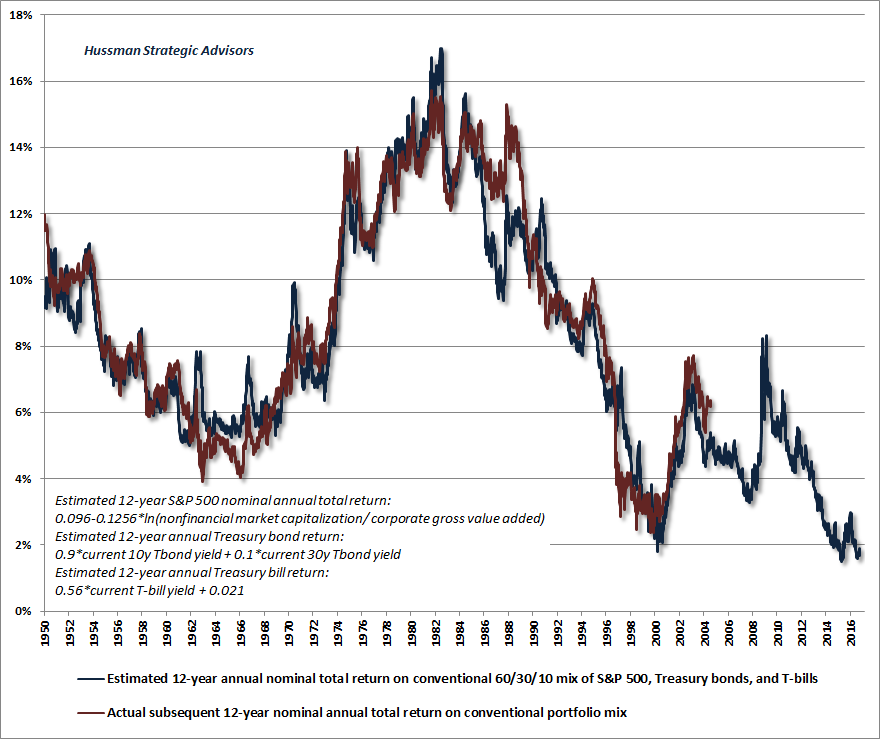

October 10, 2016 Overvaluation, Deteriorating Market Action, and Coordinated Exit A few weeks ago, our most reliable measures of market internals shifted to a uniformly unfavorable condition, reversing a few trend-following components that had held us to a fairly neutral near-term outlook for several months (see Support Drops Away). This deterioration was indicative of a shift away from the somewhat mixed investor attitude toward risk that we’ve seen since March, and toward increasing risk-aversion; particularly an unwillingness to extend speculative yield-seeking in the face of already extreme valuations across multiple asset classes. Since then, we’ve seen a series of abrupt but still shallow and uncoordinated retreats in U.S. and German government bonds, precious metals, and utility shares, along with a brief “flash crash” in the British pound. My impression is that these may be the initial tremors of a more systematic “risk off” shift among investors, but that remains more a possibility than a forecast. What we do know is that based on the observable data we use to classify expected market return/risk profiles, the profile we currently identify for stocks has been associated with extremely poor market outcomes, on average, across history. Indeed, the current profile on a blended horizon of 2-weeks to 18-months is among the most negative we’ve observed in post-war data outside of the market peaks in 2000 and 2007. Keep in mind that much of our concern and defensiveness before mid-2014 was driven by the repeated emergence of extreme overvalued, overbought, overbullish syndromes that were regularly associated with steep market losses in prior market cycles across history. The only thing truly “different” about the advancing half-cycle since 2009 was that the Federal Reserve’s deranged experiment in quantitative easing aggressively and intentionally encouraged yield-seeking speculation even after overvalued, overbought, overbullish extremes repeatedly appeared. Rather than becoming risk-averse in response to those extremes, as investors had in prior market cycles, QE disrupted that response, and investors continued speculating. Given a zero interest rate environment, one had to wait until market internals deteriorated explicitly, signaling a shift to risk-aversion among investors, before taking a hard-negative outlook on the market. See the Box in The Next Big Short for the full narrative. Notably, the broad market has essentially flat-lined since mid-2014, with the NYSE Composite still below its July 2014 level. Market behavior has also increasingly featured sequences of small, marginal advances punctuated by abrupt “air pocket” losses. This behavior reflects what I’ve often called “unpleasant skew.” See Impermanence and Full-Cycle Thinking for a chart of what the underlying return/risk distribution looks like. My impression is that one of the “air pockets” ahead is likely to be accompanied by an initial but meaningful credit event, quickly devolving into an outright bear market collapse as trend-sensitive and volatility-targeting investors attempt a coordinated exit on the break of widely-monitored support levels. It’s worth repeating that once risk-aversion kicks in strongly, monetary easing has historically failed to support the markets, because at that point, low-interest liquidity is viewed by investors as a desirable asset rather than an inferior hot-potato. Creating more of the stuff, as investors should recall from the persistent and aggressive easing of the Fed during the 2000-2002 and 2007-2009 collapses, doesn’t promote much more than a few days of risk-seeking. Meanwhile, the expected return/risk profiles we identify for Treasury bonds, corporate debt, high-yield credit, utilities, and even precious metals have all deteriorated, which is somewhat unusual in that these profiles typically strengthen on price retreats. Among these, only the profile for precious metals is even positive, but it has also backed off substantially from our estimates earlier this year. The problem currently is that uniform, though subtle, deterioration in market internals and related support factors is driving the negative shifts we observe here across nearly every asset class. The unfavorable effect of deteriorating market internals has outweighed the slight improvement of valuations created by price declines. History teaches that once rich valuations are joined by unfavorable market action, particularly when deterioration emerges across multiple asset classes, steep losses can emerge without specific and identifiable “catalysts” (e.g. 1987). Even when a catalyst is present, it’s typically only a symptom of a larger set of risks, and investors only ascribe it with pivotal importance in hindsight (e.g. Lehman). Still, with regard to specific risks, the most salient vulnerability today is still the European banking system, and while Deutsche Bank has the highest gross leverage ratio among major institutions, the largest French and Swiss banks are close behind. Other risks include unbalanced growth and a property bubble in China, heavy use of leverage in price-insensitive investment strategies, and U.S. corporations that are now more highly leveraged as a ratio of gross value-added than at any point in history. In a very late-stage global financial bubble, which we’re in whether Wall Street or policy makers realize it or not, it’s not really necessary to identify which risk will blow up first as economic growth slows, profit margins narrow, and risk aversion increases. Once a barrel of lit matches rolls into a field of dynamite sticks, you don’t try to predict which one will explode; you just get the heck out of there. I’m not encouraging investors to sell everything - in aggregate, that’s not even possible. Every security that’s issued has to be held by someone until that security is retired. Despite what we view as wicked overvaluation, someone has to take a hit for the team over the completion of this market cycle. It’s still best if those investors do so after reviewing history and considering or dismissing our own concerns. Whatever your investment strategy, just make sure that it’s sufficiently disciplined and historically-informed that you’ll remain willing to follow it, without abandoning it in the face of steep market losses. Every disciplined strategy has challenging periods over the course of a market cycle. They just come at different times. We’re seeing numerous hedge funds close, across a wide range of investment disciplines, as advisors and pension funds move away from strategies that involve discretion and selective investment, in preference for strategies that are always fully-exposed to market risk. I see this as pure, unadulterated, late-cycle, market-top behavior. Whether you’re a passive buy-and-hold investor or a tactical one, the dumbest thing a smart investor can do with a disciplined, historically-informed, full-cycle strategy is to abandon it after the portion of the cycle where it didn’t do well, and chase a different strategy that did well in hindsight. “Risk-on, all-the-time” has done well in recent years precisely because nearly every asset class has been driven to obscene valuations. By making a shift into passive strategies after-the-fact, investors are locking in the worst prospects for 10-12 year portfolio returns in history, along with the likelihood of awful interim losses.

None of this means that every investment has to be held forever. It’s just that investors can destroy themselves over time by repeatedly chasing companies or strategies they see as “winners” and abandoning companies or strategies they see as “losers.” In my view, the elements of a good sell discipline are: 1) look to sell lower-ranked holdings on periods of strength; 2) look to buy higher ranked candidates on periods of weakness; and 3) limit selling on weakness to a) initial deterioration after an extended period of strength or overvaluation, or b) an event that changes the long-term fundamentals of the company or strategy. With regard to risk, investors should recognize: 1) the potential risk of equity market losses on the order of 40-55%, which would still represent only a run-of-the-mill cycle completion from current valuations; 2) the tendency for seemingly “safer” assets (e.g. dividend-paying stocks, utilities, international stocks in countries with generally lower valuations) to be highly correlated with the S&P 500 when U.S. stocks collapse; and 3) the potential for meaningful bond market losses on Treasuries, corporate bonds, and junk debt in response to yield spikes, given compressed yields, narrow risk-premiums on bonds, and a resulting elevation of durations. I continue to believe that investors should make room in their portfolios for safe, low-duration assets, hedged equities, and alternative strategies that have a modest or even negative correlation with conventional securities. Even low-yielding cash has significant option value, because it provides investors with the future opportunity to establish exposure to conventional assets after a material retreat in valuations. Overvaluation, deteriorating market action, and coordinated exit Remember that the hinge that distinguishes an overvalued market that continues higher from an overvalued market that crashes is the preference of investors toward risk-seeking or risk-aversion. We find the most reliable measure of that preference to be the uniformity or divergence of market action across a broad range of individual stocks, industries, sectors, and security types. We’re certainly open to a shift toward more uniformly favorable market action, which could put us back to a more neutral outlook, or one that might be characterized as “constructive with a safety net.” Unfortunately, even that sort of shift wouldn’t be associated with a very strong expected return/risk profile here, because valuations remain so offensive. Historically, the best opportunities to boost market exposure emerge when a material retreat in valuations is joined by an early improvement in market action. At present, exactly the opposite is true. Extreme valuations and compressed risk-premiums have been joined by deterioration in market internals. This deterioration is an indication of growing risk-aversion among investors. Much of the recent bubble has been driven by yield-seeking, trend-sensitive speculators, with value-conscious investors progressively stepping back. As a result, any coordinated attempt by trend-sensitive market participants to exit by selling stock is unlikely to be met by demand from value-conscious investors at prices anywhere near present levels. This, in turn, leaves the market vulnerable to potentially abrupt losses. As I detailed a few months ago in Lessons from the Iron Law of Equilibrium, what matters isn’t so much the balance between bulls and bears per se, but instead the balance of sentiment between trend-sensitive and value-conscious investors: “Understand that the worst market declines typically emerge from conditions where value-conscious investors have been defensive for quite some time, and where trend-following speculators have been rewarded for quite some time. The most severe price losses are those where trend-followers are ‘all in,’ followed by an initial deterioration in market action that prompts them to reduce their desired holdings. In contrast, the strongest market advances are those where trend-followers are out (offset by value-conscious investors being all-in) and an initial improvement in market action prompts trend-followers to abruptly increase their desired holdings. “In market cycles across a century of history, the strongest market return/risk profiles we identify are associated with a material retreat in valuations that is then joined by an early improvement in market action. By the time value investors are all-in, trend-followers are out. They then have to pry stock away from committed value investors once market action begins to improve, driving prices sharply higher. Conversely, the most severe market collapses are associated with steep overvaluation that is then joined by initial deterioration in market action. By the time trend-followers are all-in, value investors are out, and attempts by trend-followers to exit require prices to decline until skittish value-conscious investors are willing to absorb the shares being offered for sale.” Put simply, current market conditions are associated with small potential returns and enormous latent risks across nearly every asset class. The combination of extreme valuations, weak prospective returns, and emerging risk-aversion suggests that market losses could unfold abruptly, creating an interconnected Rube Goldberg chain of consequences because of the steep leverage that investors and corporations have taken on in recent years. The image that comes to mind is that of speculators scrounging around on their hands and knees to pull a few pennies from the catch of a mousetrap whose hammer is tied to the lid of a box of angry bees and a switch that drops an anvil. Even if there are rewards in the short-run, the situation isn’t likely to end well.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |